Hi, I’m Chris Walton, author of this guide and CEO of Eton Venture Services.

I’ve spent much of my career working as a corporate transactional lawyer at Gunderson Dettmer, becoming an expert in tax law & venture financing. Since starting Eton, I’ve completed thousands of business valuations for companies of all sizes.

You started your company with a vision to build something that lasts, whether that means disrupting an industry, scaling a proven model, or taking your next big step toward IPO.

You’ve been heads down building the product, hiring a strong team, and raising capital from investors who share your vision.

Now, issuing stock options has become an important part of that growth, rewarding the people building alongside you and aligning everyone for what’s ahead.

But it also comes with IRS rules you need to follow, including obtaining an independent 409A valuation report to establish the fair market value of your common stock, known as the 409A price.

In this guide, we’ll break down everything you need to know about 409A valuations: what they are, when you need one, how they’re performed, their cost, how they differ from other types of valuations, and how to ensure your report meets IRS standards.

Whether you’re an early-stage startup or a later-stage company managing multiple rounds, understanding these fundamentals will help you make informed decisions and stay compliant.

What Is a 409A Valuation?

A 409A valuation is an assessment of the fair market value (FMV) of a private company’s common stock, essentially the price a willing buyer and a willing seller would agree on for those shares under normal market conditions.

This value is then used to set the 409A strike price for stock options, which give employees the right to buy common stock in the future.

The IRS requires a 409A valuation to make sure those stock options aren’t issued below fair market value. Setting the strike price below FMV could trigger heavy tax penalties for employees, so a 409A helps keep both the company and its team compliant.

To determine FMV, the valuation considers the company’s financials, market conditions, capital structure, and growth prospects (but cautiously and only if they’re well supported).

Most companies hire a third-party 409A appraiser to perform this analysis using accepted methods such as discounted cash flow, market comparables, or asset approach. We cover these in more detail later in the article.

A 409A valuation remains valid for 12 months or until a material event occurs, such as a new funding round.

How a 409A Valuation Differs From Other Types of Valuations

To put the 409A valuation in context, here’s how it compares to the other types of valuation terms you’ll encounter as your company grows:

Type of Valuation

Purpose

Subject

Methodology

Typical Outcome

No results found for ""

Showing 7 of 7 valuation types

409A Valuation vs Investor Valuation (VC Valuation)

A VC valuation reflects what investors are willing to pay for preferred shares, which include special rights like liquidation preferences and anti-dilution protection.

It’s usually much higher than a 409A valuation, because it’s based on where the company is going, not where it is today. Investors factor in growth potential, not just current numbers.

A 409A valuation, by contrast, only focuses on the fair market value of common stock as it stands today, without future projections or negotiation.

Some of the factors that may lead to differences in the two valuations include:

Growth projections: 409A uses modest, defensible projections based on historical performance; VCs assume much higher growth, often 50-100% year-over-year.

Discount rates: 409A applies higher rates to reflect risk around 30-40% for early stage companies; VCs use lower ones, reflecting higher risk tolerance due to the protective rights of preferred shares.

Comparable companies: 409A relies on truly comparable peers based on industry, business model, financials, and stage; VCs can choose aspirational ones.

Liquidity: 409A assumes the company will stay private for the foreseeable future, applying larger discounts for lack of liquidity; VCs assume a shorter time to exit or IPO.

Negotiation: 409A is objective; VC valuations are negotiable based on deal terms.

While a VC valuation sets investor pricing and guides funding terms, a 409A valuation keeps option pricing aligned with IRS standards, each serving a distinct purpose. However, both play an important role in the startup ecosystem.

A 409A valuation reflects the fair market value of common stock for compliance purposes and assumes the company will remain private in the near term, which means applying discounts for illiquidity since the shares cannot be easily sold.

An IPO price is set when the company goes public and is influenced by investor demand, market conditions, and future growth expectations.

Unlike 409A valuations, it is not limited by tax or compliance requirements and often reflects a much more optimistic view of the company’s potential.

For instance, a private company could have a 409A valuation of $50 per share, only to see those same shares debut at $150 once public.

The gap between the two reflects their purpose. The private company 409A valuation is for compliance and employee option pricing. The IPO price is driven by public market sentiment.

