Hi, I’m Chris Walton, author of this guide and CEO of Eton Venture Services.

I’ve spent much of my career working as a corporate transactional lawyer at Gunderson Dettmer, becoming an expert in tax law & venture financing. Since starting Eton, I’ve completed thousands of business valuations for companies of all sizes.

Read my full bio here.

For early-stage startups, a 409A valuation can feel like just another compliance step, but it’s one that sets the foundation for every stock option you grant.

At this stage, you need a valuation that’s accurate, defensible, and delivered quickly. And preferably, without the high costs that often come with large 409A firms like Morgan Stanley.

As a leading 409A provider, Eton Venture Services combines Big 4-level technical rigor with the speed, accessibility, and personal guidance early founders need.

Our reports are human-prepared, not automated, and are built to withstand auditor and investor scrutiny, delivering full IRS safe harbor protection while remaining cost-effective for growing teams.

In this article, I’ll break down how early-stage 409As differ from late-stage ones, the process we follow at Eton, and highlight why growing companies choose us as their valuation partner.

The purpose of a 409A valuation is always the same: to determine the fair market value of a company’s common stock and maintain IRS safe harbor. What changes between early- and late-stage startups is how that value is determined.

For early-stage companies, valuations rely on simpler inputs and methods. With limited financial history and a straightforward cap table, usually common stock, SAFEs, or a single preferred round, the analysis often draws on recent funding terms, comparable private transactions, or an asset-based approach to estimate value.

These reports still need to meet IRS requirements and must hold up to review, but they don’t need the complex scenario modeling that later-stage companies require.

By the time a company reaches Series B or beyond, valuations involve more layers of data and modeling. Multiple preferred rounds, liquidation preferences, and secondary transactions make equity allocation more complex, so more advanced methods are necessary to capture how value flows across share classes.

These later-stage valuations also face deeper external scrutiny from auditors and investors, which means documentation and assumptions must be detailed enough to withstand that level of review.

In essence, early-stage 409As are simpler in structure and analysis, while late-stage 409As involve greater modeling depth, documentation, and review.

The table below shows how they compare across key areas:

Aspect | Early-Stage (Seed / Series A) | Late-Stage (Series B, C, D, Pre-IPO) |

Equity structure | Simple cap tables (founders’ common stock, SAFEs, one preferred round). | Multiple preferred rounds, layered terms, secondary transactions. |

Financial history | Limited or no revenue history, forecasts often uncertain. | Established revenue, track record, reliable forecasts. |

Methodologies | Market comparables, asset/cost approaches. | Backsolve, DCF, PWERM (scenario modeling). |

Scrutiny level | Primarily reviewed for IRS safe harbor, with minimal outside involvement. | Must satisfy IRS safe harbor while also withstanding review from auditors, investors, and in some cases the SEC. |

Frequency | Typically refreshed after funding rounds, or annually if options are being granted. | Refreshed every 6-12 months, often more frequently due to financings, secondaries, or audit requirements. |

Valuation partner needs | Provider focused on straightforward compliance for simple structures. | Provider with the expertise to handle complex equity and meet auditor-level standards. |

At the early stage, your 409A valuation might seem like a simple compliance step, but if it’s done poorly, it can create bigger problems later, from overpriced options to IRS exposure when you least expect it.

At Eton, we built our early-stage 409A service to keep that step straightforward and problem-free, so you can stay focused on building.

You get fast, defensible valuations, real human guidance, and safe harbor–compliant reports, without Big 4 pricing or automated shortcuts.

Here’s what early-stage teams value most about working with us:

Early-stage founders can’t afford to wait weeks for a valuation when they’re trying to close a round, issue option grants, or prepare for board approval.

That’s why we offer a 1-day turnaround option. And while we’re able to meet tight timelines, this speed never comes at the expense of technical accuracy, documentation, and compliance expected by auditors and investors, so you can move forward with confidence knowing your valuation meets every required standard.

Big 4 firms often charge $8,000 or more for a single 409A valuation, even when a company’s structure is straightforward.

