Written by Chris Walton, JD

Written by Chris Walton, JDAs companies and their finance teams approach their 409A renewal date, it is worth allocating a small amount of time to ensure the renewal process runs smoothly and aligns with key internal deadlines.

A closer look at the language of the regulation provides some important guidance: Treasury Reg. §1.409A-1(b)(5)(iv)(A) grants a safe harbor presumption — but only as long as no information has emerged since the valuation date that could materially affect the company’s value. That caveat is important to note.

A valuation from nine months ago can already be indefensible if the right things have changed. A valuation from four months ago can be rock solid. The 12-month window is a ceiling, not a guarantee — the IRS ultimately asks whether the exercise price reflects fair market value on the date of the grant, and a stale appraisal won’t answer that question.

That’s why it’s worth understanding what a renewal actually requires before you begin. The preparation is straightforward once you know what you’re assembling and why — and the companies that move fastest through the process are the ones that arrive at kickoff with a clear picture of what’s changed and a complete document package ready to go. This guide walks through both.

If Eton Venture Services performed your last 409A, we already have the baseline — the prior capital structure, the methodology applied, the comparable companies selected, the discount rates and scenario weightings used. A renewal doesn’t start from zero, but it isn’t a formality either. We will need to understand what’s changed since the last valuation date, and that assessment may lead to adjustments in methodology, comparables, or scenario weightings. The output is a new, independent conclusion as of a new date.

A 409A renewal asks three things of the client. Everything else — the analysis, the modeling, the report drafting, the comparable company screening — happens on our side.

Before kickoff, take ten minutes to inventory what’s changed since the last valuation date. Did you raise capital? Close a bridge round? Issue new SAFEs or convertible notes? Did the revenue trajectory shift — up or down? Did you hire a CRO who’s transforming the go-to-market motion, or lose a technical co-founder who was central to the product roadmap? Was a competitor acquired? Did the broader market reprice your sector? Any of these can constitute the kind of intervening information that erodes safe harbor protection — and material events we don’t know about can’t be reflected in the valuation.

It’s worth noting where the risk lands: the §409A penalties fall on the employee — a 20% additional tax plus premium interest — for a decision they had no part in making. Accuracy here matters beyond compliance.

The data request includes a set of qualitative assessment questions that feed directly into the discount rates, probability weightings, and scenario analyses. These should be completed by someone with real strategic visibility — usually the CEO or CFO. The answers should reflect management’s actual view, not the upside case from the last fundraise deck.

The full assessment covers additional dimensions including competitive positioning, customer concentration, geographic dependence, and product-market fit — you’ll receive the complete questionnaire before kickoff.