409A Valuation vs Post-Money Valuation

A 409A valuation reflects what your common stock is worth today. A post-money valuation reflects what investors pay for preferred shares after funding, based on expected growth and added rights.

Post-money valuation can be calculated by dividing the investment amount by the percentage of ownership the investor receives. It sets the paper value of the company and is based on the preferred stock price agreed during the deal.

Preferred shares carry protections like liquidation preferences and anti-dilution protection, which don’t apply to common stock. This makes preferred shares more valuable.

So, if a company raises $10 million at a $40 million pre-money valuation, the post-money is $50 million. But the 409A valuation of common stock might fall between $10 and $15 million. This isn’t a mismatch but is instead a result of the different goals behind each valuation.

409A Valuation vs Preferred Price

Preferred price is what investors pay for preferred shares during a funding round.

Preferred shares typically come with added rights and protections. These can include liquidation preferences, anti-dilution clauses, board seats, and priority in payout if the company is acquired. Because of these advantages, preferred stock is more valuable than common stock and commands a higher price.

The preferred price is set through negotiation between the company and its investors. It reflects the perceived upside of the company and is often based on future growth expectations, not just current performance. This price becomes the basis for the company’s post-money valuation, but it does not apply to common shares.

In contrast, a 409A valuation applies discounts to reflect the lack of these rights, lower liquidity, and higher risk associated with common stock. That’s why the common stock price in a 409A valuation is usually significantly lower than the preferred price, even at the same point in time.

409A Valuation vs Strike Price

⚠️ Note: In public markets, a “strike price” is the fixed price at which options can be exercised, to buy (calls) or sell (puts) a stock.

In startups, it refers to the price employees pay to purchase common stock under their equity grants.

A 409A valuation sets the minimum legal strike price by determining fair market value on the grant date.

By law, the strike price must be at or above the FMV on the grant date. Setting it lower without proper documentation can expose employees to IRS penalties.

Most startups complete a 409A valuation to establish a compliant strike price that still leaves room for employee upside. A lower 409A means a lower strike price, which creates greater potential gain for employees when the company’s value increases.

So while the strike price is the number written into an option grant, the 409A valuation is what makes that number valid.

Why Is a 409A Valuation Important?

409A compliance protects you and your employees from major tax consequences when issuing stock options or RSUs.

Proper valuations also:

Minimize alternative minimum tax (AMT) risks.

Help set terms for new equity grants. New grants should be issued at the most recent 409A price to comply with IRS rules.

Give you an unbiased, accurate read of what your business is really worth

Prove to auditors and investors that you’re complying with legal and reporting obligations

Attract investors by providing them with a clear understanding of your company’s value

Maintain employee trust by ensuring they’re protected from IRS penalties

Luckily, there’s a system in place that makes these benefits easy to obtain. It’s called a “safe harbor”.

409A safe harbor is a set of IRS rules that, when met, give your 409A valuation a presumption of reasonableness. In practice, that means the IRS has to prove your 409A value is grossly unreasonable before it can challenge your stock option pricing.

There are three routes to 409A safe harbor status:

Independent Appraisal Presumption: A qualified, independent third-party appraiser determines the company’s value (the most common method).

Illiquid Start-Up Presumption: A valuation performed by a qualified individual (who may be internal or external) with relevant experience, used by early-stage private companies under certain conditions.

Formula Presumption: The company uses a consistent, legally binding formula (often in shareholder agreements) to set share value.

The simplest way to secure a 409A safe harbor for most businesses is the first route: A 409A Independent Appraisal Presumption. It involves hiring a reputable, independent third-party valuation firm who will complete the valuation on your behalf.

These experts ensure your 409A valuation satisfies the IRS criteria to be considered safe harbor-compliant. The following section details those legal requirements.

Legal IRC 409A Valuation Requirements You Must Meet to Avoid Penalties

The valuation must be documented in a written report. A verbal estimate or internal spreadsheet does not satisfy IRS requirements.

2. Update your 409A every 12 Months or after a material event

Valuations expire after 12 months, or sooner if new information arises that materially affects the company’s value, such as a funding round, merger, acquisition, or major business change.

