Pensions Valuation Divorce: 5 Steps to Value Your Pension Plan

Business Valuation in Divorce, Valuation

Written by Chris Walton, JD

Chris Walton, JD

President & CEO

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, legal counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.

Chris has led thousands of valuations, including for equity securities, intangible assets, financial instruments, investment valuations, business valuations for tax compliance and financial reporting compliance, as well as fairness and solvency opinions.

Navigating a divorce is never easy, emotionally or logistically. And when major assets like pensions enter the picture, things can get even more complicated.

For many couples, a pension is one of the most valuable assets on the table. Properly valuing it is essential to reaching a fair settlement, especially since pension benefits are often paid years into the future. A pension valuation for divorce determines the present value of those future benefits so they can be divided accurately and equitably.

In this guide, we break down:

The key factors that affect pension valuation in divorce

How to value a pension for divorce, step by step

How long pension valuations take and what documents are required

Whether you’re early in the divorce process or preparing for settlement discussions, understanding how pension valuation works will help you protect your financial interests and avoid costly mistakes.

Key Takeaways:

A pension can be one of the most valuable assets in a divorce, even though the money may not be paid for years. Getting the value right matters because it directly affects how the rest of the settlement is balanced.

How a pension is valued in divorce depends on several factors, including the type of pension plan, when benefits were earned, retirement timing, and the legal rules in the state where the divorce is handled.

In most divorces, only the portion of the pension earned during the marriage is divided, which means when the pension was earned is just as important as how much it’s worth.

Why Do You Need to Value Pensions During a Divorce?

When going through a divorce, marital assets must be identified and divided between both parties. This includes obvious assets like the family home and vehicles, but also retirement accounts and pensions accumulated over the course of the marriage.

Below are examples of assets that need to be divided during a divorce:

For many couples, pensions represent a significant share of total net worth. Ignoring them, or valuing them incorrectly, can materially distort a divorce settlement.

However, unlike many other assets, certain pensions don’t have a clear market value you can look up. Instead, valuing them requires navigating multiple variables, including:

Future benefit payouts and retirement age assumptions

Life expectancy and mortality tables

Discount rates used to calculate present value

Plan-specific rules and benefit formulas

This is why pension valuation for divorce is far more complex than dividing a savings account or investment portfolio.

There are also important legal considerations. For example, pension division rules differ by jurisdiction:

Some states treat pensions as fully joint property, often split evenly

Others divide only the portion earned during the marriage

Some require immediate offsets, while others defer division until retirement

Whoever values the pension must understand not just financial modeling, but also the legal framework governing your divorce.

Because pension valuation combines actuarial assumptions, financial modeling, and legal context, most divorcing couples rely on an independent expert.

At Eton, we provide impartial, court-defensible pension valuations backed by over 15 years of experience and Big Four–trained valuation professionals. Our work is designed to hold up under scrutiny and support equitable outcomes for both parties.

If you’re navigating a divorce and need clarity around valuing a pension, we can guide you through the process with a defensible valuation you can rely on.

🤔 Did you know? Business owners facing divorce also need to get their business valued. This is a service Eton offers which we can do alongside a pension valuation.

