Written by Chris Walton, JD

Written by Chris Walton, JDWhen we value a business, the numbers alone only tell part of the story.

I’ve valued hundreds of companies and seen businesses with similar revenue and profit margins sell for wildly different prices. Why? Because part of their value comes from something intangible: assets like brand reputation, customer relationships, patents, and trademarks. These aren’t physical, but a smart valuation expert will argue they hold significant value.

In this article, we’ll explore what intangible assets are, the different types, how they’re accounted for, and how they’re valued, so you can understand their true impact.

Key Takeaways

|

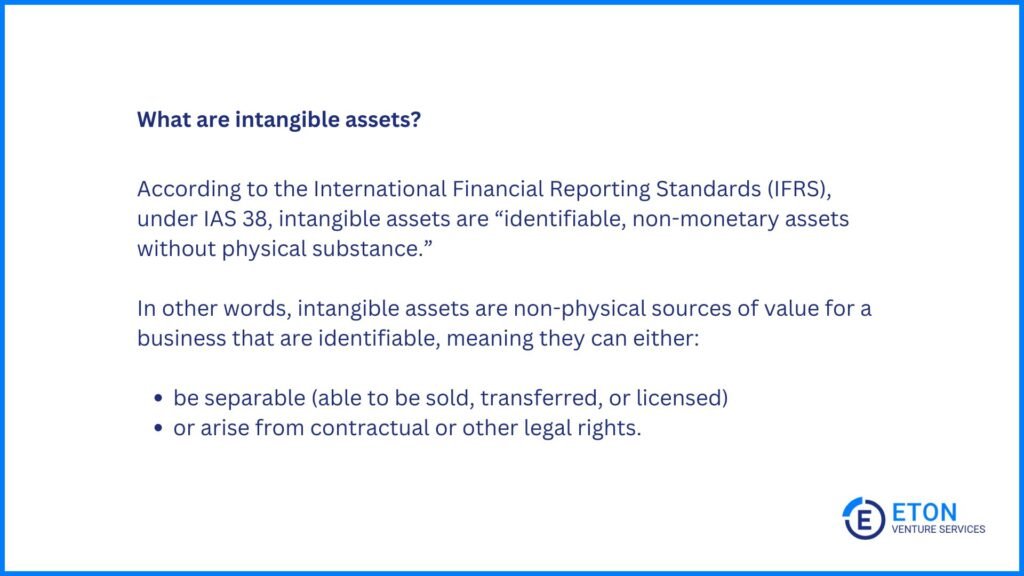

According to the International Financial Reporting Standards (IFRS), under IAS 38, intangible assets are “identifiable, non-monetary assets without physical substance.”

In other words, intangible assets are non-physical sources of value for a business that are identifiable, meaning they can either:

Despite being unseen, they often sit at the heart of a company’s operations, driving revenue, building customer loyalty, and protecting innovation. That’s why they matter as much as physical assets, if not more, in determining a business’s value.

Here are 11 examples of some of the most common intangible assets and how they add value to a business:

Note that while goodwill isn’t identifiable or separable, it is still classified as an intangible asset because it has no physical form. This is what places it in the broader intangible category rather than the tangible category.

However, because it isn’t identifiable, its accounting treatment is different from other intangibles like trademarks or patents.

Since goodwill can’t be separated or directly linked to a specific legal right, it isn’t recognized under IAS 38, meaning it isn’t recorded as a standalone asset on the balance sheet.

Instead, when goodwill is acquired through a business combination (industry lingo for one company acquiring or merging with another), it is recognized under IFRS 3 and recorded as part of the purchase price allocation to the acquiring company.

This distinction reflects goodwill’s role as the excess value paid beyond identifiable net assets (when purchased), rather than a directly measurable asset (when internally generated).

Accountants categorize intangible assets by origin, lifespan, and identifiability because these factors impact how they appear on financial statements, directly influencing a company’s reported value.

This classification helps stakeholders by showing how much of a company’s value is tied to intangible assets, how long those assets will contribute to earnings, and whether they can be sold or transferred. This, in turn, affects financial analysis, investment decisions, and risk assessment.

Here are the three types of intangible assets you’ll come across when evaluating a business or analyzing financial statements:

Purchased:

Purchased intangible assets are those that companies acquire from external sources. For example, companies may acquire patents during an acquisition, purchase trademarks from another company, or buy customer lists as part of a business deal.

For business valuation purposes, these assets have a clearly defined purchase cost, which makes them easier to evaluate and document.

Internally generated:

In contrast, internally generated intangible assets originate within the company.

For example, a brand’s value a company builds through marketing campaigns or software they develop in-house falls into this category.

Finite-life:

Finite-life intangible assets are those that provide economic benefits over a limited period.

Examples include copyrights, which expire after a certain number of years, or licensing agreements with fixed terms.

These assets are consumed over their useful life and typically require systematic allocation of their value over time.

Indefinite-life:

On the other hand, indefinite-life intangible assets, such as goodwill or renewable trademarks, have no foreseeable expiration.

These assets remain in use for as long as the company continues to derive value from them and maintains the necessary renewals.

Identifiable:

Identifiable intangible assets are those that businesses can separate and sell, transfer, license, rent or exchange. They can also arise from legal rights, such as contracts or agreements.

For example, a company’s ownership of a patent or a licensing agreement for a specific technology qualifies as an identifiable intangible asset.

Non-identifiable:

On the other hand, non-identifiable intangible assets—a prime example of which being goodwill—are tied to the overall value of a business and can’t be separated or sold on their own.

