Hi, I’m Chris Walton, author of this guide and CEO of Eton Venture Services.

I’ve spent much of my career working as a corporate transactional lawyer at Gunderson Dettmer, becoming an expert in tax law & venture financing. Since starting Eton, I’ve completed thousands of business valuations for companies of all sizes.

Read my full bio here.

Determining what a portfolio is worth isn’t always straightforward, especially when assets vary in liquidity, complexity, and market visibility.

Still, having a clear, well-supported view of your portfolio is fundamental to financial transparency and governance. It helps you report accurately, approach audits with confidence, and make informed investment decisions when timing matters.

This article covers the key principles of portfolio valuation and explains how to calculate portfolio value under ASC 820 (U.S. GAAP), with practical examples and the steps we use to reach defensible conclusions.

Key Takeaways

Portfolio valuation is the process of determining the value of a portfolio, a collection of assets held by an individual, company, or financial institution at a specific point in time.

While the concept can apply to many types of asset groupings, it is most commonly used in financial reporting, investment management, and regulatory contexts to describe the valuation of an investment portfolio.

This is because investment portfolios consist primarily of financial instruments and investment assets whose values fluctuate with market conditions and are often required or permitted to be measured using fair value, essentially the price a willing buyer and seller would agree on in an orderly market transaction.

In these situations, fair value measurement is governed by frameworks such as ASC 820, which explain how fair value should be determined. We’ll build on that as we go through the valuation process later in the article.

An investment portfolio typically includes a mix of:

We assess the value of each of these assets individually using appropriate methods and inputs, then combine the results to determine the portfolio’s overall value.

Portfolio valuation is a core consideration for all investors. A good way to think about it is to ask whether you need a clear, current view of what your portfolio is worth right now.

You’ll likely need a portfolio valuation if you’re:

If any of these situations apply, an up-to-date portfolio valuation provides the foundation for informed decisions and accurate reporting.

Before getting into how to calculate portfolio value, it helps to understand how ASC 820 fits into the portfolio valuation process.

ASC 820, the Fair Value Measurement standard under U.S. GAAP, establishes a consistent framework for how fair value is measured and disclosed when assets or liabilities are reported at fair value.

This framework is especially relevant for portfolio valuations because many portfolios include assets whose values depend on different inputs and valuation approaches depending on asset type, market activity, and available data.

ASC 820 provides a common reference point for how those values should be determined and supported and ensures that portfolio valuation is:

A key concept under ASC 820 is the fair value hierarchy, which ranks valuation inputs by their reliability:

ASC 820 emphasizes using observable inputs whenever possible. For illiquid or hard-to-price assets, the standard also provides guidance on how to apply judgment and assumptions when observable market data is limited or unavailable.

Related Read: ASC 820: The Complete Guide to Fair Value Measurement

Valuing portfolios under ASC 820 follows a clear and practical process for arriving at accurate, supportable fair value measurements. While portfolio valuations can vary in complexity, the process generally comes down to three key steps:

The first step in any portfolio valuation is identifying the valuation inputs for each asset or liability in the portfolio. As discussed earlier, these inputs fall into different levels based on how observable the underlying market data is.

Some assets can be valued using direct market prices, while others require estimates based on observable market data or, in more complex cases, internally developed assumptions.

Understanding which inputs are available for each asset is critical, as this directly affects both the valuation method used and the reliability of the resulting portfolio value.

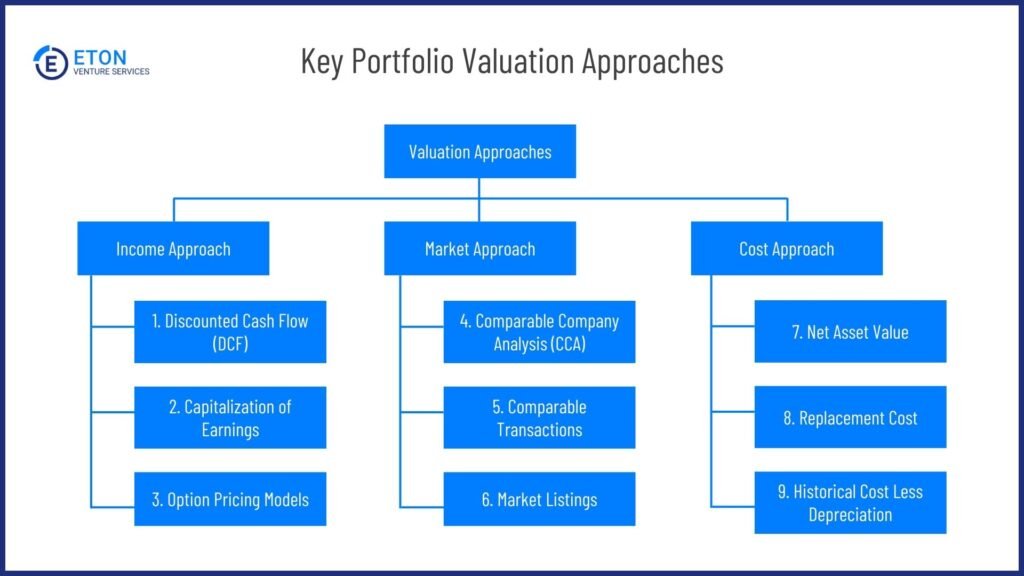

Once valuation inputs are identified, the next step is selecting the appropriate valuation method. We typically rely on three core approaches, with the choice depending on asset type, data availability, and the nature of the investment.