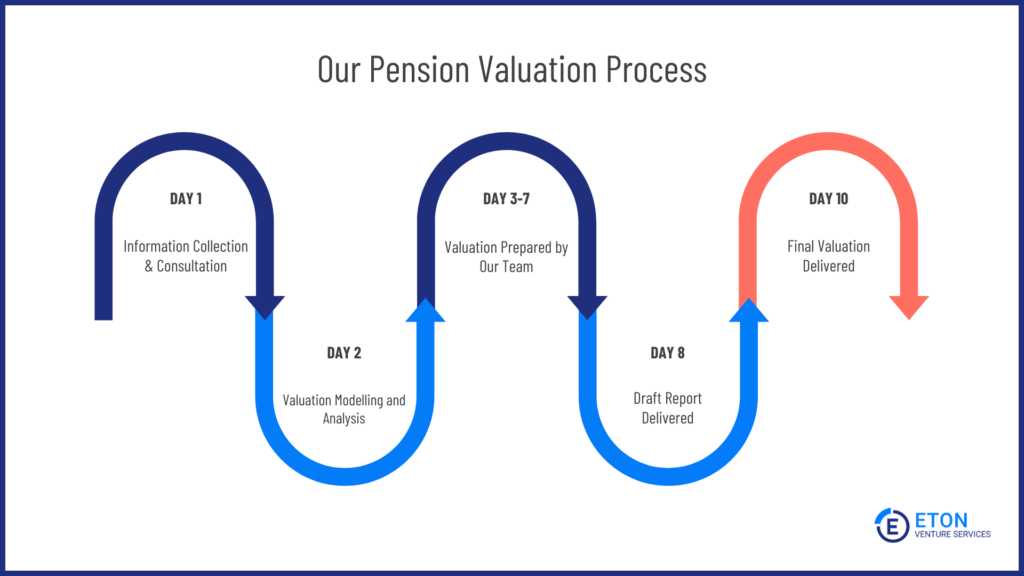

The timeline for a pension valuation for divorce depends on the complexity of the plan, the type of pension involved, and how quickly the required documents can be provided. That said, when the information is available, the process does not need to take weeks or months.

At Eton, we typically complete a pension valuation within 10 days of receiving the necessary documentation.

For time-sensitive divorce matters, expedited timelines are available, although we always require at least one business day from document submission to ensure the valuation is accurate and defensible.

This is what a typical pension valuation process looks like:

Generally, turnaround times can vary widely across valuation firms:

Larger firms often have multiple internal review layers and handoffs, which can slow the process.

Smaller firms may move faster but sometimes lack the in-house expertise required to efficiently handle more complex pension plans, particularly defined benefit pensions.

Because Eton operates as a boutique firm with Big Four-trained professionals, pension valuations are handled directly by senior experts from start to finish, without unnecessary handoffs or automation.

This allows us to move efficiently without compromising the rigor required for a court-defensible pension valuation.

If timing matters in your divorce, we can help you get a reliable pension valuation on a timeline that supports your case. Reach out to us here.

Before moving forward with a pension valuation for divorce, there are a few fundamentals you need to understand. These factors determine how a pension is valued and how much of it is subject to division.

Factor 1. The Type of Pension Plan

The valuation process depends heavily on the type of pension involved. Broadly, pension plans fall into two categories:

defined benefit plans

defined contribution plans

Defined benefit plans provide a fixed payout in retirement based on a formula, typically comprising years of service and compensation. Examples include:

traditional pensions

cash balance plans

some government/military plans

Because these plans pay benefits in the future, valuing them means estimating what those future payments are worth today. This involves accounting for factors like when payments begin, how long they’re expected to last, and the specific rules of the pension plan itself.

Defined contribution plans, like 401(k)s and 403(b)s, have no guaranteed payout. Instead, their value depends on contributions made and investment performance over time.

In divorce, these plans are usually valued based on account balances as of a defined date, making them far more straightforward to assess.

Factor 2. Whether It’s Separate Property or Marital Property

Not all pension benefits are always subject to division

In most states, only the portion of pension benefits earned during the marriage is considered marital/community property.

Contributions earned before the marriage are generally treated as separate property and excluded from the division process.

This distinction matters, because even a modest error in classifying service periods can materially change the outcome of a settlement.

To isolate the marital portion, we rely on established methods like:

Segregation method: Calculates the separate property portion first and deducts it from the total present value

Subtraction method: Calculates the present value of benefits earned as of separation, then subtracts the present value of benefits earned as of marriage

Coverture fraction: Uses a ratio of marital service years to total service years to determine the marital share

Factor 3. What State Laws and Regulations May Apply

State law ultimately governs how pensions are treated in divorce, and the rules vary significantly across jurisdictions:

Some states follow a deferred distribution approach, where the marital portion of the pension is divided when benefits are actually paid.

