Hi, I’m Chris Walton, author of this guide and CEO of Eton Venture Services.

I’ve spent much of my career working as a corporate transactional lawyer at Gunderson Dettmer, becoming an expert in tax law & venture financing. Since starting Eton, I’ve completed thousands of business valuations for companies of all sizes.

Read my full bio here.

A fairness opinion is a professional evaluation provided by an independent third-party expert to determine whether the price offered in a financial transaction, like a company buyout or merger, is fair to the shareholders.

Let’s say company A and B are negotiating for a merger/acquisition.

Company A says it will buy Company B for $40 billion.

To make sure this is a fair deal, Company B’s board of directors will hire a third-party, independent Fairness Opinion Services firm to assess whether $40 billion is fair or not.

Fair to whom?

In this situation, it’s likely the shareholders of Company B because essentially they are the “true” owners of the company and they will be compensated when the company gets bought out.

For some situations, fairness opinions are mandated by the SEC. In other situations, company directors and investors get fairness opinions to:

If anyone questions their decision, the involved parties can use the fairness opinion to prove that their choice was fair and reasonable.

Fairness opinions are completed by investment banks and independent transaction advisory and valuation firms.

They bring a comprehensive suite of financial services, including mergers and acquisitions (M&A) advisory and strategic financial planning, coupled with deep market knowledge and extensive deal-making experience.

But, they can be expensive and might not always be fully unbiased because they often work on the deals they’re reviewing.

Because of the sheer scale of their operations, they might also not be able to give each client as much personal attention.

Independent firms like Eton provide fairness opinion services that are conflict-of-interest-free, robust, and thorough.

We specialize in fairness opinions and transaction opinions, which means we’re experienced in the process and offer reports that stand up to all outside scrutiny—and we’ll be there to defend our opinion reports if needed.

Reach out to us here to learn more about our process and fees.

Let’s look at three real-world examples of fairness opinion letters submitted to the Securities and Exchange Commission (SEC), the U.S. government agency responsible for regulating the securities markets and protecting investors.

These examples will give you a clear understanding of what to expect and how to prepare when hiring a fairness opinion firm.