The Income Approach looks forward, grounding valuation in the cash an investment is expected to generate over time. It is most informative when future performance can be reasonably estimated and tied to economic fundamentals.

Let’s say a portfolio holds minority equity interests in two private companies, one generating $1.2 million in annual cash flow and another generating $800,000.

Applying the income approach, we would discount each investment’s projected cash flows to reflect risk and timing, producing a fair value for each position. Those individual values are then combined to determine the portfolio’s overall value.

Common techniques under the income approach include:

The Market Approach looks at current market evidence to estimate value. It works best when there is meaningful market activity that can be used as a benchmark.

For example, an investment portfolio holding minority stakes in three technology companies may estimate fair value by looking at how similar public companies are priced in the market.

If comparable companies trade at, say, 5x revenue, that multiple is applied to each company’s own revenue to estimate value.

If those calculations result in individual investment values of $12 million, $18 million, and $25 million, those amounts are then combined to determine a total portfolio value of $55 million.

Common techniques under the market approach include:

The Cost Approach looks at what an investment is worth based on the value of the assets it owns, net of any liabilities. It’s most relevant when asset values are more observable or meaningful than projected earnings or market comparisons.

For each investment, the fair value of underlying assets is estimated and outstanding liabilities are deducted. If one investment has assets valued at $40 million and liabilities of $15 million, its net asset value would be $25 million. Net asset values across all investments are then combined to determine the portfolio’s total value.

Common techniques under the cost approach include:

After estimating the preliminary value of each investment using the appropriate valuation approach, the final step is to consider whether that value needs to be adjusted based on how the investment is held.

Many portfolios include minority interests or illiquid positions, particularly in private companies. In these cases, we often apply adjustments to reflect two key factors:

These adjustments are applied at the individual investment level, after the initial value is estimated. The adjusted investment values are then aggregated to arrive at the portfolio’s total value.

Not every portfolio requires these adjustments, but they are especially relevant for portfolios with private, illiquid, or minority holdings.

Choosing the right portfolio valuation service provider can make a meaningful difference in the quality of the analysis and how confidently you can rely on the results.

Here are four factors worth paying close attention to:

Portfolio valuation requires more than general finance knowledge. Look closely at who will actually be performing the work: the analysts’ backgrounds, how long they’ve worked on portfolio valuations, and whether they regularly deal with the types of assets in your portfolio.

Experienced specialists are better equipped to handle judgment-heavy areas, select appropriate valuation methods, and navigate complex inputs, especially when portfolios include illiquid or hard-to-price investments. This depth of experience directly impacts the accuracy and defensibility of the valuation.

Past work is often the best indicator of future reliability. A strong provider should be able to point to completed portfolio valuations across different scenarios, asset types, and reporting needs.

Client testimonials, case studies, and repeat engagements signal that the provider consistently delivers work that holds up under scrutiny, whether from auditors, investors, or regulators.

A proven track record also reflects how well a firm communicates findings and supports clients beyond the final report.

Timing matters in portfolio valuation, particularly when valuations feed into financial reporting, audits, or investment decisions. Delays can create downstream issues or force rushed decisions.

A capable provider should be able to deliver efficiently without compromising quality. As a general benchmark, portfolio valuations should not take longer than ten days under normal circumstances.

In time-sensitive situations, experienced teams can often move much faster while still maintaining rigorous standards.

Pricing should be transparent and aligned with the complexity of your portfolio and the level of analysis required. While lower cost can be appealing, it’s important to understand what’s included and whether corners are being cut.

Reliable portfolio valuation is an investment in accuracy and credibility. Comparing providers on cost alone can overlook differences in methodology, experience, and the level of support you receive throughout the process.

At Eton, we’ve completed thousands of business valuations, including portfolio valuations, for leading startups, VC firms, and legal teams for 15 years.

We combine the accuracy and professionalism of Big-4 firms with the friendly and personalized approach of a boutique firm.

Our valuation services are fast, thorough, and affordable. We support our clients through the entire process and will be on hand to support them even after the valuation is delivered.

Should things turn contentious, our valuations are designed to stand up to scrutiny. They’re built on expert human judgment and robust methodologies that automated valuation services can’t replicate.