Others require an immediate offset, where the present value of the pension is calculated and balanced against other marital assets at settlement.

There are also state-specific exclusions and nuances.

For example, Illinois excludes certain disability pension benefits from marital property and has special treatment rules for some government pensions. New York, on the other hand, treats any pension benefits earned during the marriage as marital property subject to division.

Because these rules affect both valuation methodology and division mechanics, pension valuation must align with applicable statutes and case law.

An experienced valuation firm like Eton will ensure compliance with applicable state statutes and precedents to deliver an airtight, court-admissible, and equitable pension valuation.

How to Value a Pension for Divorce [5 Steps]

There are very few people who should take it upon themselves to value their pension during a divorce.

The process is technically detailed and context-specific, requiring expertise most people don’t have. It also requires impartiality for the valuation to be accurate and defensible.

For that reason, most people choose to work with an independent valuation firm like Eton to handle the process end to end.

A reputable, court-experienced provider can ensure the pension is valued correctly and in line with legal requirements, rather than leaving room for disputes later on.

That said, understanding how pension valuation works is still valuable, even if you ultimately rely on a professional.

The steps below outline the standard process experts follow when valuing a pension for divorce, so you know what’s involved and what to expect.

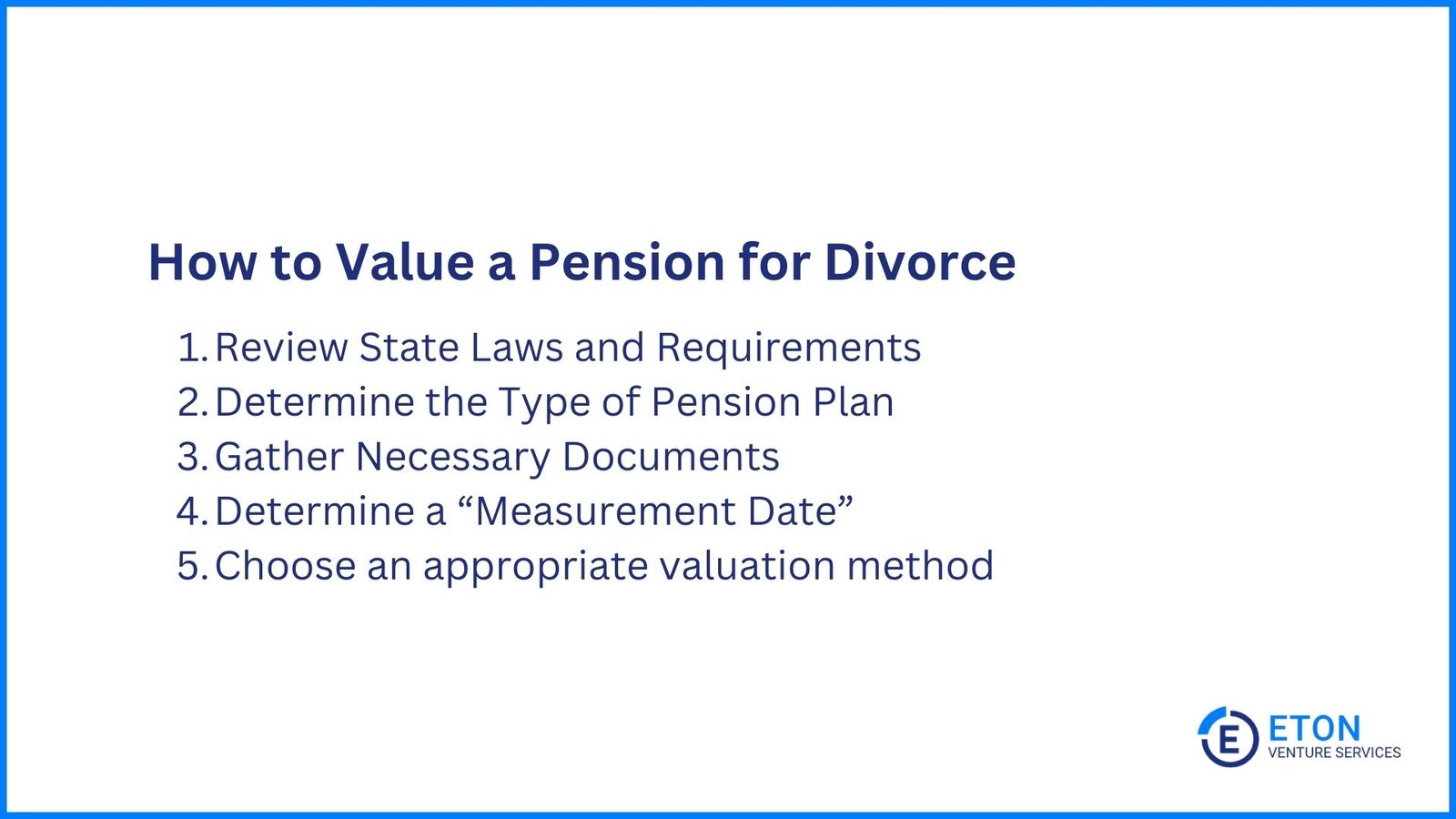

Step 1. Review State Laws and Requirements

As previously noted, where you’re getting divorced plays a role in how your pension is valued and divided.

Some states may require the pension to be split equally, while others consider the length of the marriage and other factors.

Experienced valuation experts well-versed in state-specific pension division rules account for those legal frameworks at the outset to ensure the analysis proceeds on the right basis.

See factor 3 (What State Laws and Regulations May Apply) above for more information.

Step 2. Determine the Type of Pension Plan

We shared earlier that pensions can be classified into two main types: defined benefit plans and defined contribution plans.

A defined benefit plan provides a specific monthly payment upon retirement, while a defined contribution plan’s payout depends on the contributions and the plan’s investment performance.

Because of these differences, the valuation of a defined benefit pension follows a very different approach than a defined contribution plan. That’s why clarifying the plan type upfront is critical to the process.

