Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, legal counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.

Chris has led thousands of valuations, including for equity securities, intangible assets, financial instruments, investment valuations, business valuations for tax compliance and financial reporting compliance, as well as fairness and solvency opinions.

Startup valuation is an incredibly complex and nuanced process.

There are a lot of variables to consider: the nature of your business, your business model, the market potential, your team’s expertise, and more.

But it’s also incredibly important. An inaccurate or skewed valuation can lead to:

Lost investment opportunities

Poor strategic decisions and potential financial losses

Compliance issues with tax authorities and legal penalties

At Eton, we’ve helped hundreds of startups with their valuations over the past 15 years, making us highly experienced in the field.

In this article, I’ll give you a complete guide to the startup valuation world, including:

Key Factors that Impact Valuation

10 Startup Valuation Methods

Case Studies from Real Companies

Best Practices When Valuing Startups

Key Takeaways:

Whether you’re planning for a merger or acquisition, or issuing stock options to your employees, getting your valuation right is so important to avoid financial losses, legal penalties, and bad investment decisions.

Startup valuation depends on a lot of different factors like the maturity of the company, market size, product stage, team experience, and growth trajectory.

There are 10 key valuation methods and the most relevant ones to startups are the Berkus, Scorecard, and Risk Factor Summation methods.

For best valuation results, we recommend you combine different valuation methods, understand market dynamics, prepare thoroughly, and consult a valuation expert.

What is Startup Valuation and Why Is It So Important to Get It Right?

Startup valuation is the process of figuring out how much a startup and its assets are worth at a specific time, also called the fair market value (FMV).

This involves examining various aspects of the startup, including:

Capital structure

Future cash flows

Earnings estimation

Other financial metrics

FMV is what someone would pay for a business or property if both the buyer and seller are willing, not forced, and both have reasonable knowledge of relevant facts.

When might you need to determine FMV? Let’s look at key scenarios and why it’s important to get this value right.

1. Employee Stock Compensation for 409A Requirements

In tech and software fields, 409A valuations are essential for companies issuing stock options as part of employee compensation.

These valuations determine the fair market value (FMV) of your company’s common stock, ensuring that stock options granted to employees comply with IRS regulations.

Accurate 409A valuations prevent penalties and provide a defensible FMV, protecting both your company and your employees from unfavorable tax consequences.

Compliance with these regulations builds trust and transparency within your company and with the IRS.

2. Raising Venture Capital

When you’re raising venture capital, accurate valuations determine ownership percentages for new and existing investors.

Known as “Venture Capital Valuations,” they assess your company’s worth before (“pre-money”) and after (“post-money”) new capital injections.

This helps you negotiate fair investment terms and attract investors by providing transparency and confidence in your startup’s growth potential.

Accurate valuations ensure you retain appropriate equity and control, aligning all stakeholders’ interests.

3. Mergers and Acquisitions (M&A)

Valuations play a critical role in mergers and acquisitions by helping founders, investors, and potential buyers understand the value of the company.

Exit valuations, similar to M&A valuations, offer a clear picture of your company’s worth during an acquisition or sale.

These valuations facilitate negotiations and decision-making by providing realistic expectations about the potential return on investment.

Accurate valuations ensure that all parties have a solid basis for aligning interests and finalizing deals.

4. Financial Reporting

Accurate valuations are vital for financial reporting purposes.

They ensure regulatory compliance with accounting standards and provide stakeholders with a true picture of the company’s financial health.

Reliable valuations build trust among investors, creditors, and other stakeholders by demonstrating transparency and integrity in the company’s financial statements.

This transparency is crucial for maintaining strong relationships with financial backers and regulatory bodies.

5. Taxation

Valuations are crucial for determining the correct amount of taxes your startup owes.

Accurate valuations help you avoid overpayment or underpayment of taxes, preventing fines and penalties.

Compliance with tax laws maintains your financial stability and reputation with tax authorities.

Accurate tax valuations also prevent potential disputes with tax authorities, saving you time and resources.

Exit valuations estimate your company’s value in the context of an acquisition or sale.

Accurate valuations maximize returns for you and your investors by providing a clear basis for negotiating exit terms and structure.

They help determine the best exit timing and ensure fair compensation for all parties, leading to a successful and profitable exit.

So, what are the key factors that influence the accuracy of your valuation?

5 Key Factors Influencing Startup Valuations

There is no one-size-fits-all when it comes to valuing startups. It’s highly subjective and depends on a lot of different factors like:

Factor 1: The Maturity of the Startup

The maturity of a startup, from seed stage to more developed stages, impacts its risk profile and the amount of data available for valuation.

