Written by Chris Walton, JD

Written by Chris Walton, JDIn a nutshell: This section summarizes the fair market value calculation and provides oversight of the approaches and methodologies used.

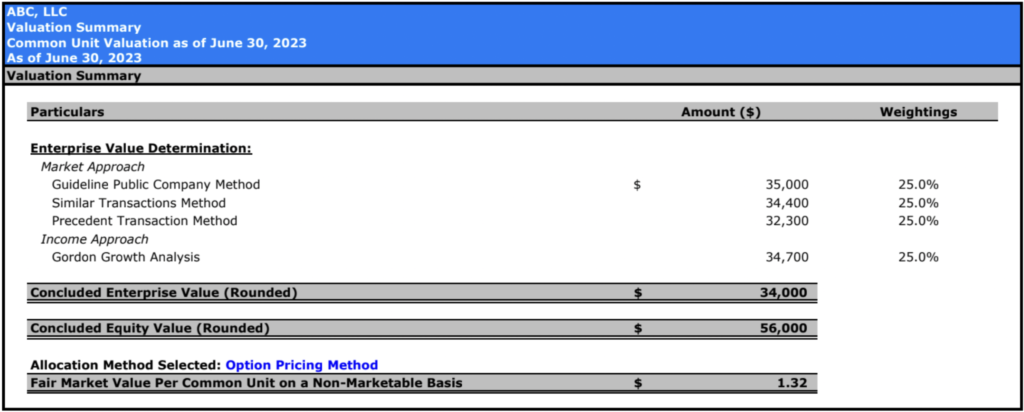

Every 409A valuation report we produce begins with a valuation summary.

This summary tells you what methods we took to determine the equity value of your company and then shows the concluded FMV of the common security (here, a “unit” because the 409A report is from an LLC).

In this example, the “Fair Market Value Per Common Unit on a Non-Marketable Basis” (i.e., post-DLOM) is $1.32.

In a nutshell: The Business Enterprise Valuation Determination shows in detail the value indications (enterprise and equity value) based on the methods we used to provide a reasonable and rigorous analysis, ensuring the 409A valuation report complies with “Safe Harbor.”

You might also like: 409A Valuation Requirements | How Often & When

As you can see in the image above, this section first showcases the value indication determined by each methodology applied, their weightings (25% each), the Concluded Equity Value, and the Concluded Enterprise Value.

Helpful hint: In a 409A valuation, it’s essential to consider both the Equity Value and the Enterprise Value of the company. The Equity Value reflects the worth of the company’s shares, vital for determining the fair market value (FMV) of common stock for stock option pricing and reporting exercises. On the other hand, the Enterprise Value offers a broader perspective, encompassing not just equity but also debt and other factors, to give a comprehensive view of the company’s total value. Understanding these two values in conjunction provides a more nuanced and accurate assessment of the company’s financial standing, crucial for a reliable 409A valuation. |

