Goodwill Impairment: Definition, Calculation & Case Studies

Goodwill Impairment

Written by Chris Walton, JD

Chris Walton, JD

President & CEO

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, legal counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.

Chris has led thousands of valuations, including for equity securities, intangible assets, financial instruments, investment valuations, business valuations for tax compliance and financial reporting compliance, as well as fairness and solvency opinions.

Goodwill impairment occurs when the carrying value of goodwill from a past acquisition exceeds its current fair value, meaning that the goodwill asset has lost value.

This can indicate that the expected benefits from the acquisition, such as synergies or market position, are not as valuable as initially anticipated.

Such situations can be daunting for business owners, investors and financial professionals, as questioning the value of previous acquisitions raises concerns about leadership’s decision making.

This guide is designed to help you navigate the challenges, risks, and testing process for goodwill impairment. We’ll also look five case studies that show the impact of unaddressed goodwill impairment.

What Is Goodwill and How Is It Initially Recognized?

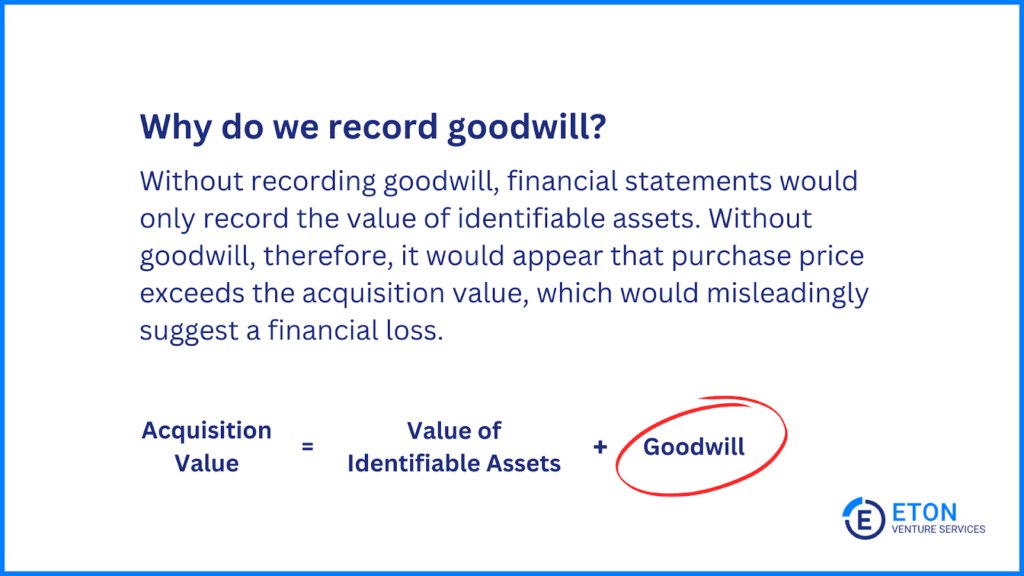

Goodwill is an intangible asset that arises when one company acquires another for a price higher than the fair value of its “identifiable assets”.

Identifiable assets include both tangible assets, like property, equipment, and inventory, as well as certain intangible assets that can be measured independently, such as patents, trademarks, or customer contracts.

Unidentifiable assets include more subjective things like brand reputation, customer loyalty, and employee expertise which can’t separately be measured.

For example, if Company A buys Company B for $5 million, but Company B’s identifiable assets are valued at $3 million, the $2 million excess is recorded as goodwill. This reflects non-identifiable factors like brand reputation, customer relationships, or employee expertise that the buyer expects to generate future economic benefits.

To understand impairment, it’s helpful to know how this process typically works as it sets the foundation for assessing any potential loss in value:

Revaluing assets and liabilities: All existing assets and liabilities in the acquired company’s balance sheet are revalued at fair value. Often, there aren’t significant changes here, but sometimes hidden assets or liabilities are identified.

Recognizing unrecognized assets and liabilities: Intangible assets that may not have been previously recorded—such as self-created brands or customer contracts – are recognized at their fair value.

Calculating goodwill: The difference between the purchase price and the fair value of the acquired net assets is then recorded as goodwill on the acquirer’s balance sheet.