Step 3. Gather Necessary Documents

The next step in conducting a reliable pension valuation for divorce is collecting and reviewing a set of essential documents, including:

Benefit plan descriptions and amendments

Current and historical benefits statements

Employee data like hire date, birth date, compensation

Actuarial reports and plan asset statements

Domestic relations orders and divorce decrees (if applicable)

These documents provide the information needed to assess the pension’s value accurately.

Step 4. Determine a “Measurement Date”

The “measurement date” refers to the specific point in time for which the present value of pension assets or liabilities will be calculated.

Because the present value of a pension can fluctuate based on factors like interest rates and actuarial assumptions, selecting an appropriate measurement date is an important part of the process.

This date may be determined by state law, court order, or agreement between both parties and their counsel.

Common valuation dates include the date of legal separation, the date the divorce petition is filed, and sometimes the date of trial or final divorce decree, depending on jurisdiction and the specifics of the case.

The goal is to establish a fair, clearly defined reference point from which all pension valuation calculations are performed.

Step 5. Choose an appropriate valuation method

There are different methods used when valuing a pension for divorce, and the appropriate approach depends on the type of pension involved and the legal framework governing the case.

For Defined Contribution Plans (401(k), 403(b), IRAs)

Valuation is straightforward. The value is simply the account balance as of the valuation date, no complex calculations required.

The main consideration here is determining the marital portion using methods like coverture, segregation, or subtraction (as discussed earlier).

For Defined Benefit Plans (Traditional Pensions)

Valuation is far more complex because these plans pay future monthly benefits rather than providing a lump sum. To determine what those future payments are worth today, we must calculate the present value using two key inputs:

Mortality tables: Statistical data that estimates how long the pension holder is likely to live (and therefore how many payments they’ll receive)

Discount rate: An interest rate used to convert future dollars into today’s dollars

Here’s how it works:

For each future year of pension payments, we calculate the value today by multiplying the expected payment by the probability the person will be alive that year, then discounting it based on how far in the future it will be paid. These yearly values are then added together to arrive at the total present value.