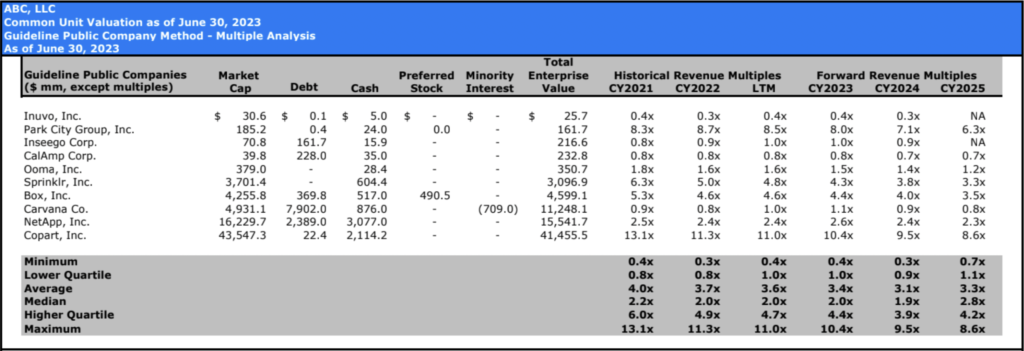

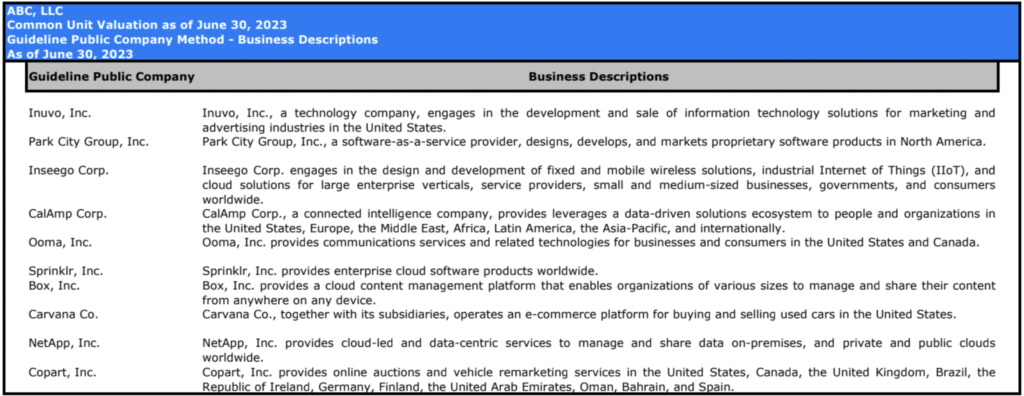

In this sample 409A valuation report, one of the approaches applied is the Market Approach, which uses three methods. You’ll find tables pertaining to all three and in the order they were first presented.

In the two images below, the report shows tables outlining the financial metrics and multiples of the companies used as comparison points in the Guideline Public Company Method (“GPC”), along with descriptions of those guideline public companies.

The second method under the Market Approach is the Similar Transaction Method (also sometimes called Guideline Transaction Method or (confusingly) Precedent Transaction Method). It estimates FMV by comparing your business to similar businesses that have been sold.

The third method used is the Precedent Transaction Method (PTM). It begins by examining a company’s recent securities transaction, such as the sale of Series A Preferred equity, to deduce an overall value for the company and its entire capital structure.