What Is Goodwill Impairment? How Does It Work?

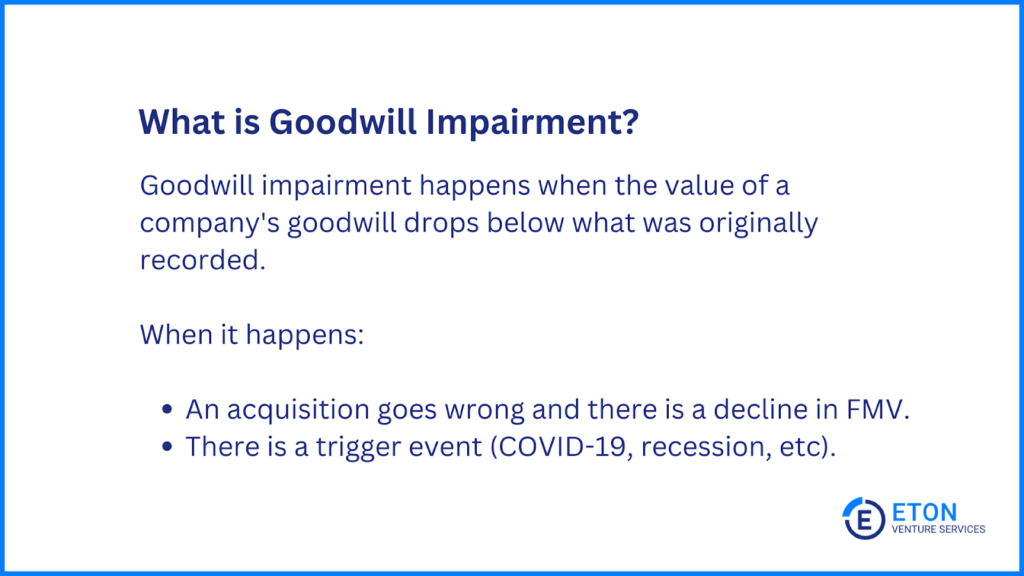

Goodwill impairment happens when the value of a company’s goodwill drops below what was originally recorded.

This happens for any number of “trigger” reasons, like when a business acquisition does not perform as expected or when external conditions change.

The impairment of goodwill is then recorded as an expense, directly decreasing the carrying amount of goodwill on the balance sheet.

For example, if you acquire a business for $5 million, recording $2 million of goodwill, but subsequent events suggest that the acquired business can no longer generate $1 million of anticipated returns, a goodwill impairment loss of $1 million might be recognized, reducing the goodwill value on the books.

In most cases, goodwill impairment is not good news. It signals that the value of the acquisition has dropped, reflecting a shift from the original plan.

It’s worth noting that, although investors and external stakeholders often see an impairment of goodwill as a signal of poor financial decision-making, these shifts aren’t always within management’s control. Sometimes, they result from forces beyond the company’s reach, such as economic recessions, competitive disruptions, and regulatory changes.

Triggering Events: What Causes Goodwill Impairment?

Triggering events are like warning lights for a finance team; they signal when it’s time to start goodwill impairment testing.