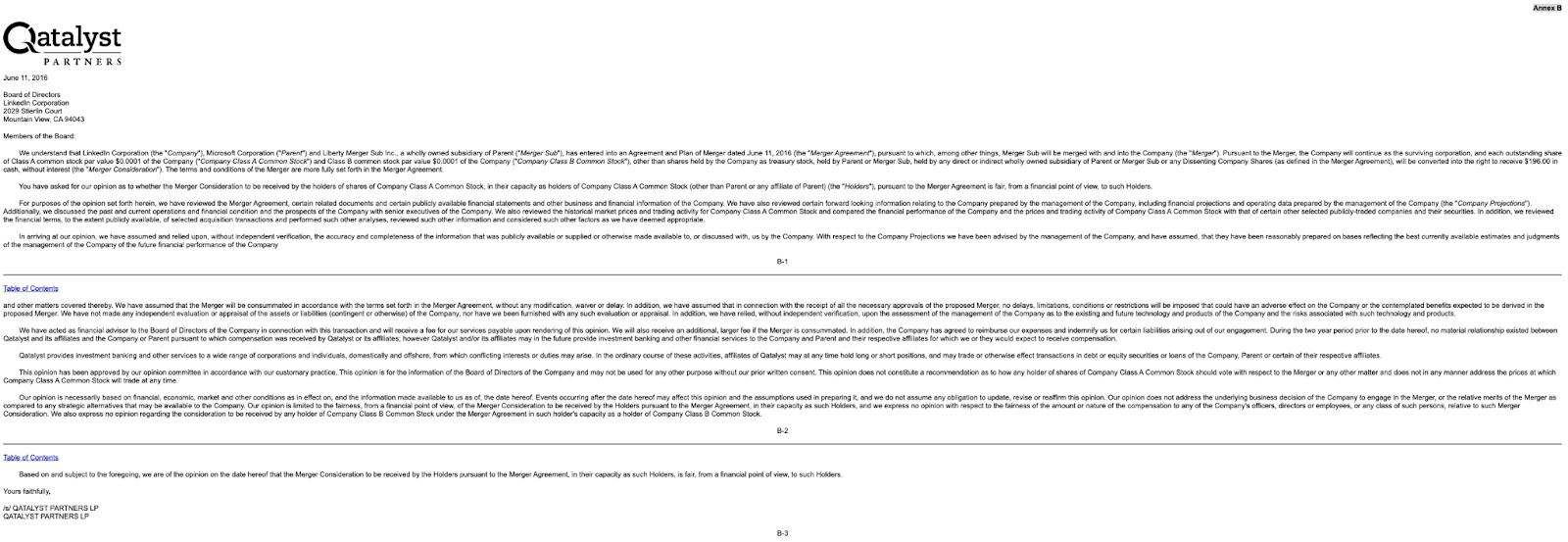

Here are the details of the fairness opinion received by LinkedIn:

The letter from Qatalyst Partners to LinkedIn’s Board of Directors said that after looking at the details of the merger with Microsoft, they believe the $196 per share price is fair.

This opinion was based on various financial analyses and was given because Qatalyst was helping advise LinkedIn during the deal.