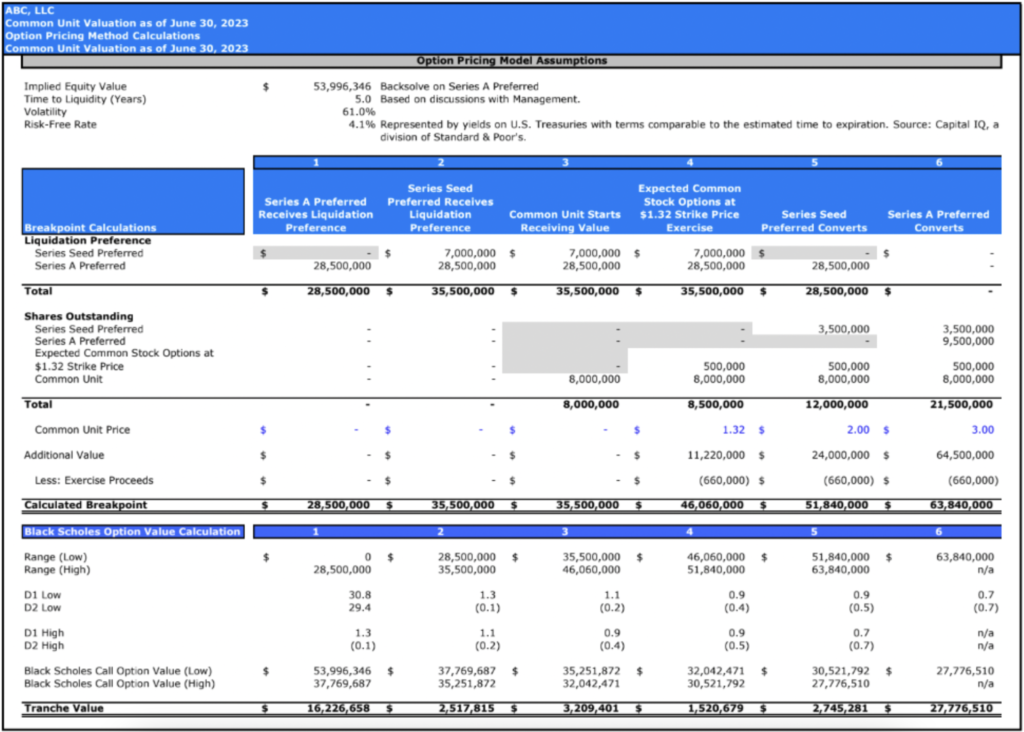

This method involves using the Options Pricing Model, informed by the Black-Scholes framework, to incorporate various elements like the rights and preferences of all securities, the total number of outstanding securities, and the recent transaction’s per-share price.

Specifically, it ‘backsolves’ for the implied equity value that aligns the Series A Preferred’s issue price with its fair market value.

This approach is based on the rationale that the recent Series A transaction, being an arms-length deal, accurately reflects the fair market value, assuming that investors are neither overpaid nor underpaid.

The chart below provides the setup of the method, including its assumptions:

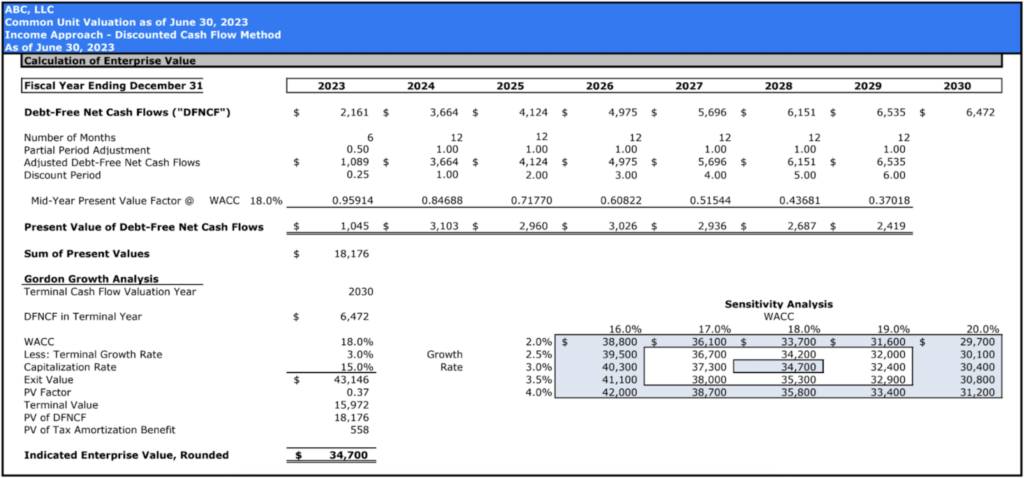

The next section covers the Income Approach, using the Discounted Cash Flow (DCF) Method:

This section is long and can look overwhelming at first glance. But it’s important that the reasonable methodologies used, and assumptions made, are clearly shown.

Think back to when you took math exams at school and had to show your work. It’s essentially the same thing. By showing your work, you’re communicating that you know how to get to the answer, and that you haven’t taken any unreasonable steps to get there (i.e., you have “reasonably applied” the valuation method). This is important for Safe Harbor.

Where possible, we use a combination of methodologies to come to the FMV indication. That’s why this 409A report example shows two approaches applied: the Market Approach (three separate methods under the market approach!) and the Income Approach, which utilizes the Discounted Cash Flow analysis.

The DCF (DCF) Method, a key method under the Income Approach, determines a company’s Fair Market Value (FMV) by projecting its future earnings and discounting them to present value to account for risk and the time value of money.