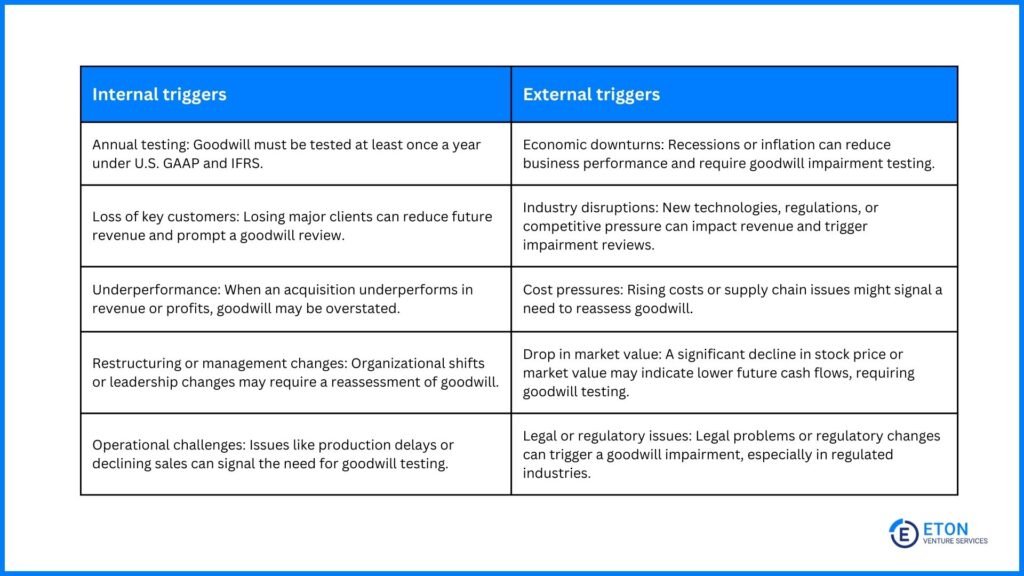

Goodwill impairment triggering events can be categorized into internal and external factors. Below, we’ve detailed the most important ones—read our full list of 30+ goodwill impairment triggering events here.

Internal Triggers

Annual testing: Goodwill impairment testing is required at least annually under accounting standards like U.S. GAAP and IFRS.

Loss of key customers: Losing a major customer or multiple important clients may significantly affect future revenue streams, prompting an impairment review.

Underperformance: Impairment happens when a company realizes that it overpaid for an acquisition because the acquired business or assets are not performing as well as expected. This could happen if the acquired company’s financial results, such as revenue or profits, are lower than anticipated, meaning the initial expectations of future economic benefits aren’t being met.

Internal restructurings or management changes: Organizational changes like restructuring, significant shifts in business strategy, or management turnover may alter previous business assumptions and lead to the need for goodwill impairment testing.

Significant operational challenges: Operational difficulties, such as production delays, can lead to reduced sales and require a goodwill reassessment.

External Triggers

Deteriorating macroeconomic conditions: Major economic disruptions such as recessions, inflation, or financial crises can reduce business performance expectations, making previously held goodwill valuations less justifiable. For instance, the 2008 financial crisis caused significant goodwill impairments across industries.

Industry disruptions and shifts: New technologies, regulatory changes, or evolving consumer preferences can trigger impairment tests. Competitive pressures or emerging market entrants may reduce an acquired business’s market share, impacting revenue forecasts.

Cost pressures: Supply chain disruptions, rising costs, or decreased profitability might signal that business assumptions have changed, necessitating a reassessment of goodwill.

A decline in share price or market value: A significant or prolonged decrease in a company’s stock price or overall equity value may indicate that the company’s future cash flows and performance are no longer in line with the assumptions made during the acquisition.

Regulatory and legal issues: Adverse legal rulings or changes in regulations can also trigger an impairment test, especially in highly regulated industries such as healthcare or finance.

How to Minimize the Risk of Goodwill Impairment

Goodwill impairment can be a tough reality, but it’s not inevitable. Fortunately, proactive measures can help reduce the risk and safeguard your financial health.

Here are key strategies you can implement throughout the acquisition process and beyond to protect your goodwill from unnecessary write-downs:

Thorough due diligence: Before acquiring a company, it’s essential to thoroughly evaluate its financial health, market position, and future growth potential to ensure the price you’re paying is justified.

Regular monitoring: Continuously track the performance of the acquired business. Regularly check if it’s meeting key financial targets like cash flow and profitability.

Seamless integration: Ensure the acquired company is smoothly integrated into your existing business to maximize its value.

Market watch: Keep an eye on market conditions and industry trends that might impact the value of the acquired company.

Transparent reporting: Maintain clear and honest financial reporting. Work closely with auditors and experts to get an objective view of the company’s performance.

By building these strategies into your routine, you’ll also be better equipped to handle goodwill impairment testing with confidence.

Goodwill Impairment Testing? 5 Things You Must Know Before Starting

When to test: Goodwill impairment testing is required annually under both ASC 350 and IFRS. Additionally, you must perform tests as soon as a triggering event occurs, such as economic downturns, significant changes in the business, or loss of key customers.