Early-stage startups come with higher risks and less data, whereas more mature startups have more operational history and possibly consistent revenue streams.

Factor 2: Market Size

The potential market size is crucial because it indicates the upper limit of what the startup could eventually earn.

Larger markets often allow for higher valuations due to the greater potential for revenue and growth.

Factor 3: Product Stage

The stage of the product (idea, prototype, fully developed, etc.) affects risk level.

The further along a product is in development, the lower the risk and the higher the valuation, as there is more proof of concept and potentially early traction.

Factor 4: Team Experience

A strong, experienced management team can significantly enhance a startup’s valuation.

This is because their experience typically reduces the risk of failure and increases the likelihood of successful execution.

Factor 5: Growth Trajectory

A startup’s historical growth and future growth potential are critical.

Rapid growth not only in revenues but also in user base or market share can lead to higher valuations.

As you can see, valuing startups is a nuanced and subjective process that requires a level of expertise many individuals might not possess.

This is why I advise folks to work with a trusted startup valuation expert to avoid legal penalties and financial losses.

At Eton, our boutique team of Stanford Law lawyers and Ex-Big 4 Consultants provide compliant, independent, and audit-defensible startup valuations leveraging our 15 years of experience.

However, if you’re considering undertaking the valuation on your own, below are the criteria to determine if you are prepared to conduct your own startup valuation.

You have a comprehensive understanding of valuation methods.

You are well-versed in key financial metrics.

You possess deep industry knowledge.

You can maintain objectivity in your assessment.

You are aware of legal and regulatory implications.

You hold relevant credentials, such as a CFA or CPA.

You have access to all required data.

You can convincingly explain your valuation to investors.

You have the time and resources necessary for a thorough valuation.

If you can check everything in the above list, you might be qualified to value your startup. In the next section, I’ll share all the key valuation methods that you can consider.

One key thing to take note of when choosing a valuation method is that startups are very different in nature from publicly traded companies.

Traditional valuation methods like Discounted Cash Flow (DCF) and Comparables don’t work for startups (or they can lead to skewed results) as startups usually don’t have substantial historical financial data or comparable assets. But if you do have these, the traditional methods are suitable.

Most valuators consider alternative approaches when they’re working with startups.

Below, I’ll share 10 different valuation methods, divided into 3 categories:

Qualitative Startup-Specific Methods

Quantitative Startup-Specific Methods

Traditional Valuation Methods

3 Qualitative Startup Valuation Methods

These methods depend more on judgment and estimation, such as evaluating the team’s expertise, market potential, and innovative business models, rather than relying solely on hard numbers like financial history, which many new companies lack.

Startups often face uncertain futures and rely heavily on these factors, making qualitative assessments crucial.

Here are the three qualitative startup valuation methods:

Berkus

Scorecard

Risk Factor Summation

Method #1: Berkus

The Berkus Method assigns a monetary value to key qualitative aspects of a startup, like its operations and risks.

When Is Berkus Used

Berkus is used to value early-stage startups, where financial data is scarce or non-existent.

However, it can only be used for startups which are expected to reach at least $20m in revenues in the next five years.

How to Calculate Berkus

1. Assign a value of up to $500,000 to each of the five key elements:

Sound Idea

Prototype

Quality Management Team

Strategic Relationships

Product Rollout or Initial Sales

2. Add the assigned values to get the total pre-money valuation of the startup.

Example

Let’s assume a startup with the following characteristics:

Sound Idea: $300,000

Prototype: $400,000

Quality Management Team: $450,000

Strategic Relationships: $350,000

Product Rollout or Sales: $250,000

Total Berkus Valuation: 300,000+400,000+450,000+350,000+250,000=1,750,000

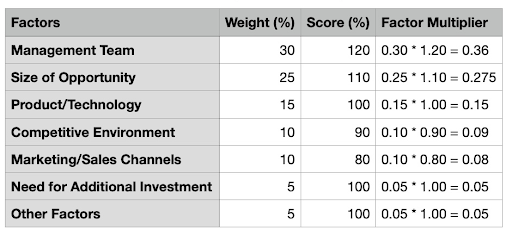

Method #2: Scorecard

The Scorecard Valuation Method helps angel investors value pre-revenue startups (in the valuation range of $1m and $2.5m) by adjusting average pre-money valuations using weighted factors.

When to Use Scorecard

It is best used for pre-revenue startups that have some initial market traction but do not have long-term financial data.

It’s especially useful where many similar startups exist by development stage, sector, and location.