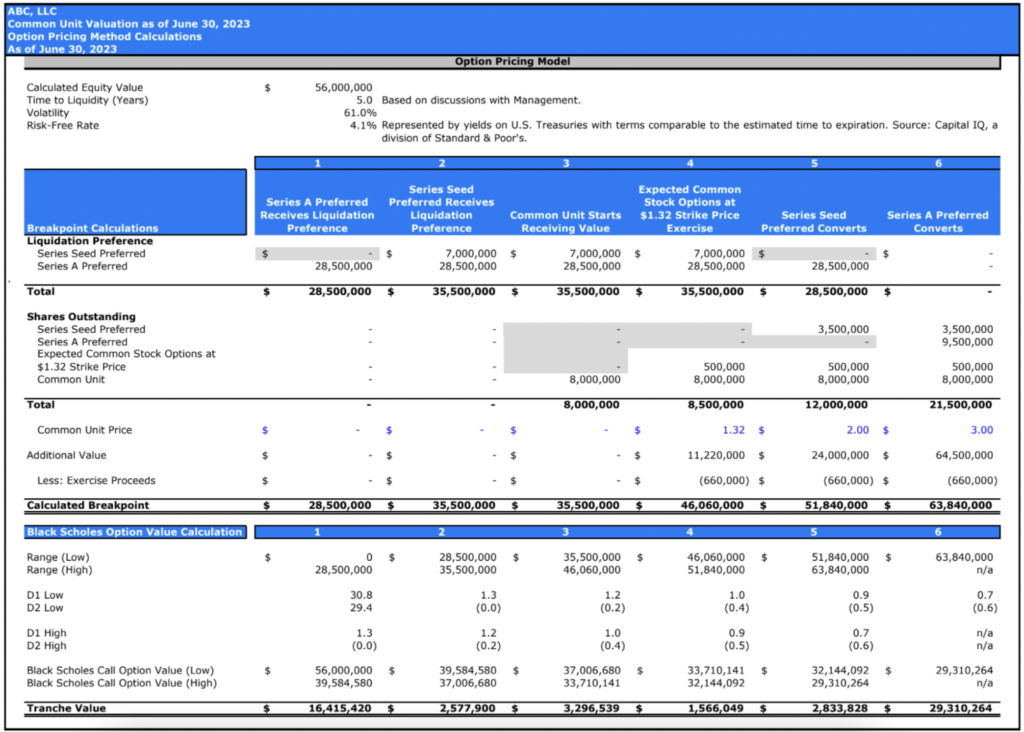

In a nutshell: This section provides a concise overview of the calculations applied in the Option Pricing allocation method, illustrating how the company’s total value – $56 million in our case – is distributed among various equity types, including Series Seed Preferred, Series A Preferred, upcoming Common Stock Options, and Common Units.

The allocation method considers specific factors such as liquidation preferences, dividend rights, and conversion privileges, alongside risk factors like volatility and opportunity cost (using US Treasury securities as the risk-free rate), and the element of time.

Below is the model’s first page from our 409A valuation example report:

The next section of the model expands on the capitalization table, detailing it for each valuation breakpoint.

This section highlights that not all classes of securities are affected equally in the valuation waterfall. Particularly, “preferred” securities are given this name due to their “preferences” over “common” in the distribution hierarchy.

Helpful Tip: A “breakpoint” in a company’s equity “waterfall” marks where the division of equity value shifts among different securities, such as preferred and common stock. Triggered by contractual terms (like liquidation preferences and exercise prices), these breakpoints affect each security type’s value uniquely. They signify where equity distribution rules change, crucial in complex structures with various securities. |

The accompanying chart details how each equity class is impacted at distinct valuation levels, with precise breakpoint calculations illustrating the varied effects on these classes at each threshold or “tranche” (i.e., Tranche 1, Tranche 2, etc.).

Additionally, the model calculates the Black-Scholes option values for each tranche, offering vital insights into the complex financial dynamics at play across the company’s valuation spectrum.

This analysis is key to getting a handle on how equity is distributed among stakeholders under varying valuation scenarios.