Where to test: Under ASC 350 (U.S. GAAP), goodwill is tested at the reporting unit level, which refers to a division or subsidiary that operates independently. Under IFRS, it’s tested at the cash-generating unit (CGU) level, which is the smallest identifiable group of assets that generates cash flows independently.

Key comparison metrics: For ASC 350, compare the fair value of the reporting unit with its carrying amount. For IFRS, compare the recoverable amount of the CGU (the higher of fair value less costs of disposal or value in use) with the carrying amount. If the carrying amount exceeds these values, an impairment loss is recognized.

Impact on financial statements: Impairment results in a non-cash charge, meaning the company reports an expense that reduces its net income without actually spending any cash. This can affect how investors see the company’s financial health, as lower net income may suggest weaker performance.

Documentation is critical: Thoroughly document the steps, assumptions, and results of your impairment tests to remain compliant with both ASC 350 and IFRS. This is key for audit readiness and regulatory reviews.

How to Calculate Goodwill Impairment Loss in 7 Steps

Once you’ve determined that goodwill impairment testing is needed due to a trigger event like a market downturn or changes in performance, the next step is calculating the impairment loss.

If your company is based in the U.S., you’ll use GAAP. For companies outside the U.S. or those doing international business, IFRS is the appropriate standard.

Understanding which framework to follow is important, as the calculations and requirements may vary between GAAP and IFRS.

For first-time acquirers in particular, this can seem overwhelming, but it’s necessary for keeping your financials accurate and compliant with these accounting standards.

Here are the main steps to guide you through this process:

1. Perform a Qualitative Assessment (Optional for U.S. GAAP)

Often called “Step Zero”, U.S. GAAP permits companies to begin with a qualitative evaluation of external and internal factors to gauge whether it’s more likely than not that a reporting unit’s fair value is below its carrying amount (i.e. goodwill has been impaired). If the likelihood is below 50%, the costly quantitative test can be skipped.

In contrast, IFRS mandates impairment testing whenever there are clear indicators of impairment, without an option for a qualitative step.

2. Identify Reporting Units or Cash-Generating Units (CGUs)

Next, it’s important to determine which reporting units (under U.S. GAAP) or cash-generating units (under IFRS) will be subject to the goodwill impairment test.

These units are the basis for evaluating potential impairment, as they represent the smallest identifiable business divisions that generate largely independent financial data or cash flows.