Failing to update your 409A on time can lead to significant IRS penalties, including immediate taxation on deferred compensation and a 20% additional penalty.

3. Use an independent, qualified specialist

While we’ve mentioned earlier that there are other routes to safe harbor (such as the Illiquid Start-Up and Formula Presumptions), these apply only in limited circumstances and are subject to greater IRS scrutiny.

An independent appraisal ensures objectivity, credibility, and compliance with IRS standards, giving your company the strongest presumption of reasonableness if reviewed.

Your valuation provider must apply accepted methods, typically the Market Approach, Income Approach, or Asset Approach, and follow USPAP (Uniform Standards of Professional Appraisal Practice).

Using reasonable, standardized methodologies ensures your valuation is credible and defensible in the event of an IRS review.

5. Consider all relevant information and document the valuation

Your appraiser must account for all factors that could influence value, including financial data, market trends, capitalization structure, and growth prospects.

In addition, a compliant valuation must include thorough documentation of the data, assumptions, and methods used.

What Happens if These 409A Valuation Requirements Aren’t Met?

If any of these requirements are not met, your valuation may fail to qualify for safe harbor protection, which can trigger significant IRS penalties and severe consequences. These can include:

Tax implications for employees: Employees might face immediate tax liabilities on their stock options, including a 20% federal penalty, accrued interest, and potential alternative minimum tax (AMT), a situation most startups want to avoid.

Monetary penalties: The IRS can impose substantial fines on the company depending on the degree of non-compliance, plus additional legal or accounting costs to correct past errors.

Legal and reputation risks: Beyond financial penalties, legal challenges and a damaged reputation can have long-term effects on your startup’s growth and ability to attract talent and investment.

To avoid these risks, you want to work with a 409A valuation provider whose reports consistently qualify for IRS safe harbor.

A safe harbor-compliant valuation is presumed valid unless the IRS can prove it’s “grossly unreasonable”. If it doesn’t qualify, the burden of proof falls on you.

At Eton, every valuation we deliver meets safe harbor standards. We offer two tailored 409A valuation packages designed to match your company’s stage and structure:

Early-Stage Startup 409A Valuation Package: Ideal for seed to Series A companies with straightforward ownership structures. It includes everything needed to issue options quickly and stay compliant without unnecessary complexity.

Late-Stage Startup 409A Valuation Package: Designed for Series B and later companies with multiple investment rounds or more intricate ownership structures. It includes deeper analysis, scenario modeling, and additional rigor for audit or investor review.

What Are the Biggest 409A Valuation Mistakes Startups Make?

We often see companies make these mistakes (and get penalized for it):

Misconception about desiring low stock values for granting options: Many companies mistakenly aim for the lowest possible stock value to grant cheap stock options. This approach can lead to significant compliance issues and potential legal and financial repercussions, as it might contravene the fair market value requirements of Section 409A.

Improper timing and granting of options: Ensuring that stock options are granted at no less than fair market value on the date of the grant is critical. Mishandling this can result in significant non-compliance issues with the IRS. Get your 409A first, and then grant your stock options pursuant to its conclusion.

Non-compliance with the “Safe Harbor” methodology: Adhering to accepted valuation methodologies, like independent appraisals, is essential for compliance. Deviations from these methods can lead to serious consequences.

Lack of documentation: Keeping thorough records is crucial. Inadequate documentation of the valuation approach and data used can be problematic, especially during audits.

Ignoring material events: Failing to reassess the company’s valuation immediately after a significant event can result in outdated and unacceptable valuations by the IRS.

Inappropriate use of historical data: Using outdated financial data can lead to incorrect valuations, making this a significant concern.

Neglecting to reassess valuations regularly: Regular reassessment, at least annually and after material events, is required to ensure ongoing compliance with IRS expectations. We recommend you consult an annual valuation service provider to help you with this.

When and How Often Do You Need a 409A Valuation?

You’re required to complete a startup 409A valuation the first time you plan to grant stock options to employees, then every 12 months as an early-stage company.

Late-stage companies often shift to semi-annual or quarterly schedules to support continuous grants and meet audit requirements.

Both early-stage and late-stage startups are also required to obtain a new 409A valuation after a material event.