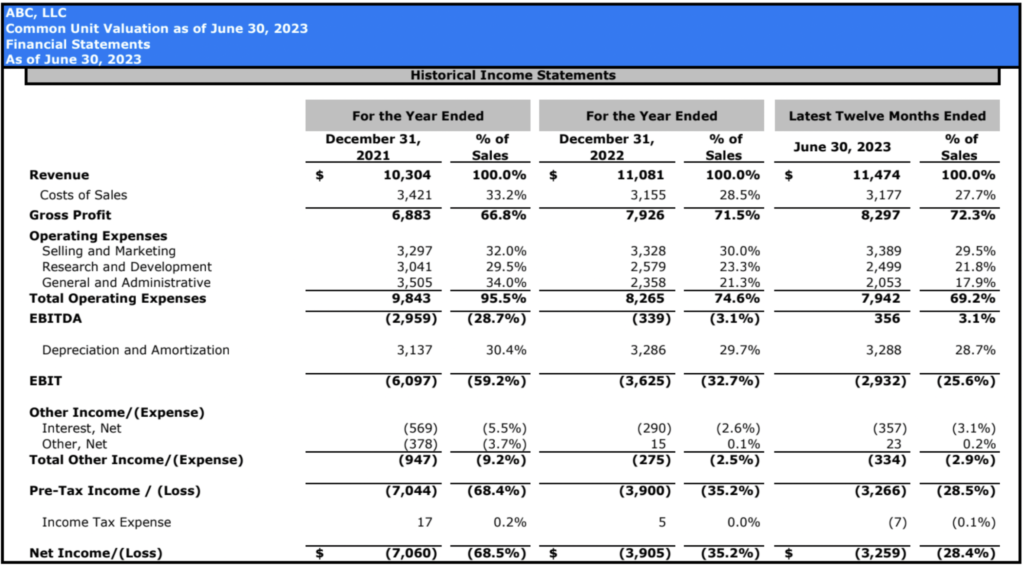

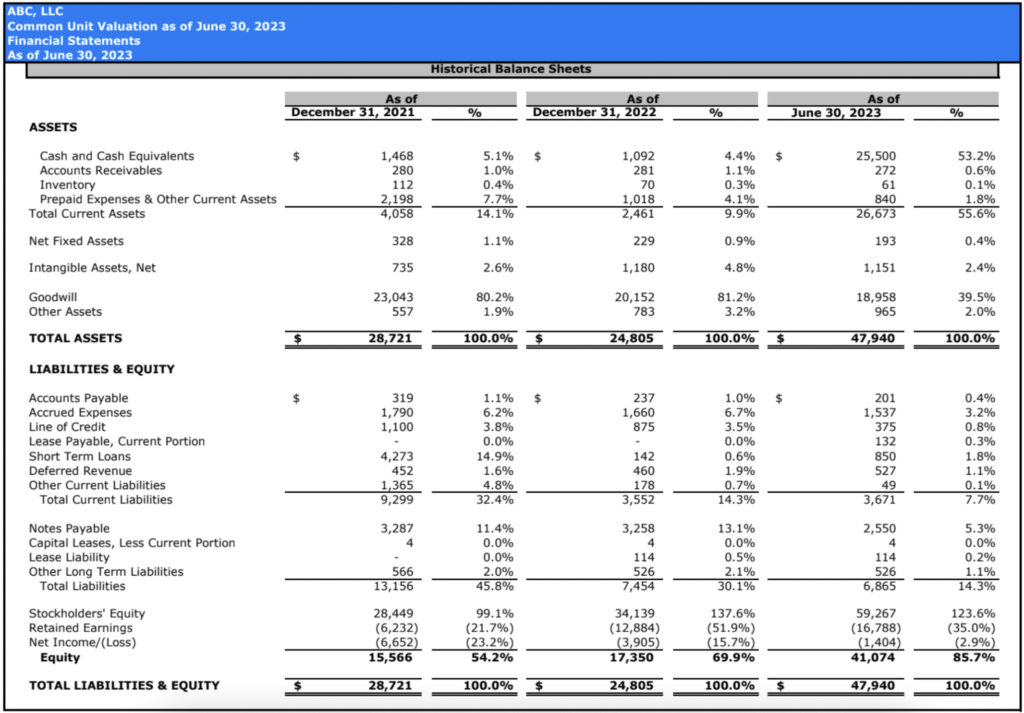

In a nutshell: In this section of the valuation report sample, you’ll find all of the secondary information used to inform the valuation (such as your company financials).