How to Calculate Scorecard

Identify the average pre-money valuation of similar companies in the region and industry for a baseline.

Identify key factors and assign weights based on importance:

Strength of the Management Team (0-30%)

Size of the Opportunity (0-25%)

Product/Technology (0-15%)

Competitive Environment (0-10%)

Marketing/Sales Channels/Partnerships (0-10%)

Need for Additional Investment (0-5%)

Other factors (0-5%)

Compare the target startup to the average using these factors.

Assign a score (%) to each factor based on performance relative to the average.

Scores can exceed 100% if the startup is above average.

Multiply each factor’s weight by its score to get the factor multiplier.

Add the multipliers to get the total adjustment factor.

Multiply the total adjustment factor by the average pre-money valuation to get the adjusted valuation.

Quantitative valuation methods use numerical data and calculations for startups that have enough financial data to make such an analysis.

Hence it is particularly useful for startups beyond the seed stage entering growth phases.

These are the 3 methods:

Venture Capital

First Chicago

Cost-to-duplicate

Method #4: Venture Capital

Also called “Pre-Money” and “Post-Money” valuations, it is used during fundraising to determine the value of a company before and after new capital is injected.

These help in determining the ownership percentages for new and existing investors.

It estimates the future exit value of a startup and discounts it back to the present using the expected rate of return.

When to Use Venture Capital

For startups that anticipate significant growth and plan to exit via sale or IPO within a foreseeable timeframe.

How to Calculate Venture Capital

1. Estimate a terminal value of the startup at the time of exit.

It is found using relative valuation multiples in the year of exit.

It requires an estimate of either revenue or earnings in the year of exit.

2. Discount the terminal value using a proper discount rate.

The investor’s expected ROI is used as a discount factor.

4 Traditional Late-Stage Startup Valuation Methods

If you’re a late-stage startup, have substantial historical financial data, or comparable assets in the industry, then these traditional valuation methods will be suitable for you.

These methods are applied to businesses in general, not just startups.

These are the 4 traditional valuation methods:

Discounted Cash Flow

Market Comparables

Precedent Transaction

Real Options

Method #7: Discounted Cash Flow

Discounted Cash Flow (DCF) estimates the value of an investment based on its expected future cash flows.

These cash flows are discounted back to their present value using a discount rate that reflects the investment’s risk and the cost of capital.

When to Use DCF

For businesses with predictable, stable cash flows and a record of historical financial data.

How to Calculate DCF

The general formula for DCF is:

Where:

CFt is the cash flow in year t, and r is the discount rate.

Here are the general steps to start the valuation process:

Estimate the future cash flows for each period.

Choose an appropriate discount rate based on the risk profile and time value of money.

Calculate the present value of each of these future cash flows.

Sum up all these present values to get the total DCF value.

Example

Assume $100,000 annual cash flows for 5 years at a 10% discount rate.

The Market Comparables method values a company by comparing it to similar companies with publicly available financial data.

This approach utilizes financial ratios such as the ones below to gauge a company’s market value relative to its peers.

Price-to-Earnings (P/E)

Price-to-Sales (P/S)

Enterprise Value-to-EBITDA (EV/EBITDA)

When to Use Comparables

It’s effective in industries with many public companies, providing robust data for comparison.

How to Calculate Comparables

Find the right comparable set of companies.

Gather their financial data.

Define which financial parameters and multiples to compare.

Calculate the comparable ratios.

Determine the value by applying the average industry multiple to the financial metric of the company being valued.

Value=Metric×Average Industry Multiple

Example

Assume:

Similar companies in the tech industry are trading at an average P/E of 25

The company being evaluated has earnings of $4 million

So Value = $4M x 25 = $100M

Method #9: Precedent Transaction

The Precedent Transaction method values a company by analyzing the prices paid for similar companies in past acquisition deals.

It takes into account the premium that buyers have historically been willing to pay for companies within the same industry.

When to Use Precedent Transaction

This method is particularly effective in industries where acquisitions are common and there is a sufficient record of past sales.

How to Calculate Precedent Transaction

Find relevant transactions that have happened in recent years.

Determine a range of valuation multiples.

Commonly used multiples include:

Enterprise Value-to-Revenue

Enterprise Value-to-EBITDA

Price-to-sale

Apply the defined multiples to the company being evaluated.

Example

Suppose

Similar companies in the same industry were acquired for an average multiple of 4x sales.

The company being evaluated has sales of $10 million.

So Value = $10M x 4 = $40M

Method #10: Real Options

Real Options Valuation (ROV) values the flexibility to change strategies in response to future events.