A material event is any development that significantly affect your company’s value, such as:

New financing rounds – like your first priced round (Seed or Series A) for early-stage startups, or later rounds such as Series C or D for more mature companies.

Mergers or acquisitions – whether you’re acquiring another business or being acquired.

Secondary share sales – common in later-stage startups when early investors or employees sell their shares.

Major shifts in your business model – such as entering new markets or launching a new revenue stream.

Significant market changes – for example, an economic downturn, major industry event, or pandemic.

Pre-IPO preparation – for late-stage companies gearing up to go public.

If a material event occurs, you’ll need to update your valuation before granting any new stock options. The 12-month cycle resets from that new valuation date.

For example, if you conduct your first 409A valuation in March and later close a Series A in September, you’ll need to complete a new 409A valuation after the raise. Your next one would then be due the following September, assuming no further material events occur before then

How Does a 409A Valuation Work? 409A Valuation Process, Timeline & Methodologies

If you’re wondering how to do a 409A valuation or what the process looks like and how long it takes, we’ve outlined it all below, using our approach and timelines here at Eton as a reference.

Step #1: Initiate the 409A Valuation Process – Choose Your Provider

Time taken: You can choose a provider in as little as 1-2 days.

We recommend looking for these three characteristics:

Look for experience and pedigree: Find out who the analysts are, how many years they’ve worked in valuation, what methodologies and processes they follow, and where they’ve worked before.

Check their turnaround time and cost: Some firms charge Big 4 prices and take months to deliver. Others automate the process to cut costs, but leave you exposed to IRS scrutiny or inaccurate results. Look for a provider with Big 4 experience, boutique-level pricing and efficiency, and a 100% human-led process (like Eton) to ensure high-quality valuations within ten days at an affordable cost.

Prioritize ongoing support and accessibility: Choose a team that treats your valuation as a partnership; one that explains assumptions clearly, answers your questions, and offers real human guidance throughout the process.

The first step in working with a consultant will be documentation collection.

This is often a bottleneck, as it takes your team time to collect and prepare information.

At Eton, we request:

financial statements (if you have them)

financial forecasts (if you have them)

capitalization table

articles of incorporation

bylaws

stock option agreement

the deck you show investors

SAFE notes (if you have them)

convertible debt (if you have it)

straight debt (if you have it)

Upon receipt of these documents, our side of the process starts. The first thing we’ll do is check we have everything we need. If we don’t we’ll get in touch immediately and make additional requests.

But from here on out your input and effort are minimal. Your consultant will begin their valuation methodology and get back to you within a few days.

Step #3: Tailored Consultation – Choosing Your 409a Valuation Date

Time taken: 1 day (client and valuation firm)

It’s part of our process to understand what prompted your 409A valuation and what stage you’re at as a start-up.

These details will inform the methodologies we choose and determine if we need to fast-track the process to meet deadlines.

We’ll ask you at this point to choose a valuation date. The valuation date is the date on which the fair market value of your company’s stock will be determined.

If you’re not sure what date to choose, we’ll make some suggestions to assist with this choice.

There are a few things we’ll take into consideration when choosing the date, such as if you’re approaching or have just passed a major corporate event, you’re close to the end of the fiscal year, and when you want to issue stock options to employees.

Your 409A is valid for a year from the date of valuation or until a ‘material event’. Material events include financing rounds, term sheets for financing rounds and acquisitions.

Step #4: Valuation & Modeling in the 409A Valuation Process

Time taken: Anywhere from 1-7 days (depending on specified turnaround time)

Once we have your valuation date and we’ve received your documents, the 409A analysis begins.

This is where advanced methodologies are used to determine your startup’s valuation.

Three Commonly Used 409A Valuation Methodologies

There are three 409A valuation methodologies we use:

market approach

income approach

asset approach

Each one adheres to the AICPA (American Institute of Certified Public Accountants) published guidance on 409A valuations.

Which one gets applied depends on the developmental stage of your business. For example, a series-a 409A valuation might use a different methodology than a seed-stage valuation.

Generally speaking, early-stage startups that have raised funding but aren’t yet profitable will rely on the market approach. Those who haven’t generated revenue and who haven’t raised funds will likely use an asset approach. In both instances, because of the early stage, the company is unable to reliably forecast financials.