This section includes:

Think of the supporting exhibits as an appendix to the valuation calculation pages. They contain all of the information that helped inform which methodologies we chose and the application of those methodologies as it relates to the company being valued.

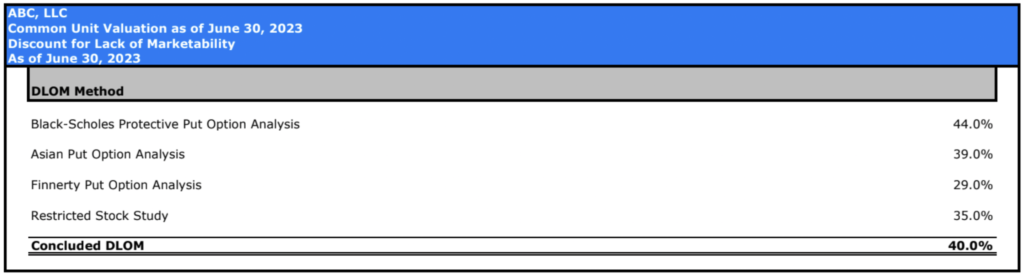

This section also includes the vital calculation of the Discount for Lack of Marketability (DLOM). The DLOM is applied to account for the reduced liquidity associated with private company securities, which are not as readily marketable as public company stocks.

This discount reflects the relative difficulty and uncertainty in selling such securities and the longer time frames often required to find a buyer.

Calculating the DLOM involves assessing factors like the company’s size, the rights and restrictions associated with the securities, the holding period, and the general market conditions.

Including the DLOM in our valuation model ensures a more accurate and realistic assessment of the company’s common equity, recognizing the inherent challenges in liquidating private securities.

Helpful hint: Ensure your 409A valuation report is signed by the provider, as an unsigned report may lack validity and safe harbor protection. This necessity is underscored by the Tax Court’s ruling in Estate of Hoensheid v. Comm’r (In re Estate of Hoensheid), T.C. Memo 2023-34, which stipulates that a “qualified appraisal” must be signed and dated by a qualified appraiser. Unsigned reports risk non-compliance with tax regulations, potentially jeopardizing the safe harbor status of any related grants. |

Every now and again, a company’s valuation makes headlines—either because it’s high or faltering. When that happens it allows us to look at what’s happened and why.

Three recent company valuations that landed on TechCrunch are Stripe, Instacart, and X (formerly Twitter). Let’s look at each one in turn to see what occurred and why.

Founded in 2010 and boasting 12 million in revenue as of 2021, Stripe is a fintech automating financial processes for businesses.

Following a 409A valuation in 2022, Stripe’s valuation was slashed by 28%. The 409A valuation was brought on by the 2022 stock market decline which was categorized as a “Material Event” for the business.

Many businesses would have lost value as a result of the economic decline, so Stripe’s valuation isn’t surprising.

Instacart faced a similar devaluation off the back of a 409A in 2021. It dropped 38.5%, taking the company’s valuation from $39 billion to $24 billion.

This devaluation was an objective reflection of how market changes had impacted the grocery delivery platform.

The company cited “market turbulence” and the need to attract talent as key reasons for reassessing its valuation.

This adjustment also reflected a steep drop in the sales growth rate since the start of the pandemic, a period when demand for grocery delivery had surged.

Additionally, the changing landscape of deliveries in the food and other sectors, and the challenges associated with the gig economy’s infrastructure for full-time vehicle drivers, contributed to this reassessment.

Other companies in similar sectors, like advertising and delivery, also experienced declines in stock value around this time

This devaluation, while indicative of market shifts impacting Instacart’s business, has a silver lining: it potentially reduces the tax obligations for employees exercising their stock options, as 409A valuations directly influence the taxation of an exercise.