For early-stage founders, these costs don’t make sense. You need a valuation you can trust without burning through your runway.

Eton delivers the same level of technical rigor and documentation expected from the Big 4, at a fraction of the price. Our appraisers come from Big 4 consulting and Stanford Law backgrounds, bringing the same analytical standards and audit-ready detail those firms are known for.

But because we operate as a boutique firm, we’re able to deliver that expertise efficiently, without the overhead or multi-layered review cycles that drive up cost at larger firms.

For early-stage startups, that means access to senior-level valuation talent and defensible, audit-compliant reports, all priced to fit the realities of a growing business.

Related Read: How Much Does a 409A Valuation Cost? 409A Prices in 2025

Many early-stage founders don’t realize that unsigned reports don’t qualify as independent appraisals under Section 409A. Those reports can be challenged by the IRS, putting both the company and employees at risk.

Every Eton valuation is signed by a qualified appraiser, ensuring it meets the IRS definition of an independent appraisal and carries safe harbor protection.

That signature is your legal and financial safeguard, protecting your team from unexpected tax exposure and preventing costly rework down the line.

Even though early-stage valuations don’t face the same level of outside scrutiny as late-stage ones, they still need to be grounded in solid analysis and credible reasoning.

Under Section 409A, the IRS only challenges a valuation if it’s deemed “grossly unreasonable,” but meeting that threshold still requires sound assumptions and clear documentation.

A rushed or automated 409A valuation report often misses that standard, creating problems down the road, like confusion during board approvals, inflated option pricing, or the need to redo valuations once investors start asking for more documentation.

Eton’s valuations are built to meet that level of defensibility from day one. Each report is prepared by experienced appraisers, not algorithms, with every assumption, comparable, and methodology fully documented and validated to ensure your valuation holds up under review.

Our team applies the same analytical rigor used in later-stage and audit-level valuations, giving early-stage founders reports that remain accurate and reliable as the company scales and external scrutiny increases.

With Eton, you’ll always work directly with experienced appraisers, not algorithms or layers of junior staff.

We believe every valuation deserves expert judgment and personal attention, especially for founders navigating 409A for the first time.

You’ll have one point of contact throughout the process, access to calls to discuss your report in detail, and the assurance that the person reviewing your data is the same one signing your appraisal.

This hands-on approach means no surprises later and no confusion about how your valuation was determined.

For founders who need to move fast, getting a defensible 409A valuation shouldn’t slow you down. Whether you’re issuing options to your early hires or completing your first funding round, Eton’s early-stage process is built for speed without sacrificing compliance, with most valuations delivered within maximum 10 days, and a 1-day turnaround available when needed.

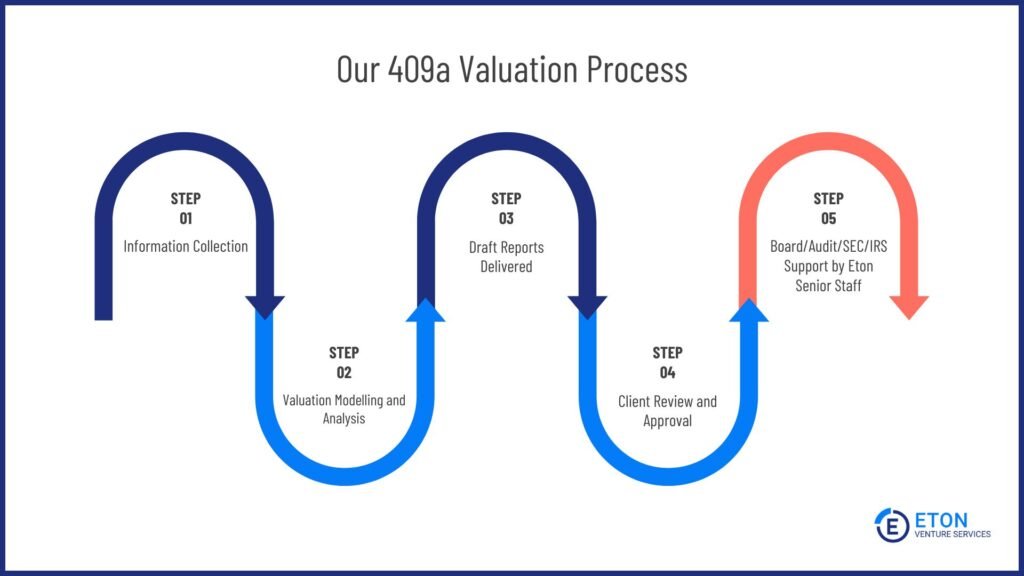

Below is what our 409A valuation process looks like from start to finish, assuming our standard delivery time of 10 days:

Timeframe: 1-2 days

We begin by gathering the key documents that form the basis of your valuation. Our team reviews everything as soon as it’s received, flagging any missing or unclear details upfront to avoid delays or complications later.

Documents typically include:

Even if your financial history is limited, as it often is at the seed or Series A stage, that’s perfectly fine. We use whatever reliable data is available to ensure your valuation remains fully supportable under Section 409A.

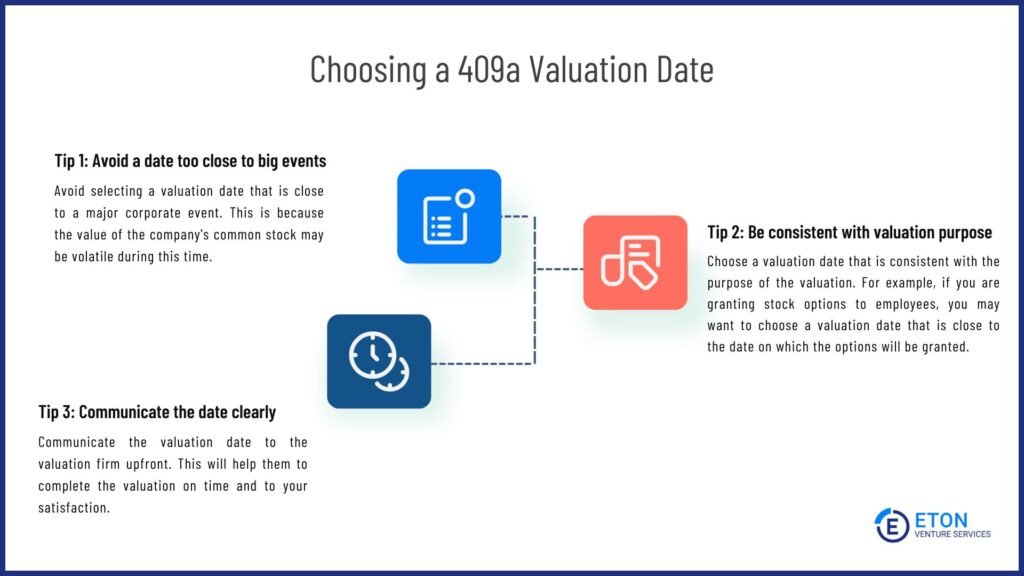

Timeframe: 1 day

Once your documents are in, we’ll help you select the right valuation date. This date determines the fair market value (FMV) of your company’s common stock as of that point in time, and your IRS safe harbor protection is tied directly to it.

If the date doesn’t align with your company’s actual activity or upcoming events, you could end up with a valuation that becomes outdated quickly, forcing you to redo it sooner than expected.

Our team helps you choose a date that keeps your valuation accurate and valid for as long as possible. We typically recommend:

These steps ensure your valuation date supports IRS compliance, reduces unnecessary rework, and keeps your option grants and reporting aligned with your company’s real financial position.

Timeframe: Anywhere from 1-7 days (depending on specified turnaround time)

Once the date is set, we move straight into valuation. For early-stage startups, our analysis draws on methods suited to limited financial history, such as the Berkus Method, the Scorecard Method, and more, depending on your structure. We’ll cover these methods later in the article.

Each report is prepared manually by senior appraisers, not algorithms, to ensure every assumption, comparable, and data source is properly reviewed and documented.

For founders on tight timelines, this entire stage can be completed within one business day through our expedited delivery option.