3. Conduct a Quantitative Valuation Test (if required)

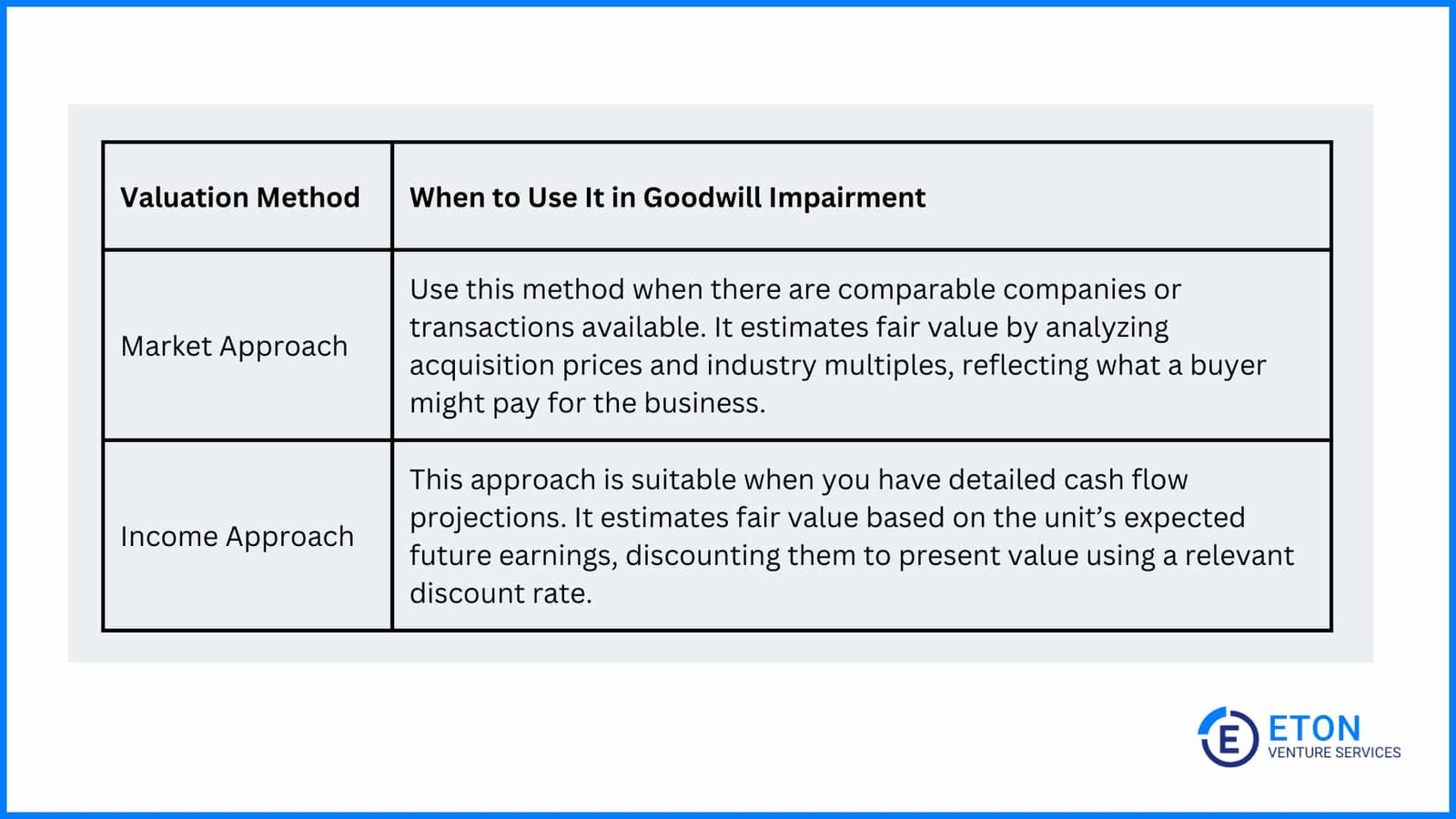

If the qualitative assessment suggests potential impairment, or if IFRS standards apply, the company must perform a quantitative test to determine the fair value of the reporting units (U.S. GAAP) or CGUs (IFRS).

This involves using recognized valuation methods, such as the market approach and income approach, either individually or in combination, depending on the business’s specific circumstances.

The selection of these methods is done on a case-by-case basis to ensure the most accurate valuation. Here are some factors to consider:

Management forecasts: Ensure that forecasts accurately reflect expected performance and align with historical data.

Business model: Understand the entity’s business model, especially for niche companies, as this can influence fair value considerations.

Comparable selections: Carefully choose comparable companies or transactions for the Market Approach; incorrect selections can distort the estimated value.

After running the quantitative test, it’s important to check that your fair value estimates aren’t too dependent on just one set of assumptions.

Sensitivity analysis helps by testing how changes in key factors, like discount rates, growth forecasts, or market conditions, affect the fair value of your reporting units or CGUs.

By looking at different scenarios, from best case to worst case, you can see how much the results might change and understand the risks involved.

5. Compare Fair Value with Carrying Amount

Under ASC 350, companies compare the fair value of the reporting unit, including goodwill, with its carrying amount. If the carrying amount exceeds the fair value, it suggests potential impairment.

Similarly, IFRS requires comparing the CGU’s carrying amount to its recoverable amount (the higher of fair value less costs of disposal, or value in use). If the carrying amount exceeds the recoverable amount, impairment is indicated.

6. Determine and Record Impairment Loss

Once impairment has been identified, the impairment loss is calculated based on the difference between the carrying amount and the appropriate fair value (ASC 350) or recoverable amount (IFRS).

The impairment loss is then recorded as an expense on the income statement, reducing net income for the period, and the carrying amount of goodwill on the balance sheet is reduced accordingly.

7. Disclose the Impairment

Finally, companies must disclose details about the impairment, including the financial impact and reasons behind it, to ensure transparency with stakeholders.

As you move through the steps of goodwill impairment testing, staying proactive is key to avoiding costly surprises.