The income approach is often applied to businesses that are bringing in revenue with a positive cash flow. They will be able to forecast financials.

We always look to see if one (or all three) approaches fit your situation and will continue to consider them as options throughout the valuation process.

Step #5: Receive a Completed Draft 409A Valuation Report

Delivered on: day 7 (by valuation expert)

Your dedicated analyst will prepare the draft valuation calculations which include the methods chosen, assumptions made, data pulled, and the draft fair market value conclusion.

We’ll let you know when you can expect to receive this draft. That way you can reserve time in your schedule to review it.

As soon as it’s completed, we’ll send them to you.

Step #6: The Final 409A Valuation Process Stage – The Sign Off

Received on: day 10 (client to review and raise any concerns and questions)

Time taken to finalize: 1-2 days

With your draft report now in your possession, you have the opportunity to review it. Check that you understand the assumptions made and are comfortable with the valuation numbers.

If anything is unclear or you have concerns, you can schedule a call with us and we’ll discuss any issues in detail.

When you’re happy with the valuation, we’ll both sign off on the draft calculation pages.

Then you’ll authorize us to prepare the final report. That final report will be delivered to you within 1-2 days.

The cost of a 409A valuation depends on your company’s size, complexity, and stage, but most 409A appraisals for startups fall within the $2,500-$4,000 range.

At Eton, both our 409A valuation packages, early-stage and late-stage, are priced fairly for the level of detail, audit readiness, and personal guidance they include.

For an exact quote tailored to your company’s needs, contact us directly. We’ll respond quickly and walk you through what to expect.

Interested in a full breakdown of 409A valuation costs?

There are a few common misconceptions about 409A valuations that can lead to compliance issues, unexpected tax exposure, or delays when companies start granting equity.

Here are four myths we see most often and the facts you should rely on instead:

Myth 1: “Only Needed for Large Companies”:

A common myth is that only large or mature companies need 409A valuations. In reality, any company granting stock options needs a 409A valuation to ensure compliance.

Myth 2: “Investor Valuation is Sufficient”

Some believe that the valuation determined in a funding round can be used for 409A purposes.

However, investor valuations reflect what VCs pay for preferred stock, which includes protective rights and preferences that make it more valuable than common stock.

Additionally, investor valuations are forward-looking and based on growth potential, while 409A valuations must determine the current FMV of common stock as it stands today.

Because of these fundamental differences, investor valuations cannot be used for 409A compliance.

Myth 3: “It’s a One-Time Requirement”

Some think that a 409A valuation is a one-time need. However, it’s an ongoing requirement as long as the company continues to grant stock options.

Myth 4: “Only for Stock Options”

While stock options are the most common use case, 409A valuations also apply to restricted stock units (RSUs), stock appreciation rights (SARs), and other forms of equity-based compensation that require fair market value determinations.

Ready to Get a Defensible, Compliant 409A Valuation Report?

At Eton, we make it simple to get a valuation you can rely on.

You get the same technical rigor and audit-ready reporting you’d expect from a Big 4 firm (because many of our consultants were trained there), combined with the speed, accessibility, and personalized service of a boutique team.

Most 409A valuations are completed in ten days, and for startups on tight deadlines, we also offer a one-day expedited option.

Our work is 100% human, never automated. Every report is signed by qualified appraisers, fully USPAP-compliant, and safe harbor-eligible. That level of diligence is why our clients’ reports have consistently passed auditor and IRS reviews without issue.

We also tailor every engagement to your company’s stage.

Early-Stage Package: Designed for younger companies issuing their first options.

Late-Stage Package: Built for startups with multiple funding rounds or preparing for IPO.

Each package is priced fairly, aligned to your needs, and delivers the same level of accuracy and defensibility to satisfy investors, auditors, and the IRS.