You might also like: 10 Startup Valuation Methods for Founders

Delivered on: Day 7 or earlier (depending on specified turnaround time)

You’ll receive a detailed draft report showing exactly how the valuation was determined, including the methods, assumptions, and resulting fair market value of your common stock.

This gives you a clear view of the analysis before finalization and time to confirm that everything aligns with your financials and board requirements.

Delivered on: Day 10 or earlier (depending on turnaround option)

Once the draft is approved, we issue the final signed report.

This signed report ensures your company’s common stock is valued accurately and defensibly, protecting your team from compliance risks and giving you the confidence to issue equity immediately.

Let’s take a look at the different valuation methods we use to complete your valuation:

The Berkus Method estimates a startup’s value before it generates revenue, focusing on progress in key qualitative areas rather than financial projections.

Created by U.S. angel investor Dave Berkus, the model assigns value to five success factors that reduce startup risk:

This method is best for pre-seed and seed stage startups that lack reliable forecasts or historical financials. It’s often used as an initial framework before applying more quantitative methods like the Venture Capital Method, which we also cover below.

Here’s how it works:

Because it focuses on concrete, verifiable numbers, this method is often used for pre-seed and seed-stage startups, especially those with significant investment in technology or intellectual property.

At this stage, there’s little financial history and limited visibility into future earnings, so the most defensible way to estimate value is by looking at what’s already been built and paid for, rather than what might be achieved later.

Here’s how it works, step-by-step:

For founders, this approach sets a defensible, objective baseline, especially when market comparables or forecasts aren’t yet credible. It gives investors a tangible sense of “what’s been built” and ensures valuations stay grounded in verifiable investment, not speculation.

That said, the Cost-to-Duplicate approach only tells part of the story. It doesn’t capture future growth potential, brand value, or network effects, which often drive a startup’s true upside.

That’s why valuation experts typically use it as a starting point, complementing it with market or income-based methods (like the Venture Capital or Scorecard approaches) to capture the full picture of a company’s worth.

The Scorecard Method values an early-stage startup by benchmarking it against recently funded peers in the same stage, sector, and region, then adjusting that benchmark up or down based on how the company stacks up across a set of weighted factors.

This method is best suited for pre-revenue or early-revenue startups, typically in the pre-seed to Series A range, where financial data is limited and valuations rely more on qualitative progress than cash flow.

It’s widely used by angel investors because it balances structure with flexibility, offering a realistic way to compare young companies that may not yet have revenue but show clear signs of potential.

Here’s how it works:

While structured, this method still carries an element of subjectivity, especially in weighting and scoring. That’s why we apply professional judgment in evaluating each factor, document our reasoning for every score, and cross-check results against comparable transactions and market norms to ensure every assessment remains objective, well-reasoned, and defensible.

The Risk Factor Summation Method starts with the average pre-money valuation of comparable startups in the same industry and region, then adjusts that baseline up or down after evaluating 12 key risk factors.

It’s typically used for seed to Series A startups, where the business has begun taking shape but still faces uncertainties that can materially affect valuation.

In many ways, this method complements the Scorecard Method. While the Scorecard evaluates how a company creates value compared to peers, the Risk Factor Summation Method assesses how risk might reduce or enhance that value.

Both start with a market benchmark, but they approach it from opposite directions: one measures strengths, the other measures exposure.

Here’s how it works:

Although it’s straightforward to apply, the Risk Factor Summation Method assumes each category has the same potential impact on value, since every risk factor can adjust the baseline by the same fixed dollar amount.

Unlike the Scorecard Method, it doesn’t assign different weights to factors like management or technology. This means it can overlook how some areas influence value far more than others.

It also tends to highlight what could go wrong more than what could go right, giving it a slightly “glass-half-empty” perspective.

For that reason, we often use it alongside other methods to build a more balanced view of a startup’s valuation.

The Venture Capital Method estimates a startup’s value by working backward from its future exit potential. Instead of asking, “What is the company worth today?” it asks, “What could it be worth at exit and what return would justify investing now?”