Different valuation methods use different mortality tables and discount rates, which can result in significantly different values, sometimes varying by $50,000 to $100,000 or more for the same pension.

Common valuation methods for defined benefit plans include:

GATT Method

Uses GAM 83 mortality tables and the 30-Year Treasury Bond rate

One of the most common methods in divorce cases

Reflects current market conditions through publicly available Treasury rates

PBGC Method

Uses GAM 83 mortality tables (or newer Pri-2012 tables) and interest rates published by the Pension Benefit Guaranty Corporation

Tends to produce higher valuations because PBGC rates are typically lower

Preferred in some jurisdictions as a conservative government standard

IRC 417 Method

Uses RP-2014 mortality tables and three “segment rates” published monthly by the IRS

Most sophisticated approach, applies different discount rates for payments expected in years 1-5, years 6-20, and beyond year 20

Required by law for certain pension calculations and often preferred for accuracy

Life Expectancy Method

Uses simplified life expectancy tables and municipal bond rates

Faster but less precise, can be off by as much as 20% in either direction

Sometimes used for quick estimates rather than court-ready valuations

Valuation experts select the method that aligns with the pension’s structure, plan provisions, and applicable legal standards, applying informed judgment to ensure the valuation will hold up under scrutiny.

Need a Quick Estimate of Your Pension’s Worth? Use Our Free Divorce Pension Calculator

Use our free divorce pension calculator below to get a quick estimate based on the valuation concepts discussed above.

It shows what a defined benefit pensionmay be worth in today’s dollars and how much of that value could be considered marital property.

This is a helpful starting point for planning, settlement discussions, and sanity-checking numbers, especially if you have a recent benefit statement or a reasonable estimate of the monthly pension amount at retirement.

However, please note that the calculator provides an estimate for educational and informational purposes only. It uses simplified assumptions, IRS-published discount rates (IRC 417(e) segment rates), and a standard mortality table.

Actual pension valuations for divorce proceedings often require additional analysis, including:

Plan-specific rules and provisions

Survivor benefit options

Early retirement reduction factors

Post-retirement death benefits

Jurisdiction-specific valuation requirements

Pension plan amendments or benefit changes

Hence, a simplified pension calculator for divorce does not constitute legal advice, financial advice, or actuarial services, and the results should not be used as the sole basis for property division decisions.

Generally, turnaround times can vary widely across valuation firms:

Larger firms often have multiple internal review layers and handoffs, which can slow the process.

Smaller firms may move faster but sometimes lack the in-house expertise required to efficiently handle more complex pension plans, particularly defined benefit pensions.

Because Eton operates as a boutique firm with Big Four-trained professionals, pension valuations are handled directly by senior experts from start to finish, without unnecessary handoffs or automation.

This allows us to move efficiently without compromising the rigor required for a court-defensible pension valuation.

If timing matters in your divorce, we can help you get a reliable pension valuation on a timeline that supports your case. Reach out to us here.

Before moving forward with a pension valuation for divorce, there are a few fundamentals you need to understand. These factors determine how a pension is valued and how much of it is subject to division.

Factor 1. The Type of Pension Plan

The valuation process depends heavily on the type of pension involved. Broadly, pension plans fall into two categories:

defined benefit plans

defined contribution plans

Defined benefit plans provide a fixed payout in retirement based on a formula, typically comprising years of service and compensation. Examples include:

traditional pensions

cash balance plans

some government/military plans

Because these plans pay benefits in the future, valuing them means estimating what those future payments are worth today. This involves accounting for factors like when payments begin, how long they’re expected to last, and the specific rules of the pension plan itself.

Defined contribution plans, like 401(k)s and 403(b)s, have no guaranteed payout. Instead, their value depends on contributions made and investment performance over time.

In divorce, these plans are usually valued based on account balances as of a defined date, making them far more straightforward to assess.