This may seem like a contradiction since intangible assets are meant to be “identifiable” as previously mentioned, but goodwill is still classified as one because it’s non-physical and, thus, not a tangible asset.

However, since it doesn’t fully meet the standard intangible asset criteria either, accounting standards treat it as a special category with its own rules, which we’ll cover in the next section.

The way companies account for intangible assets shapes how their financial health is understood. So, beyond compliance, getting their accounting treatment right ensures you’re presenting an accurate and trustworthy financial picture of the business to shareholders and board members.

In this section, we’ll explore two aspects of accounting for intangible assets that’ll help you understand their impact on financial statements and ensure you record them correctly:

Intangible assets appear as “non-current” assets on the balance sheet. That means they’re assets expected to provide economic benefits over a period longer than one year.

However, they’re only recognized on the balance sheet if they meet three key criteria:

Purchased intangible assets, like patents or trademarks acquired from another company, typically meet all three conditions:

This makes them straightforward to record on the balance sheet.

In contrast, internally generated intangible assets, such as “brand equity” created through advertising or goodwill developed over time, often fail to meet the necessary recognition criteria:

As a result, companies don’t capitalize (i.e., recognize on the balance sheet) internally generated intangible assets.

Instead, they record the costs associated with creating them, such as advertising or research expenses, as expenses on the income statement as they occur.

This means they directly reduce the company’s profit in the period they are incurred, rather than being treated as an investment spread out over time.

Intangible assets lose value over time, just like physical ones. Accounting for this ensures financial statements reflect their true worth as they change.

Managing this decline in value depends on whether the intangible asset has a finite or indefinite useful life:

Amortization is a way of spreading out the cost of an intangible asset over the years it is expected to be useful.

For example, if a company buys a licensing agreement for $100,000 that lasts for 10 years, it would record $10,000 as an expense each year for 10 years.

This expense appears on the income statement, reducing the company’s net income each period, while the corresponding reduction in the asset’s value shows on the balance sheet.

A prime example of this is goodwill. For instance, if a company acquires another business and later experiences a significant decline in its market share or profitability, this could indicate that the goodwill associated with the acquisition has lost value.

To check for impairment, the company compares the asset’s carrying value (its recorded value) to its fair value (the price it could be sold for in the market).

If the carrying value is higher, the company reduces the asset’s value on the balance sheet and records the difference as a loss on the income statement.

There are various methods to value intangible assets, all of which are rooted in the three classic valuation approaches: the market approach, the income approach, and the cost approach.

We cover the approaches below, but we’ve also written a detailed breakdown of the specific methods derived from them.

The market approach values an intangible asset based on market data, such as the sale prices, royalty rates, or licensing fees of similar assets.

It assumes that the value of the asset can be inferred by comparing it to what others have paid for comparable assets in similar circumstances.

This approach is most useful when there is reliable market data available, such as published royalty rates for trademarks, brand names, or domain names.

The income approach focuses on how much financial benefit the intangible asset is expected to generate in the future.

It works by forecasting revenue, savings, or other economic benefits the asset will bring, and then calculating what those benefits are worth today.

Companies often value assets like customer relationships or patents, which directly contribute to a company’s revenue, using this approach.

The cost approach estimates the value of an intangible asset based on what it would cost to recreate or replace it today, using modern technology and methods. It also factors in any loss in value due to obsolescence or inefficiencies.

Businesses often use this approach for assets like software or proprietary systems, where the cost to replicate is more straightforward to calculate than future earnings.

If you need support valuing your intangible assets based on these approaches, Eton can help. We bring over 20 years of experience in providing expert-led, defensible valuations across all asset types, including intangibles. Contact us today to learn more.

Intangible assets are becoming the foundation of modern economic growth, reshaping how businesses compete and innovate.

Over the past 25 years, their share of total investment has grown by 29%, contributing to a 63% rise in gross value added (GVA) across the U.S. and 10 European economies.

This growth highlights a clear shift toward a knowledge-driven economy, where intellectual property, proprietary technology, and human capital are at the center of business success.

Companies that invest more in these assets are seeing the impact: The fastest-growing firms—those in the top quartile for GVA growth—allocate 2.6 times more to intangibles than lower-performing businesses.

So, as the economy evolves, these assets are no longer an afterthought; they’re the drivers of growth, resilience, and lasting value in an increasingly knowledge-based world.

Yes, intangible assets can lose value over time due to factors such as obsolescence, loss of market relevance, or negative brand perception.

Assets like goodwill are subject to impairment testing, while finite-life assets like patents are amortized over time, reflecting their declining value.

Companies protect their intangible assets through legal measures like patents, trademarks, and copyrights, as well as through strategic business practices like maintaining customer relationships and securing trade secrets. Protecting these assets is critical to preserving their value and ensuring long-term success.

Intangible assets, like brand reputation, customer relationships, or intellectual property, play a significant role in a company’s valuation during an acquisition.

For instance, a loyal customer base suggests steady revenue, while patented technology or trademarks can signal a strong competitive edge.

These assets highlight growth potential and market positioning, which can drive up perceived value. Effectively demonstrating their importance can make a big difference in negotiations and the final deal.

Yes, intangible assets can be sold or transferred, but the process often depends on the type of asset and any legal or contractual restrictions.

For example, intellectual property like patents, copyrights, or trademarks can typically be sold or licensed to another party. Customer lists or software can also be transferred, provided confidentiality or ownership agreements allow it.

However, some intangible assets, like goodwill or personal reputation, are tied closely to the business or individual and are not transferable.

Schedule a free consultation meeting to discuss your valuation needs.