This method is best suited for Series A startups with early revenue traction and a credible path to significant growth or exit. It’s widely used by venture capital investors because it ties valuation directly to expected returns and ownership outcomes.

Here’s how to apply it:

This process connects future expectations with present ownership. In the example above, a $3 million investment in a $9.6 million post-money company would represent roughly 31% equity.

While widely used in early-stage funding, keep in mind that the VC method comes with inherent limitations. It relies heavily on assumptions about future growth, market conditions, and exit timing, all of which are uncertain.

Forecasting several years ahead is speculative, and exit multiples can fluctuate with shifts in investor sentiment or economic trends.

The expected return multiple also depends on each investor’s perceived risk and target outcomes, meaning two parties can reach very different valuations for the same company.

Ultimately, this method reflects investor expectations rather than an exact measure of fair value, making it most useful for setting benchmarks and negotiating ownership stakes rather than determining intrinsic worth.

At the early stage, every dollar and every week matters. You’re building products, raising capital, and issuing your first options, all while trying to keep momentum.

That’s why we built Eton’s early-stage 409A service: to give founders fast, defensible valuations that don’t slow you down or drain your budget.

With Big 4-level technical rigor, Stanford Law-trained appraisers, and turnaround options as quick as one day, we help you issue options fast, satisfy your board, and move forward knowing your valuation will stand up under audit or investor review.

Since 2010, we’ve delivered more than 10,000 valuations across every stage of growth, and for early teams, that experience means you’re getting the same precision and protection trusted by venture-backed companies nationwide, at a fraction of the cost.

If you’re preparing to issue your first options or need a new 409A after a funding round, Eton can get you there quickly and keep you fully protected under IRS safe harbor.

Contact us to get started.

The IRS safe harbor rule requires an updated 409A valuation at least once every 12 months, or sooner if a material event occurs that could change your company’s value.

Common material events include:

For early-stage startups, it’s best to refresh your valuation right after a financing round or before issuing new option grants. This ensures your common stock is priced correctly and your team’s equity remains compliant under safe harbor.

At Eton, we help founders plan ahead so they can time valuations efficiently, avoiding rushed reports or unnecessary re-dos while staying fully protected. Contact us here to learn more.

If your valuation isn’t prepared by a qualified appraiser or doesn’t follow reasonable methodology, it can lose IRS safe harbor protection, exposing both your company and employees to serious tax penalties.

That can include:

For early-stage startups, the impact can be severe, especially when trying to retain talent or close a round.

Every Eton valuation is signed by a qualified appraiser and built to meet safe harbor standards, giving founders peace of mind that their reports can stand up under IRS or auditor review.

Because early-stage startups often lack long financial histories or predictable cash flow, appraisers use methods suited to limited data and higher uncertainty. These include:

At Eton, we select the most appropriate method, or combination, depending on your stage, structure, and available data, ensuring every valuation is well-supported and defensible.

Our standard turnaround is within 10 days, but for founders on tight timelines, we offer a 1-day turnaround option without compromising accuracy or compliance.

Every report is prepared by senior appraisers (not algorithms or junior staff) and reviewed to the same standards used for audit-level valuations.

Whether you’re issuing your first options or wrapping up a funding round, we’ll help you meet your deadlines without sacrificing defensibility.

Large firms often charge $8,000 or more for a single 409A, even for simple cap tables. However, other companies often charge between $2,500-$4000.

At Eton, our valuations remain affordable for early-stage startups, ensuring it fits your stage while maintaining Big 4-level rigor.

You get a signed, safe harbor–compliant report without hidden fees or upsells. That’s because we believe accurate, defensible valuations should be accessible, not a drain on your runway.

If you need an exact quote tailored to your business, feel free to contact us here.

Yes. As your company matures, your valuation needs evolve, from simple common stock analysis to complex scenario modeling and audit-level reviews.

Eton supports you through every stage of growth, delivering:

And more.

When you partner with Eton early, you build continuity. The same trusted team handles your valuations from seed through pre-IPO.

Schedule a free consultation meeting to discuss your valuation needs.

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, internal / external counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.