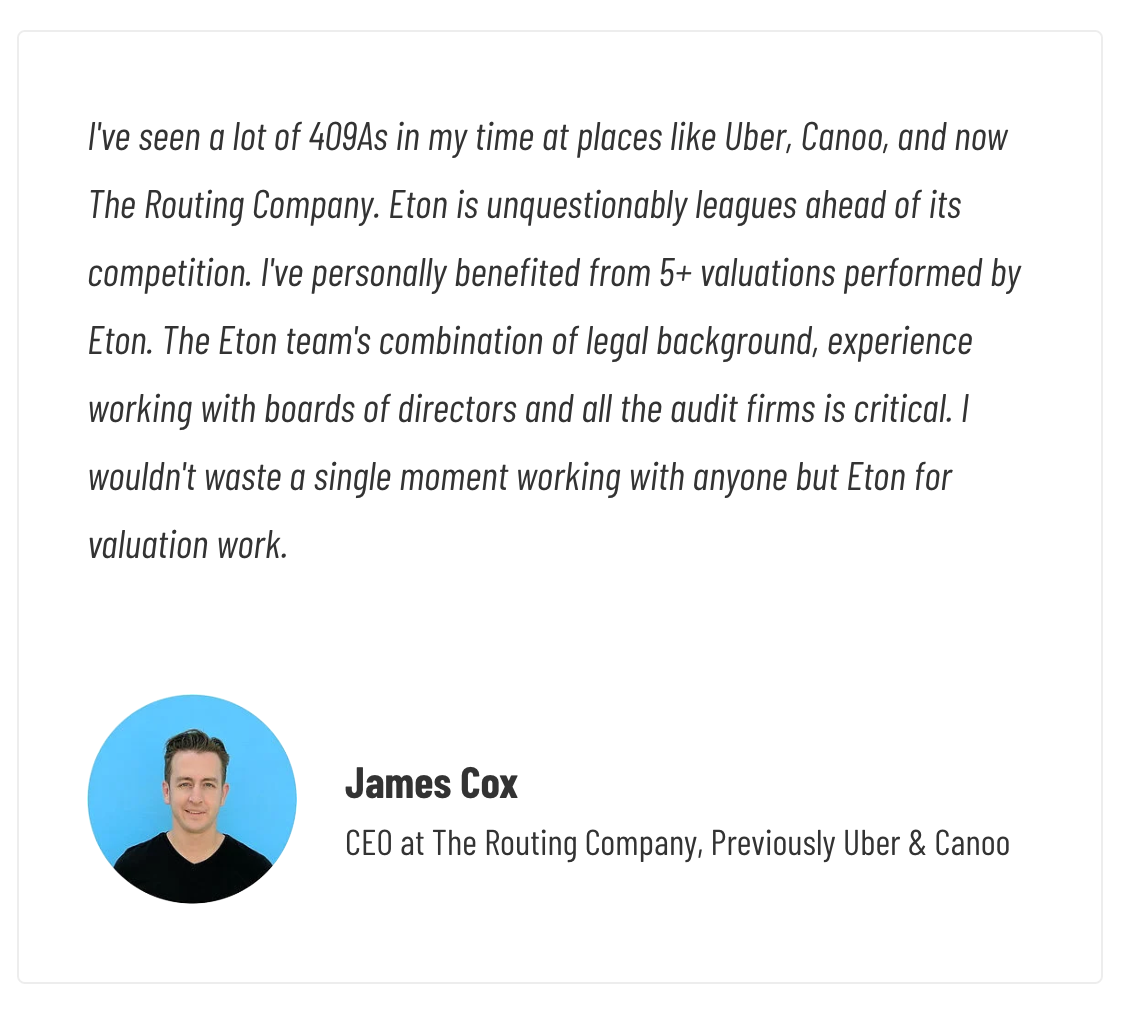

Here’s what one of our clients had to say:

With Eton, you’ll have peace of mind knowing your valuation is done right, delivered on time, and built to meet IRS 409A valuation requirements, all without the Big 4 price tag.

Ready to get started with a trusted, compliant provider?

A defensible 409A valuation is calculated using accepted methodologies under IRS guidance, typically the Market Approach, Income Approach, or Asset Approach.

Analysts consider financials, cap table, preferred pricing, market data, and risk factors to determine common-stock FMV.

At Eton, every calculation is fully documented and USPAP-compliant, giving you the assurance that your valuation is well-supported and will stand up to auditor or IRS review.

Can I do my own 409A valuation?

It isn’t recommended to perform your own 409A valuation because self-prepared valuations don’t qualify for IRS safe harbor.