It treats investments as options, measuring the value added by management’s ability to adapt, like expanding, delaying, or abandoning a project.

When to Use Real Options

Use Real Options in highly volatile industries with uncertain future conditions.

It is used for projects or companies with significant investment in innovative technologies, real estate development, or natural resources where investment decisions impact future cash flows.

How to Calculate Real Options

The valuation typically involves complex financial modeling, often using techniques from options pricing.

The basic formula inspired by the Black-Scholes model might look like this:

S = current value of potential cash flows

K = present value of exercise price (investment costs)

r = risk-free rate

T = time to maturity of the option

N(d) = cumulative normal distribution function

d1 and d2 = factors derived from the volatility of the underlying asset and other variables.

Example

A startup has the option to expand its operations in one year.

The cost of expansion is $1 million

Projected additional revenue from expansion is estimated to be $2 million in two years.

Risk-free rate is 5%

Volatility of the project’s returns is 20%

Calculation:

🤔Want tailored advice for your startup valuation? 🤔 This article is great for general guidance on the startup valuation process but unfortunately, it can’t be tailored to your unique circumstances. And when it comes to valuation, circumstance determines everything.

If you want personalized advice to help you navigate your startup valuation, get in touch with us here. We can provide advice specific to you over a call.

Otherwise, please read on for case studies and best practices.

Startup Valuation Case Studies from Real Companies

Now that you know the top 10 methods, let’s look at 2 case studies to understand startup valuations better in context.

The valuation was based on the company’s rapid user growth and profitability since its platform launch.

Since 2019, MoonPay:

Processed over $2bn

Grew to 7 million users

Expanded with 250 partners in 160 countries

Ivan Soto-Wright, the CEO, compared Moonpay to PayPal for cryptocurrency, emphasizing its “crypto-as-a-service” model and highlighting a 35x transaction volume increase in two years.

Outcomes of the Valuation:

MoonPay raised $555 million, valuing the company at $3.4 billion.

This is the largest and highest valued Series A for any bootstrapped crypto company globally.

This substantial valuation was supported by investments from major firms like Tiger Global and Coatue.

The valuation considered Griffin’s innovative “banking-as-a-service” (BaaS) model, which allows other fintechs to develop banking services without extensive in-house resources.

This approach, combined with the achievement of obtaining a banking license, significantly bolstered Griffin’s appeal to investors.

Outcomes of the Valuation:

Griffin raised $24 million from investors like MassMutual Ventures and Nordic Ninja.

Best Practices to Get Your Valuation Right

Most founders overestimate their company’s worth because they are emotionally attached, leading to unrealistic expectations.

Conversely, undervaluing your company can dilute ownership more than necessary and reduce future fundraising capabilities.

To ensure a balanced valuation, here are my best tips based on my years of experience in startup valuation:

Use Multiple Valuation Methods

Most founders overestimate their company’s worth due to emotional attachment, leading to unrealistic expectations.

Conversely, undervaluing your company can dilute ownership more than necessary and reduce future fundraising capabilities.

To ensure a balanced valuation, use multiple methods to value your business, selecting those that best fit your data and business stage.

Combining approaches like the discounted cash flow (DCF) method, comparable company analysis, and the venture capital method provides a comprehensive view of your startup’s worth.

This multi-faceted approach helps mitigate biases and gives a fuller, more accurate picture of your company’s value.

Understand Market Dynamics

Analyze similar companies and industry trends to get a sense of the competitive landscape.

This involves looking at recent funding rounds, valuations, and exits of comparable startups.

Understanding market dynamics helps you set a competitive yet realistic valuation. It also demonstrates to investors that you are aware of your market position and the factors influencing your industry.

Staying informed about market conditions ensures your valuation reflects current realities and future potential.

Prepare Thoroughly

Comprehensive documentation is key to a credible valuation.

Ensure you have clear, well-organized financial records, detailed business plans, and robust projections ready.

This preparation includes up-to-date profit and loss statements, balance sheets, cash flow statements, and any other relevant financial documents.

Thorough preparation shows your professionalism and readiness for scrutiny, building trust with investors and stakeholders.

Well-prepared documents also make it easier for valuation experts to assess your business accurately, leading to a more precise valuation.

Consult Professionals

Consulting valuation experts is essential for an objective view and guidance through complex valuation frameworks.

Professionals bring experience and expertise that can identify nuances you might miss. They can help you navigate different valuation methods, interpret market data, and understand regulatory implications.

Working with experts, like Eton, ensures your valuation is compliant, defensible, and based on sound financial principles.