Regularly monitoring both market conditions and internal performance can help you identify potential impairment triggers early.

By conducting periodic reviews and keeping your financial data up to date, you can address issues before they escalate, ensuring your business remains compliant and avoiding significant last-minute write-downs.

4 Real-World Goodwill Impairment Examples

Now, you might be wondering how goodwill impairment plays out in real-world scenarios. Below are some real-world goodwill impairment examples that illustrate how various businesses have experienced goodwill impairment due to different triggering events:

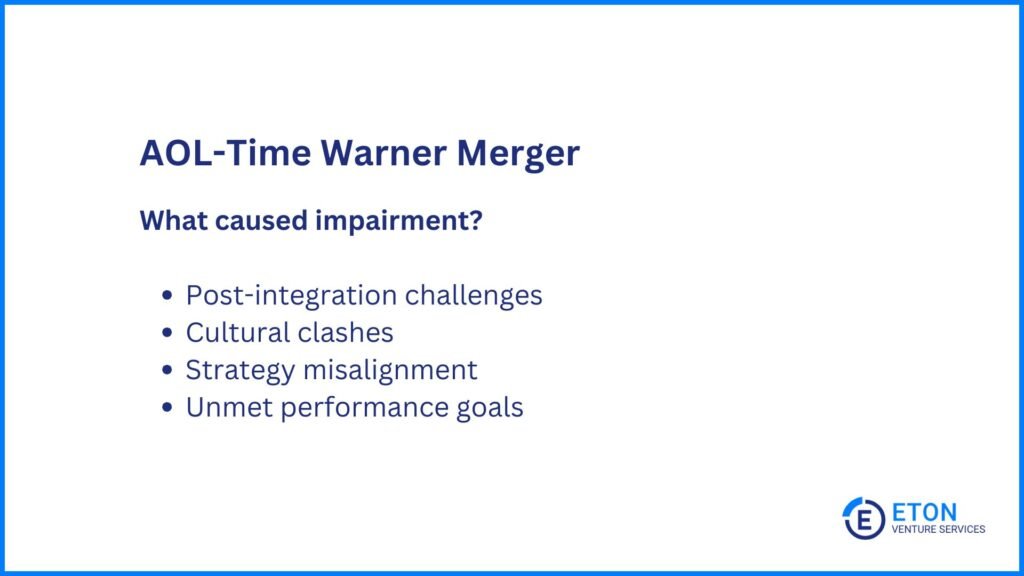

AOL-Time Warner Merger

The merger between AOL and Time Warner, once seen as a groundbreaking deal in 2000, quickly became an example of a business move gone wrong.

After the merger, the combined company struggled with internal issues like clashing corporate cultures and poor strategic decisions. They also faced a rapidly changing digital environment that they couldn’t keep up with.

By 2002, the company’s market value had dropped significantly below what was expected. This loss in value led to a large reduction in the company’s goodwill.

The downfall of AOL-Time Warner shows how challenging it can be to merge companies, especially when expectations aren’t met and market conditions change.