So how does Eton stack up across these four factors we mentioned in the previous section?

| Factor 1: Specialization & Expertise | We specialize in most common types of valuations, from portfolio valuations to Mergers & Acquisitions. |

| Factor 2: Track Record | We’ve completed 10,000+ business valuations in our 15 years as a firm. And we’ve never lost an audit. |

| Factor 3: Time to Completion | Our valuation services take no more than 10 days. If you need it faster, we can expedite the process for an additional fee. |

| Factor 4: Costs | Considering the wealth of experience that our valuators bring, we keep our costs competitive. It’s much lower than Big 4 firms. On the lower end, a portfolio valuation (not 409A) with Eton will cost around $5000. |

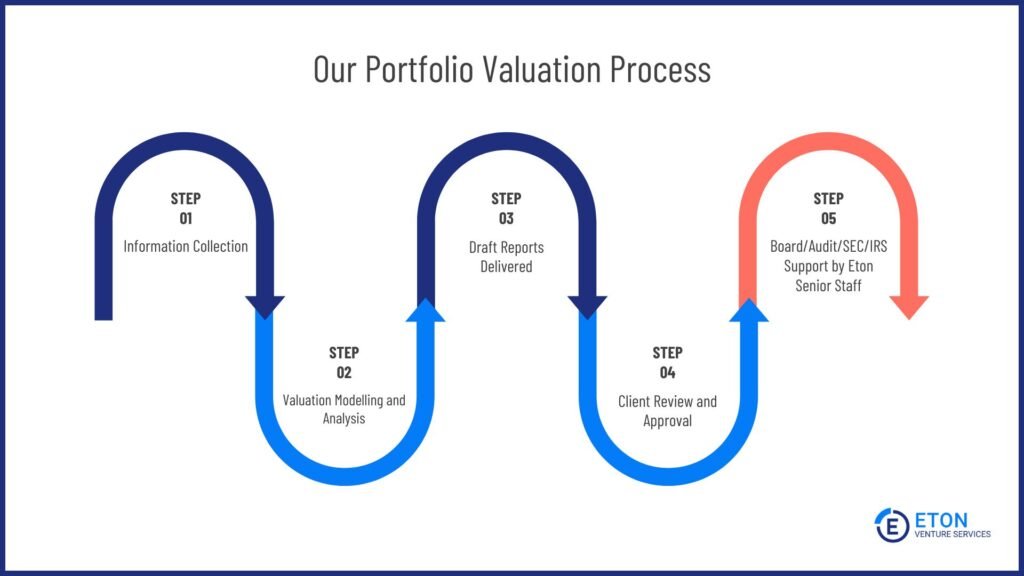

We’ve fine-tuned our portfolio evaluation process to be as smooth and efficient as possible for you. Here’s what working with us typically looks like from start to finish:

Below is a more detailed breakdown of each step in our portfolio valuation process:

Time taken: 1 day

We begin with an initial call to understand your objectives, reporting requirements, timeline, and the nature of your portfolio.

We discuss asset types, valuation complexity, data availability, and any audit or regulatory considerations.

This step ensures the portfolio valuation is scoped correctly from the outset and aligned with how the results will be used.

Time taken: 1-2 days (client side)

To perform an accurate portfolio evaluation, we typically ask you to provide the following documents where available:

Not all documents are required in every engagement. Requirements vary based on portfolio composition and valuation purpose.

Time taken: Anywhere from 1-7 days (depending on specified turnaround time)

Using the information provided, we perform a detailed analysis of each investment in your portfolio.

This involves determining the fair value of each individual asset using the appropriate valuation approaches discussed earlier and aggregating those results to determine the total portfolio value.

Delivered on: Day 7 (by valuation expert)

Your dedicated analyst prepares a draft valuation report that clearly outlines:

We’ll let you know in advance when to expect the draft so you can set aside time to review and ask questions.

Received on: Day 10 (Client to review and raise any concerns and questions)

Time taken to finalize: 1-2 days

You’ll review the draft report to confirm that the assumptions, inputs, and the conclusions about the value of your portfolio align with your understanding. If anything needs clarification, we’re always available to walk through the analysis and address any concerns.

Once feedback is incorporated, we issue the final report and complete the engagement.

If you’re looking for an accurate, fast, and court-defensible portfolio valuation, we’d be happy to help. Reach out today to get started.

Portfolio valuation affects key financial statements:

For investors and other stakeholders, inaccurate or outdated portfolio valuations can distort performance metrics, obscure risk exposure, and lead to misinformed investment or capital allocation decisions. They can also increase the likelihood of compliance issues or regulatory scrutiny.

The frequency of portfolio valuation for financial reporting purposes depends on the company’s reporting requirements and the nature of the assets held.

Publicly traded companies typically perform valuations at least quarterly, while private companies may do so annually or as required by their stakeholders.

It is also important to update valuations whenever significant changes occur in the company’s assets or market conditions that could materially impact asset values.

Engaging a third-party valuation firm, like Eton, for portfolio valuation offers several benefits, including:

Additionally, third-party valuation reports can enhance the credibility of financial statements, and help mitigate potential risks associated with regulatory compliance and stakeholder concerns.

To discuss your portfolio valuation needs, reach out to our team at Eton today for expert support.

Schedule a free consultation meeting to discuss your valuation needs.

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, internal / external counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.