Their objective perspective can balance your emotional attachment to the company, leading to a more realistic and credible valuation.

Our Startup Valuation Services – Eton

Since 2010, Eton has delivered thousands of audit-defensible startup and 409A valuations.

We’re a boutique team of Stanford Law lawyers and Ex-Big 4 Consultants who obsess over great service at affordable prices.

Our valuations are built on robust methodologies that stand up to scrutiny, so you avoid unnecessary costs and complications.

If necessary, we also defend our valuations in court.

Why you should work with us

I’ve said it before and I’ll say it again—startup valuations are incredibly nuanced and complicated.

You need a valuation partner who’s not only good at what they do, but is also willing to answer all your questions and give you guidance throughout the journey.

That’s what Eton offers.

With Eton, you’ll get the accuracy and reliability of a Big-4 firm, plus a personalized and attentive approach of a boutique firm.

If you work with us, we’ll assign you a senior startup valuation expert, and you’ll have direct access to me, the CEO.

Whether you have a question or a concern, I’m always one call or email away.

But don’t take it from me—hear what our previous startup clients had to say about us.

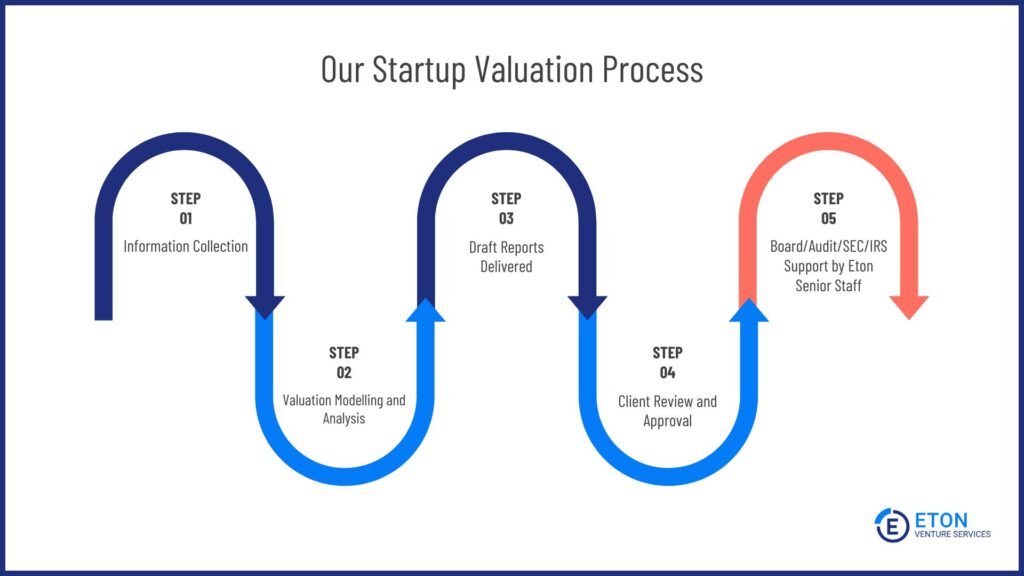

At Eton, we can deliver a startup valuation in 10 days or less.

Provided we have all the necessary documents, we can even complete it in as short as a day for an extra fee.

Here’s how our startup valuation process looks like typically:

If you’re ready to partner with us for your startup valuation, or if you’d like more information, please get in touch with me here.

Startup Valuation – FAQs

Have more questions about startup valuation? I answered them below:

What are 3 ways to value a startup?

In this article, I discussed 10 key valuation methods. Among them, these three methods are most suitable for startups:

Berkus Method: values a startup based on qualitative factors, assigning a monetary value to five key elements (sound idea, prototype, quality management team, strategic relationships, product rollout or sales) to determine its worth.

Scorecard Method: evaluates a startup by comparing it to other funded startups, adjusting the average valuation of similar startups based on factors such as:

The strength of the team

Product

Market

Business stage.

Risk Factor Summation Method: estimates a startup’s value by identifying and assessing 12 risk factors, such as:

Management

Stage of the business

Legislation

Manufacturing

Sales

Funding

Competition

Technology

Litigation

International

Reputation

Potential lucrative exit

You adjust the average valuation by adding or subtracting based on these risks.

How often should a startup be valued?

Startups should typically be valued at key stages such as before raising a new round of funding, during mergers and acquisitions, for 409A compliance, and whenever there are significant changes in the business model or market conditions.

get in touch

Let's talk.

Schedule a free consultation meeting to discuss your valuation needs.

Written by Chris Walton, JD

Written by Chris Walton, JD