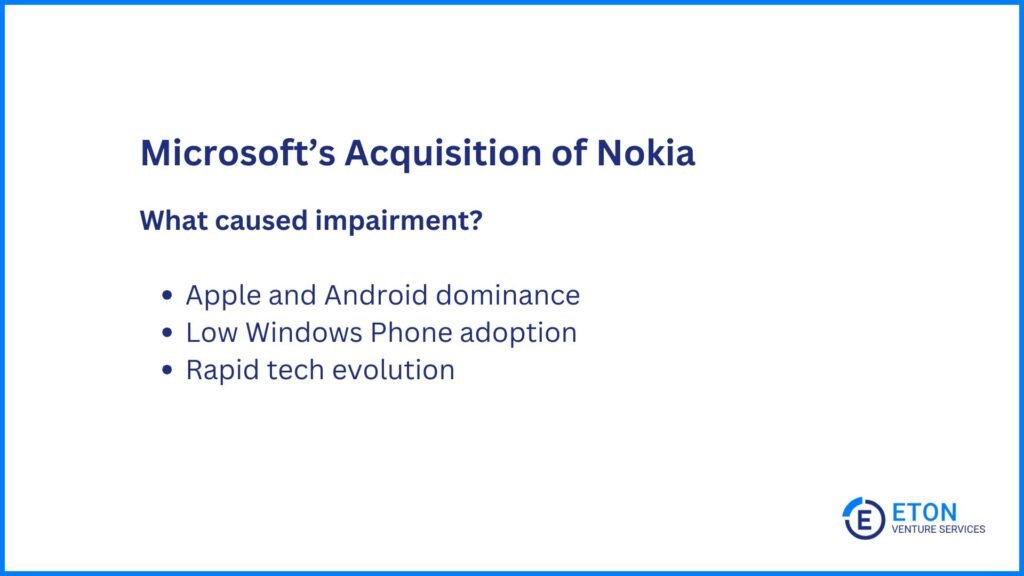

Microsoft’s Nokia Acquisition

In 2014, Microsoft acquired Nokia’s smartphone division for $7.9 billion to gain a foothold in the mobile market.

However, it soon faced strong competition from Apple and Android, and consumer interest in Microsoft’s Windows Phone remained low.

By 2015, Microsoft took a $7.6 billion goodwill impairment, nearly the entire acquisition cost, reflecting Nokia’s diminished value in a fast-evolving market.

This serves as a reminder of how quickly technological shifts can disrupt industries and diminish the expected value of an acquisition.

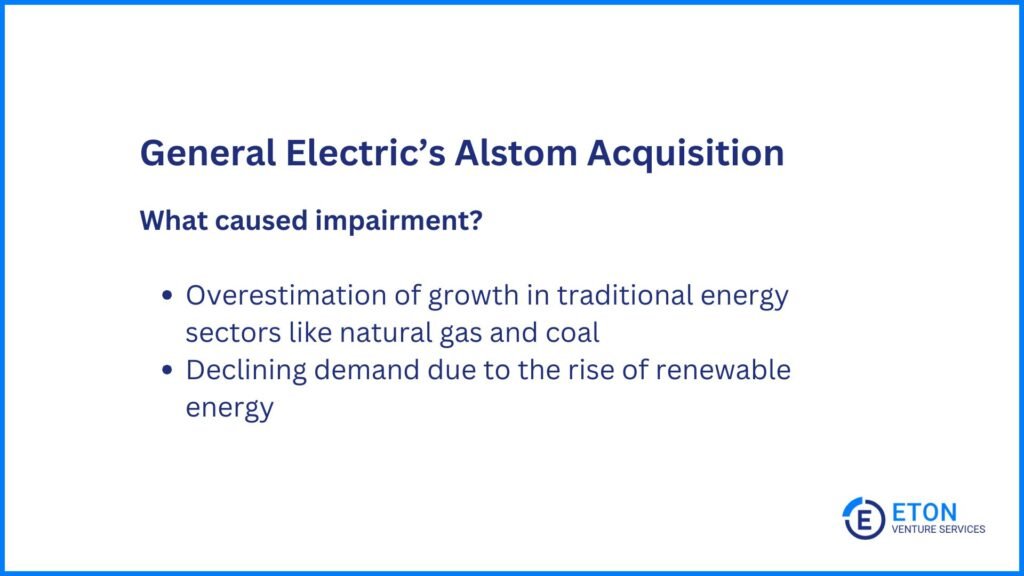

General Electric’s Miscalculation in the Energy Market

In 2018, General Electric (GE) recorded a $22 billion goodwill impairment, primarily related to its 2015 acquisition of Alstom’s power business.

GE anticipated substantial growth in traditional power generation, especially from natural gas and coal. However, as renewable energy gained traction, demand for fossil-fuel-based power declined.

This miscalculation led to a sharp drop in GE’s expected cash flows from the division, and the resulting impairment left its power business with no remaining goodwill.

This example highlights the risks of overpaying for acquisitions without fully considering shifting market trends, as well as the financial consequences that can follow.

Kraft Heinz’s Decline in Processed Food Market

In 2019, Kraft Heinz took a $15.4 billion goodwill impairment, largely due to the declining value of its Kraft and Oscar Mayer brands.

This massive write-down was caused by aggressive cost-cutting measures from 3G Capital, which reduced spending on research, development, and quality control.