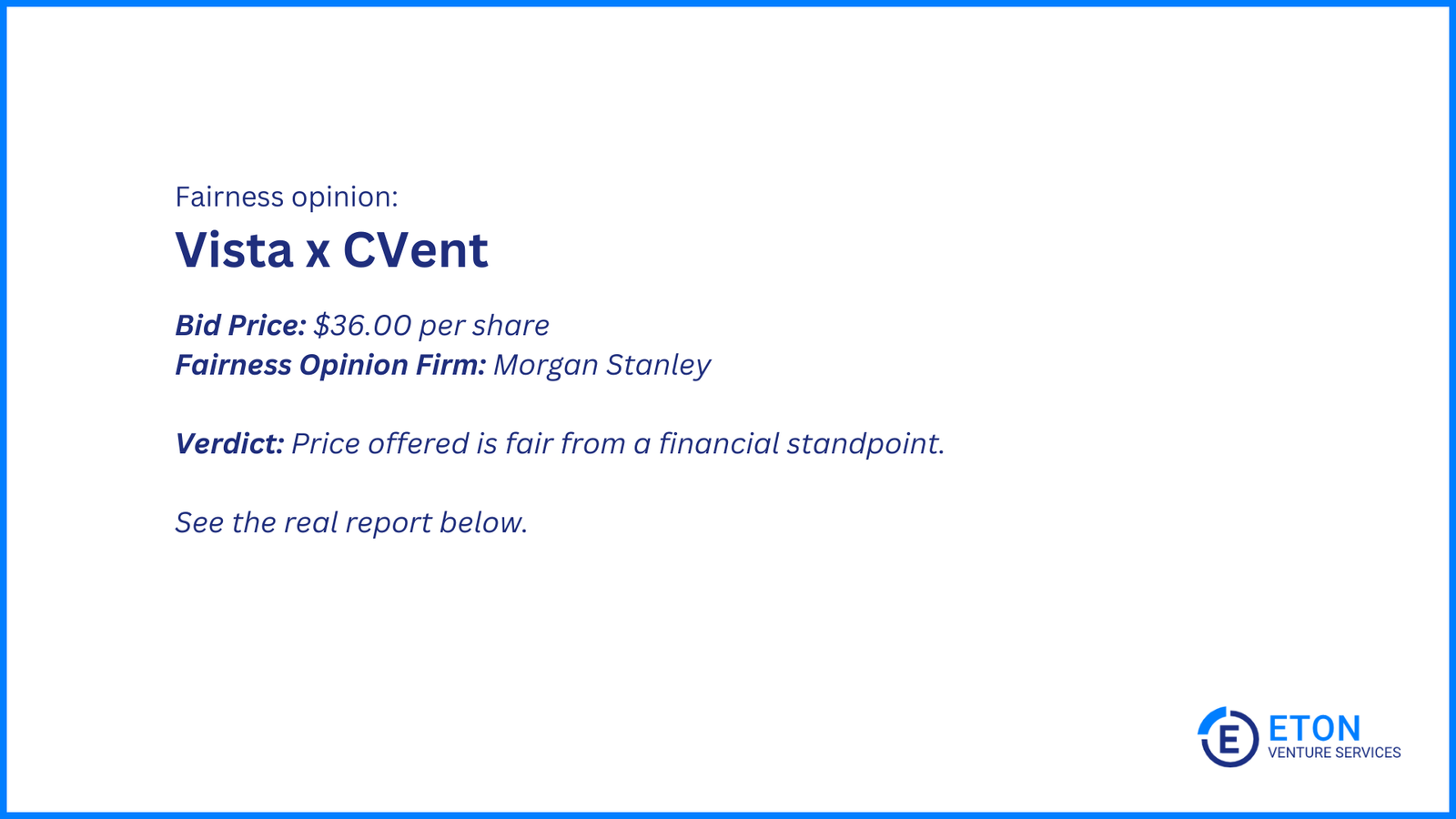

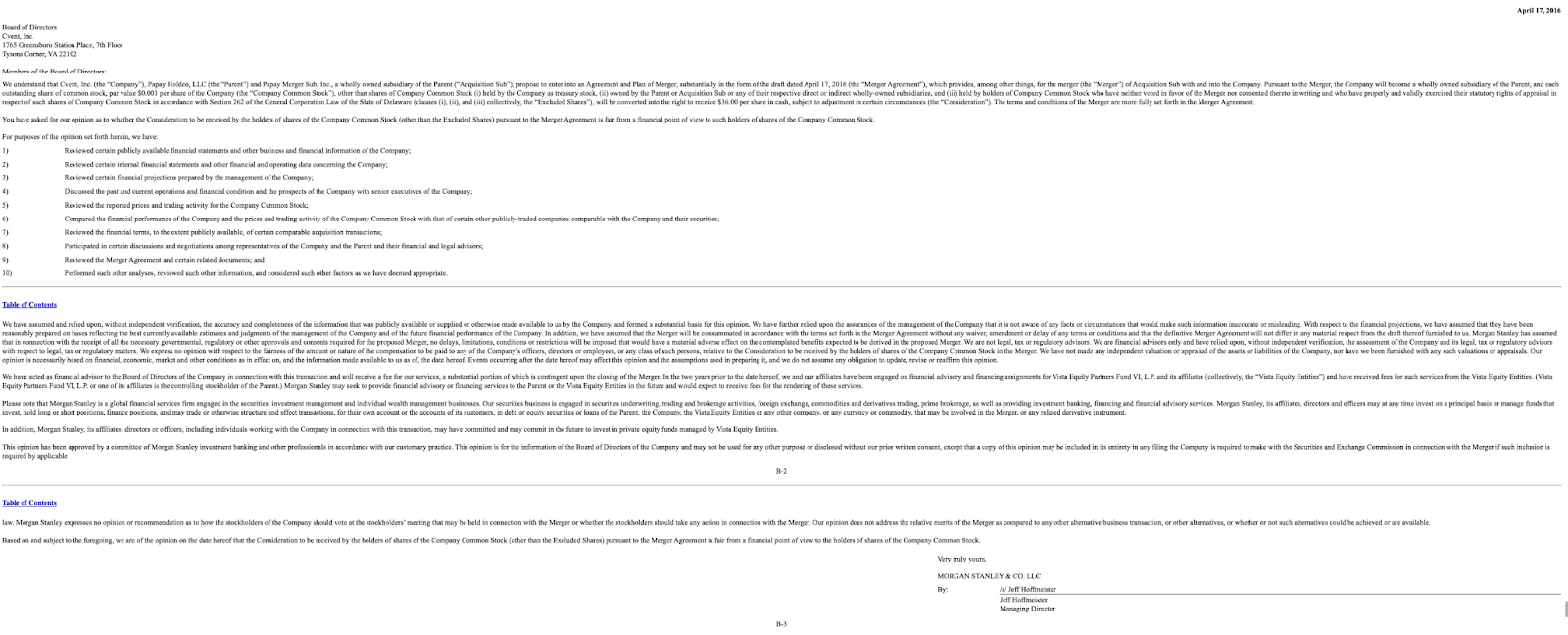

Here are the details of the fairness opinion received by CVent:

The letter from Morgan Stanley to Cvent’s Board of Directors said that the $36.00 per share price offered in the merger with Vista Equity Partners is fair.