Factor 2. Whether It’s Separate Property or Marital Property

Not all pension benefits are always subject to division

In most states, only the portion of pension benefits earned during the marriage is considered marital/community property.

Contributions earned before the marriage are generally treated as separate property and excluded from the division process.

This distinction matters, because even a modest error in classifying service periods can materially change the outcome of a settlement.

To isolate the marital portion, we rely on established methods like:

Segregation method: Calculates the separate property portion first and deducts it from the total present value

Subtraction method: Calculates the present value of benefits earned as of separation, then subtracts the present value of benefits earned as of marriage

Coverture fraction: Uses a ratio of marital service years to total service years to determine the marital share

Factor 3. What State Laws and Regulations May Apply

State law ultimately governs how pensions are treated in divorce, and the rules vary significantly across jurisdictions:

Some states follow a deferred distribution approach, where the marital portion of the pension is divided when benefits are actually paid.

Others require an immediate offset, where the present value of the pension is calculated and balanced against other marital assets at settlement.

There are also state-specific exclusions and nuances.

For example, Illinois excludes certain disability pension benefits from marital property and has special treatment rules for some government pensions. New York, on the other hand, treats any pension benefits earned during the marriage as marital property subject to division.

Because these rules affect both valuation methodology and division mechanics, pension valuation must align with applicable statutes and case law.

An experienced valuation firm like Eton will ensure compliance with applicable state statutes and precedents to deliver an airtight, court-admissible, and equitable pension valuation.

How to Value a Pension for Divorce [5 Steps]

There are very few people who should take it upon themselves to value their pension during a divorce.

The process is technically detailed and context-specific, requiring expertise most people don’t have. It also requires impartiality for the valuation to be accurate and defensible.

For that reason, most people choose to work with an independent valuation firm like Eton to handle the process end to end.

A reputable, court-experienced provider can ensure the pension is valued correctly and in line with legal requirements, rather than leaving room for disputes later on.

That said, understanding how pension valuation works is still valuable, even if you ultimately rely on a professional.

The steps below outline the standard process experts follow when valuing a pension for divorce, so you know what’s involved and what to expect.

Step 1. Review State Laws and Requirements

As previously noted, where you’re getting divorced plays a role in how your pension is valued and divided.

Some states may require the pension to be split equally, while others consider the length of the marriage and other factors.

Experienced valuation experts well-versed in state-specific pension division rules account for those legal frameworks at the outset to ensure the analysis proceeds on the right basis.

See factor 3 (What State Laws and Regulations May Apply) above for more information.

Step 2. Determine the Type of Pension Plan

We shared earlier that pensions can be classified into two main types: defined benefit plans and defined contribution plans.

A defined benefit plan provides a specific monthly payment upon retirement, while a defined contribution plan’s payout depends on the contributions and the plan’s investment performance.

Because of these differences, the valuation of a defined benefit pension follows a very different approach than a defined contribution plan. That’s why clarifying the plan type upfront is critical to the process.

Step 3. Gather Necessary Documents

The next step in conducting a reliable pension valuation for divorce is collecting and reviewing a set of essential documents, including:

Benefit plan descriptions and amendments

Current and historical benefits statements

Employee data like hire date, birth date, compensation

Actuarial reports and plan asset statements

Domestic relations orders and divorce decrees (if applicable)

These documents provide the information needed to assess the pension’s value accurately.

Step 4. Determine a “Measurement Date”

The “measurement date” refers to the specific point in time for which the present value of pension assets or liabilities will be calculated.

Because the present value of a pension can fluctuate based on factors like interest rates and actuarial assumptions, selecting an appropriate measurement date is an important part of the process.

This date may be determined by state law, court order, or agreement between both parties and their counsel.

Common valuation dates include the date of legal separation, the date the divorce petition is filed, and sometimes the date of trial or final divorce decree, depending on jurisdiction and the specifics of the case.

The goal is to establish a fair, clearly defined reference point from which all pension valuation calculations are performed.

Step 5. Choose an appropriate valuation method

There are different methods used when valuing a pension for divorce, and the appropriate approach depends on the type of pension involved and the legal framework governing the case.