Without safe harbor, your strike prices can be challenged, leading to tax penalties for employees and compliance risk for your company.

What does it take to achieve 409A safe harbor?

To meet 409A safe harbor, your valuation must satisfy several IRS requirements that collectively create a presumption of reasonableness.

In practice, that means the IRS can’t challenge your FMV unless they can prove it’s grossly unreasonable.

To qualify, your 409A valuation must:

Be documented in a written valuation report

Be completed and signed by an independent, qualified appraiser

Use reasonable, accepted valuation methodologies

Consider all relevant information as of the valuation date

Be updated every 12 months or sooner if a material event occurs

Meeting all of these criteria ensures your 409A valuation qualifies for safe harbor protection.

Eton structures every 409A appraisal around these exact requirements: each report is written, fully documented, independent, USPAP-compliant, and signed by qualified appraisers. We have a proven track record of delivering valuations that always pass auditor and IRS review.

How much does a 409A valuation cost?

Most startup 409A valuations cost $2,500-$4,000, depending on stage, complexity, and the level of expertise involved.

At Eton, we offer two packages, one for early-stage and one for late-stage startups, both priced fairly to ensure you get a defensible, IRS-compliant valuation without the high fees of larger firms.

What information do I need to prepare before getting a 409A valuation?

To complete a 409A valuation, most startups need to provide:

financial statements (if you have them)

financial forecasts (if you have them)

capitalization table

articles of incorporation

bylaws

stock option agreement

the deck you show investors

SAFE notes (if you have them)

convertible debt (if you have it)

straight debt (if you have it)

Eton streamlines this process and requests only what’s necessary, keeping the lift on your team as light as possible.

Does a pre-revenue startup need a 409A valuation?

Yes. A pre-revenue startup still needs a 409A valuation before issuing stock options. Even without revenue, the company must establish the fair market value of its common stock to set a compliant strike price and qualify for IRS safe harbor.

For early-stage companies with limited financial history, appraisers rely on methods such as the backsolve, option-pricing model, or asset approach, along with factors like recent funding terms, market conditions, and risk profile.

How long is a 409A valuation good for?

A 409A valuation is valid for 12 months or until a material event occurs, such as a new funding round, acquisition discussions, major revenue shifts, or secondary sales. After that, you must refresh your report before issuing new options.

How soon after a funding round should I refresh my 409A valuation?

You should refresh your 409A valuation immediately following a new priced round, as it’s a material event that typically increases your company’s fair market value. Grants issued after a round must use the updated FMV to stay compliant.

What happens if my 409A valuation is too low or too high?

A 409A valuation that’s too low can trigger immediate tax penalties for employees if the IRS determines options were granted below FMV.

A valuation that’s too high makes stock options less attractive to employees due to higher strike prices.

An accurate valuation (not artificially inflated or deflated) ensures compliance and preserves the effectiveness of your equity compensation.

How does a 409A valuation affect employees receiving stock options?

A 409A valuation sets the legal minimum strike price for employee stock options.

A lower (but defensible) FMV means a lower strike price and more potential upside for employees.

A higher FMV means a higher strike price and less potential upside.

Regardless of whether the FMV is high or low, it must be accurate and defensible, because options granted below true fair market value trigger IRS penalties for employees.

Do SAFE notes, convertible debt, or multiple share classes affect a 409A valuation?

Yes. SAFE notes, convertible debt, and multiple share classes all impact your 409A valuation because they add complexity to your capital structure.

Valuators must account for these instruments when determining how enterprise value is allocated to common stock.

How does a 409A valuation change as my company approaches IPO?

As a company nears IPO, the 409A FMV usually rises because liquidity risk (the difficulty of selling private shares) decreases as a public listing becomes imminent.

Analysts shift to using public market comparables, pre-IPO pricing indicators, and more sophisticated valuation models that reflect the company’s path to becoming publicly traded.

What should I do after receiving my 409A valuation?

Once you receive your 409A report, review it for accuracy, obtain board approval of the FMV, retain the report in your records for compliance purposes, and use the updated strike price for all option grants going forward.

get in touch

Let's talk.

Schedule a free consultation meeting to discuss your valuation needs.

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, internal / external counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.