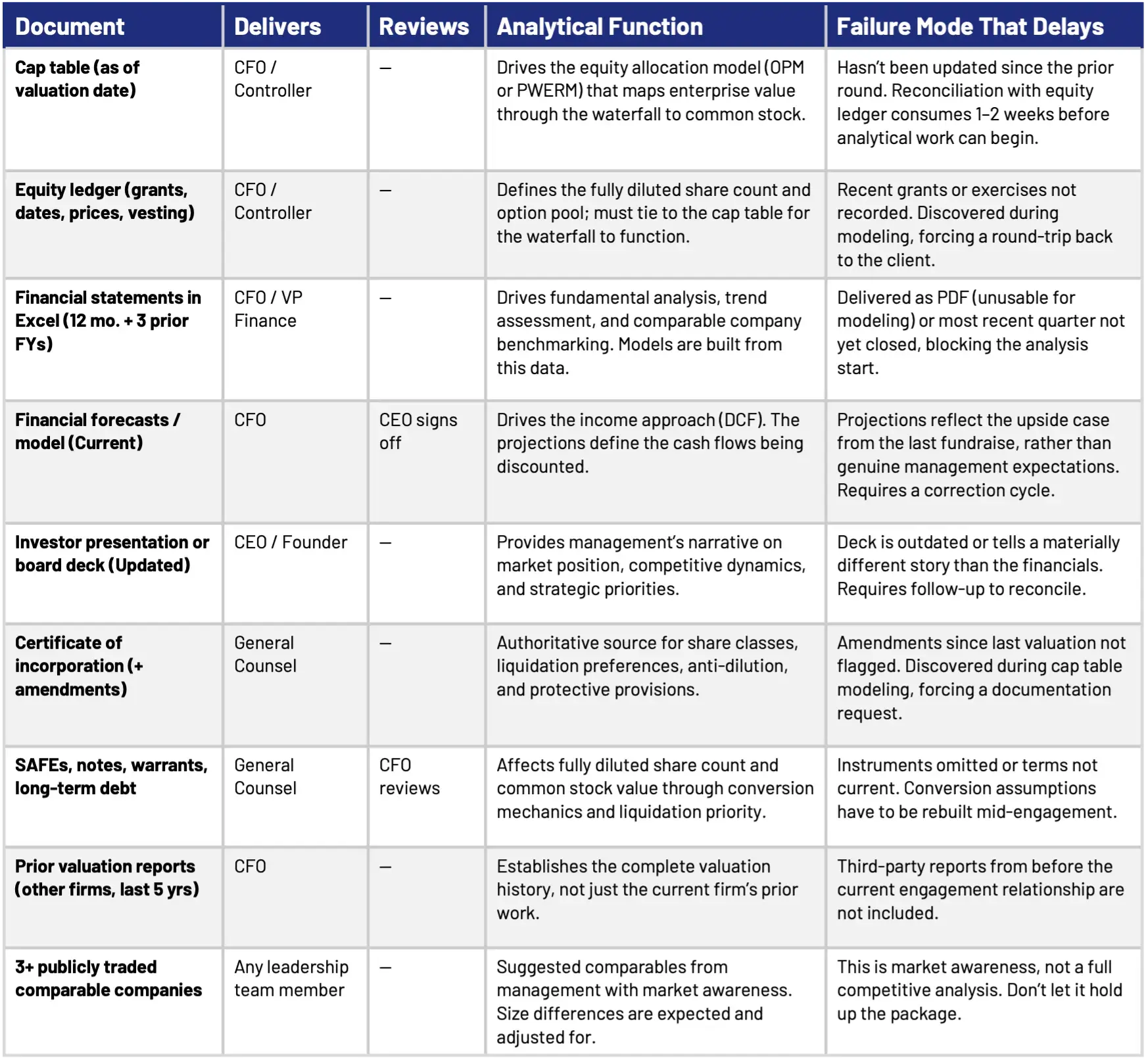

The document package is straightforward to assemble once you know what’s needed and why. A CFO or controller who sets aside a focused afternoon to pull everything together — confirmed, current, and reconciled — can kick off the engagement with a complete upload on day one.