For Defined Contribution Plans (401(k), 403(b), IRAs)

Valuation is straightforward. The value is simply the account balance as of the valuation date, no complex calculations required.

The main consideration here is determining the marital portion using methods like coverture, segregation, or subtraction (as discussed earlier).

For Defined Benefit Plans (Traditional Pensions)

Valuation is far more complex because these plans pay future monthly benefits rather than providing a lump sum. To determine what those future payments are worth today, we must calculate the present value using two key inputs:

Mortality tables: Statistical data that estimates how long the pension holder is likely to live (and therefore how many payments they’ll receive)

Discount rate: An interest rate used to convert future dollars into today’s dollars

Here’s how it works:

For each future year of pension payments, we calculate the value today by multiplying the expected payment by the probability the person will be alive that year, then discounting it based on how far in the future it will be paid. These yearly values are then added together to arrive at the total present value.

Different valuation methods use different mortality tables and discount rates, which can result in significantly different values, sometimes varying by $50,000 to $100,000 or more for the same pension.

Common valuation methods for defined benefit plans include:

GATT Method

Uses GAM 83 mortality tables and the 30-Year Treasury Bond rate

One of the most common methods in divorce cases

Reflects current market conditions through publicly available Treasury rates

PBGC Method

Uses GAM 83 mortality tables (or newer Pri-2012 tables) and interest rates published by the Pension Benefit Guaranty Corporation

Tends to produce higher valuations because PBGC rates are typically lower

Preferred in some jurisdictions as a conservative government standard

IRC 417 Method

Uses RP-2014 mortality tables and three “segment rates” published monthly by the IRS

Most sophisticated approach, applies different discount rates for payments expected in years 1-5, years 6-20, and beyond year 20

Required by law for certain pension calculations and often preferred for accuracy

Life Expectancy Method

Uses simplified life expectancy tables and municipal bond rates

Faster but less precise, can be off by as much as 20% in either direction

Sometimes used for quick estimates rather than court-ready valuations

Valuation experts select the method that aligns with the pension’s structure, plan provisions, and applicable legal standards, applying informed judgment to ensure the valuation will hold up under scrutiny.

Need a Quick Estimate of Your Pension’s Worth? Use Our Free Divorce Pension Calculator

Use our free divorce pension calculator below to get a quick estimate based on the valuation concepts discussed above.

It shows what a defined benefit pensionmay be worth in today’s dollars and how much of that value could be considered marital property.

This is a helpful starting point for planning, settlement discussions, and sanity-checking numbers, especially if you have a recent benefit statement or a reasonable estimate of the monthly pension amount at retirement.

However, please note that the calculator provides an estimate for educational and informational purposes only. It uses simplified assumptions, IRS-published discount rates (IRC 417(e) segment rates), and a standard mortality table.

Actual pension valuations for divorce proceedings often require additional analysis, including:

Plan-specific rules and provisions

Survivor benefit options

Early retirement reduction factors

Post-retirement death benefits

Jurisdiction-specific valuation requirements

Pension plan amendments or benefit changes

Hence, a simplified pension calculator for divorce does not constitute legal advice, financial advice, or actuarial services, and the results should not be used as the sole basis for property division decisions.

Pension Valuation Calculator for Divorce Proceedings

Is This Calculator Right for You?

This calculator is for defined benefit pension plans that promise a specific monthly payment at retirement (for example, "$3,500 per month starting at age 65").

If you have a defined contribution plan (401k, 403b, IRA) with a current account balance, you don't need this calculator. Those are valued at the account balance on the separation date.

This is the portion of the pension earned during the marriage.

Important note: This calculator assumes pension payments remain constant over time (no annual increases). If your pension includes automatic annual cost-of-living adjustments (COLA), the actual value will be higher than shown here. For a precise valuation that accounts for COLA and other pension-specific features, contact Eton Venture Services.