These cuts hurt the company’s long-term brand strength and damaged customer relationships, forcing Kraft Heinz to reassess the value of its brands.

The impairment highlighted the risks of overestimating brand value and not adapting to changing market trends.

These case studies clearly show how factors such as market shifts, technological advancements, and strategic miscalculations can lead to significant goodwill impairments across industries.

They’re a good reminder for businesses to stay aware of potential risks and proactively manage their intangible assets to maintain value and protect their balance sheets.

Managing Goodwill Impairment to Protect Your Business

Goodwill impairment is more than a technical accounting adjustment. It reflects how real-world challenges, from market shifts to industry disruptions, can impact a company’s most valuable assets.

As highlighted in the examples above, businesses across industries have faced significant write-downs, underscoring the importance of proactive management of goodwill.

To accurately assess goodwill and avoid major financial impacts, it’s important to seek professional guidance. Experts help companies identify potential risks early, maintain compliance with financial standards, and provide clear and accurate valuations.

This support is necessary for avoiding misstatements, protecting financial health, and ensuring that a company’s balance sheet reflects its true value.

Goodwill Impairment | FAQs

Why is goodwill important in mergers and acquisitions?

Goodwill is important in mergers and acquisitions because it represents the premium paid for intangible assets that can’t be separately identified, such as brand reputation, customer loyalty, and market position.

These elements, although not recorded as individual assets, contribute to the overall value that the acquiring company expects to gain from the purchase.

By accounting for these intangible benefits, goodwill helps justify the price paid for an acquisition that exceeds the fair value of the identifiable net assets, reflecting the long-term potential the buyer sees in the acquired business.

How is goodwill recognized on the balance sheet?

Goodwill is recognized on the balance sheet when a company acquires another business, and the purchase price exceeds the fair value of the acquired company’s net identifiable assets and liabilities. The difference, known as goodwill, is recorded as an intangible asset.

During the acquisition process, the company revalues the acquired assets (both tangible and intangible) and liabilities to fair value, and any excess of the purchase price over this valuation is attributed to goodwill.

How do you know if goodwill is impaired?

Goodwill impairment is triggered by events such as declining cash flows, market downturns, changes in consumer behavior, or internal restructuring. Companies must then determine whether goodwill impairment has occurred through an impairment test, which evaluates whether the carrying value of goodwill on the balance sheet exceeds its recoverable amount, often measured by the fair value of the business unit.

If the business unit’s fair value falls below its carrying value, the impairment is recorded as an expense, reducing the value of goodwill on the balance sheet.

How often should companies test goodwill for impairment?

Goodwill must be tested for impairment at least annually. Additional tests are required if triggering events occur, such as significant declines in cash flows, market disruptions, loss of key customers, or economic downturns, which indicate potential impairment.

How does goodwill impairment affect investors?

Goodwill impairment offers investors a clearer understanding of a company’s true financial condition by recognizing that certain intangible assets may no longer provide expected future benefits.

While it improves transparency, a significant goodwill impairment can indicate deeper operational or market issues within the company, potentially leading to a drop in stock prices and reduced investor confidence.

As a result, large impairments are often seen as warning signals of underlying business challenges.

What are the tax implications of goodwill impairment?

The tax implications of goodwill impairment can vary based on the country’s tax laws and the company’s specific situation. Here are the main tax impacts:

Tax deduction: Goodwill impairment can be tax-deductible in some countries, reducing taxable income.

Timing differences: Financial reporting and tax rules may differ, leading to timing differences in recognizing the impairment for tax purposes.

Deferred tax assets/liabilities: Impairment can create deferred tax assets or liabilities, depending on how it’s treated for taxes.

Valuation: Determining the value of goodwill for tax purposes can be complex and may follow specific guidelines from tax authorities.

Tax planning: Companies can use goodwill impairment strategically to reduce taxes in certain jurisdictions.

In short, goodwill impairment can reduce a company’s taxes through deductions, but the specifics depend on local tax laws and how the impairment is treated for tax and accounting purposes.

get in touch

Let's talk.

Schedule a free consultation meeting to discuss your valuation needs.

Written by Chris Walton, JD

Written by Chris Walton, JD