A lower 409A FMV could also enable management to offer enticing retention grants or even recruit more talent with a lower, more attractive, exercise price on their stock options.

Elon Musk’s acquisition of Twitter in late 2022 for about $44 billion was followed by a notable drop in its valuation to $19 billion a year later, as per a 409A valuation. This stark reduction led to speculation about Musk’s leadership impact.

Unlike companies like Instacart and Stripe, whose valuations seemingly were affected by broader market changes, social media platforms, in general, had not faced similar valuation declines.

However, that sharp drop in Twitter’s valuation after Musk’s acquisition might have had a silver lining for employees with stock options.

Just as in the scenarios above, a lower 409A Fair Market Value (FMV) could have reduced their tax obligations when exercising options, as 409A valuations directly affect such taxes when an option is exercised.

Additionally, the lower valuation might have allowed the company to offer more appealing retention grants and attract new talent with attractively priced stock options.

However, more recent reports indicate that X’s valuation has rebounded toward its original $44 billion purchase price.

Eton Venture Services is the trusted choice for startups and law firms that demand precision in every 409A valuation.

Our team brings Big-4 rigor to every engagement, and with over 10,000 valuations completed, we know what it takes to deliver reports that hold up under IRS and audit scrutiny.

But we also know founders need more than technical accuracy. They need speed, clarity, and a partner who actually picks up the phone.

That’s why we offer turnaround in as little as one day and work directly with you to make sure your report is defensible, compliant, and easy to understand.

Contact us today to get your 409A valuation report.

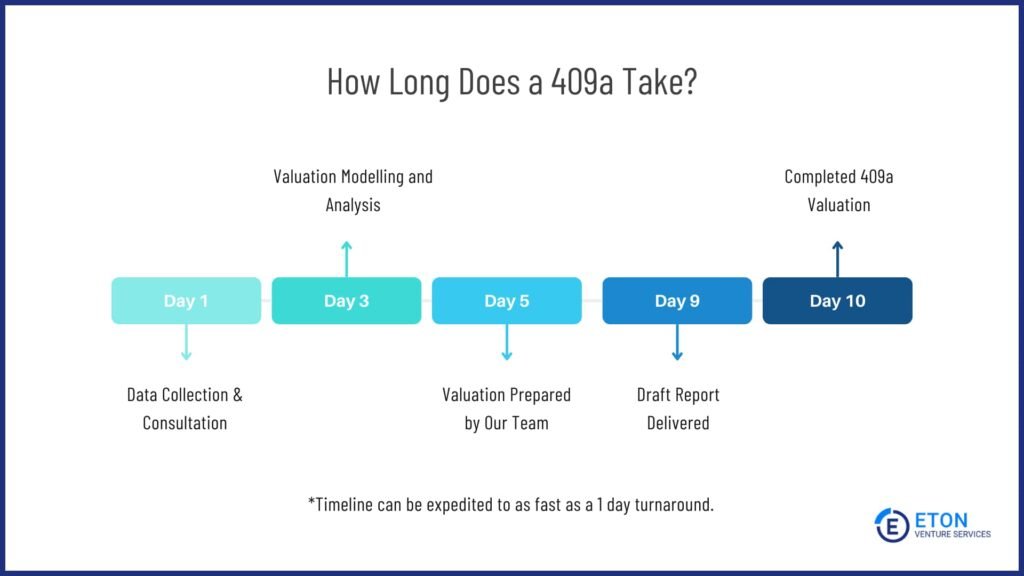

At Eton, 409A valuations never take longer than 10 days from the receipt of all requested documents and information.

If you need a valuation sorted faster, we can accommodate that for an additional fee.

Those 10 days (or less) include a consultation, a thorough analysis of your company and the market, preparation of the valuation draft, a review process, and a final, signed narrative 409A valuation report with calculation pages.

For a full breakdown of how long 409A valuations can take and the factors that influence different timelines, read our article: How Long Does a 409A Valuation Take?