Our Pension Valuation Services

Divorce already comes with enough complexity. Pension valuation shouldn’t be another source of confusion or conflict.

Whether you need a straightforward pension valuation or are dealing with a more complex defined benefit plan, Eton provides reliable valuations you can use with confidence throughout the divorce process.

Our pension valuations are prepared by Big Four-trained professionals with deep experience in divorce and litigation contexts. With 10,000+ valuations completed, our team understands how these reports are reviewed, challenged, and relied on in real proceedings.

We pair that depth of experience with an efficient process, delivering speed without compromising rigor or defensibility.

If you’re navigating a divorce and want a pension valuation that supports a fair outcome without unnecessary headaches or delays, get in touch with us today.

Pension Valuation Divorce – FAQs

What percentage of my partner’s pension am I entitled to?

The percentage of your partner’s pension you’re entitled to after a divorce can vary quite a bit, depending on the state laws and the specific circumstances of your marriage and divorce.

It’s really important to understand that there isn’t a one-size-fits-all answer to this. Different states have different rules.

Generally, in many states, you might be entitled to a portion of the pension that was earned during the time of your marriage.

This doesn’t usually include the portion of the pension that was earned before you were married or after you separated.

As for the percentage, it can often range from 50% of the marital portion of the pension in community property states (like California and Texas) to a different percentage in equitable distribution states (like New York or Florida), where the court looks at what is fair, which might not always be a straight 50/50 split.

But these are just general guidelines. The actual percentage can be influenced by a lot of factors like the length of your marriage, other assets you and your partner have, and any agreements you might have made.

It’s really key to get advice from a legal professional in your state to understand exactly what you might be entitled to in your specific situation. They can give you the most accurate information based on your state’s laws and your individual circumstances.

Is my ex-partner entitled to my pension after divorce?

Generally, yes.

In the United States, the division of pensions in a divorce falls under state law, and most states consider pensions earned during a marriage as marital property that can be divided in a divorce.

However, the specific rules and methods of division can vary from state to state. Here are examples from a few states:

California: As a community property state, California typically divides all marital assets, including pensions, equally between spouses.

New York: New York follows an equitable distribution approach, meaning the court divides marital property in a way that is fair but not necessarily equal. This includes pensions earned during the marriage.

Texas: Similar to California, Texas is a community property state, and pensions are usually split evenly between the spouses.

Florida: In Florida, the court follows equitable distribution, meaning pensions are divided in a fair and equitable manner, though not always equally.

Illinois: Like many states, Illinois uses equitable distribution for dividing marital property, including pensions. The court considers various factors to determine a fair division.

These are just examples, and it’s important to understand that “equitable” does not always mean “equal.”

The division of pensions can be influenced by several factors, including the length of the marriage, the value of the pension, and other assets and income of each spouse.

It’s essential for anyone going through a divorce to seek legal advice specific to their state and situation to understand how their pension might be affected.

How much is my pension worth in divorce UK?

In the UK, the value of a pension in a divorce depends on various factors and can be quite complex.

The method for assessing a pension’s worth isn’t straightforward and hinges on considerations like the length of your marriage, both parties’ financial needs, and other shared assets.

There are different approaches to dealing with pensions in a divorce, such as ‘pension sharing’ where a part of your pension is transferred to your ex-partner, or ‘pension offsetting,’ where its value is balanced against other assets.

The type of pension you have (like defined benefit or defined contribution) also plays a key role in its valuation. A financial expert is often needed to determine the pension’s value, considering future payouts and other factors.

However, if you’d just like to have an idea of how much your pension is worth or work out how much you should pay out / receive during a divorce, this is a helpful resource: Pension Divorce Calculator

(Please note that this is not a substitute for legal advice.)

It’s crucial to get specialized advice from a financial advisor or a divorce solicitor, as they can provide guidance tailored to your specific situation, including the type of pension you have and your overall financial circumstances.

get in touch

Let's talk.

Schedule a free consultation meeting to discuss your valuation needs.

Written by Chris Walton, JD

Written by Chris Walton, JD