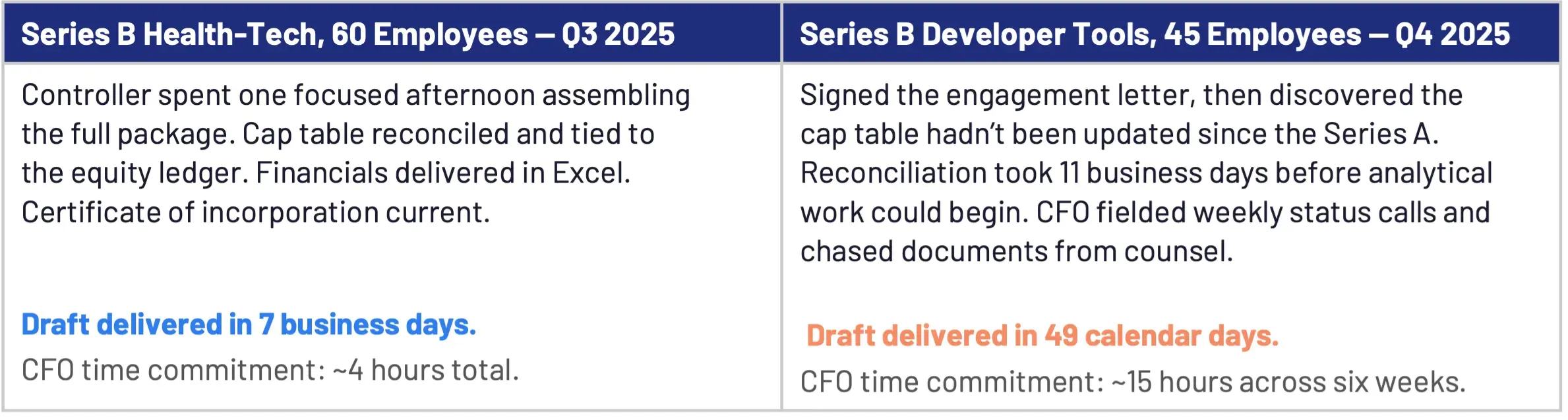

How much difference does document readiness make? Here are two real engagement case studies:

With the same valuation methodology, same team, and the same flat-rate fee the only difference was whether the checklist above was complete on day one. Company A’s board approved the new strike price on schedule. Company B’s board had to postpone option grants by a full quarter.

The person quarterbacking the engagement — usually the CFO or controller — needs to align three dates: when the documents will be ready, when the board will meet to approve the new strike price, and when the next option grants are planned.

The cleanest approach is to work backward from the grant date. If the company is planning to issue options at the next board meeting, the final valuation report needs to be delivered before that meeting — with enough lead time for the board to review. The question we hear most often at this stage: once you have everything you need, how long does the valuation take?

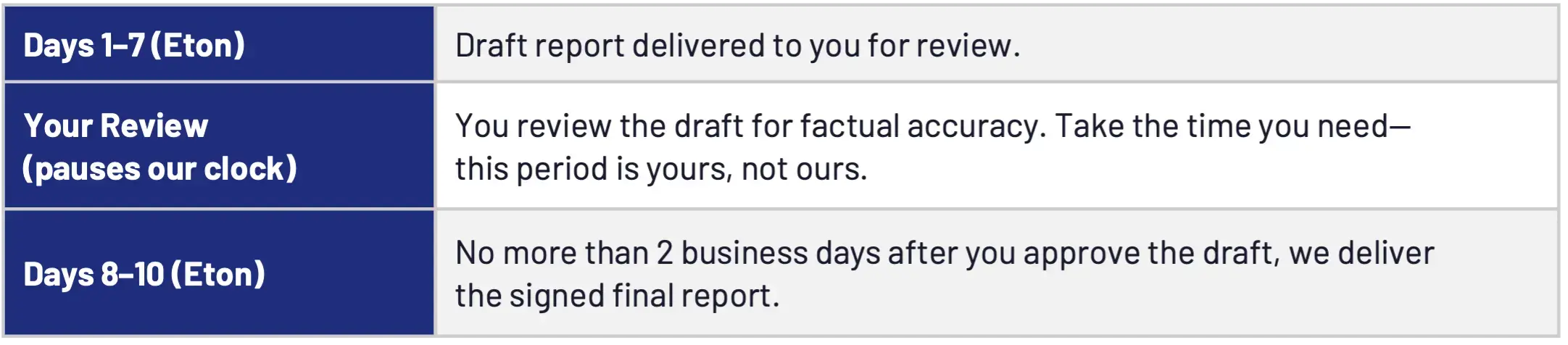

Here’s how the calendar works at Eton, once we’ve confirmed that we have everything we need:

That’s 10 business days of our work from confirmed materials to a signed report—at our longest standard turnaround, which is also our lowest price tier. Faster turnarounds are available. The fee is a flat rate, all-in—no hourly billing, no revision surcharges, no surprises.

The companies that move through renewals most smoothly share a common trait: they don’t treat their 409A as a compliance requirement to be refreshed on a schedule. They monitor for material events between formal valuation dates and stay in communication with their valuation firm when circumstances change — not at month eleven, but when something significant happens.