This opinion was based on the information they had at the time and would only stay valid if the merger goes through without big changes.

Morgan Stanley also made it clear that they weren’t telling shareholders how to vote on the merger.

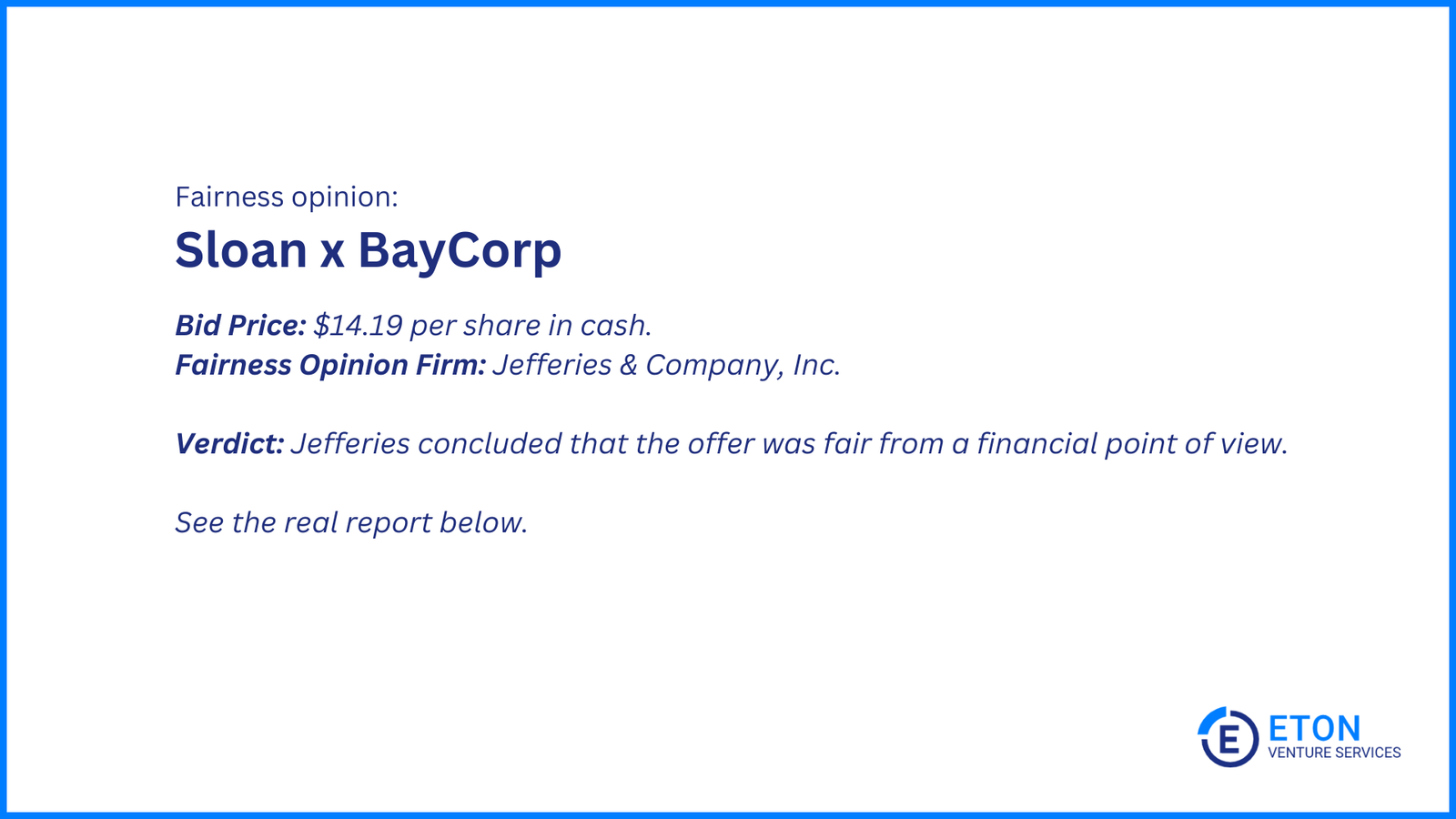

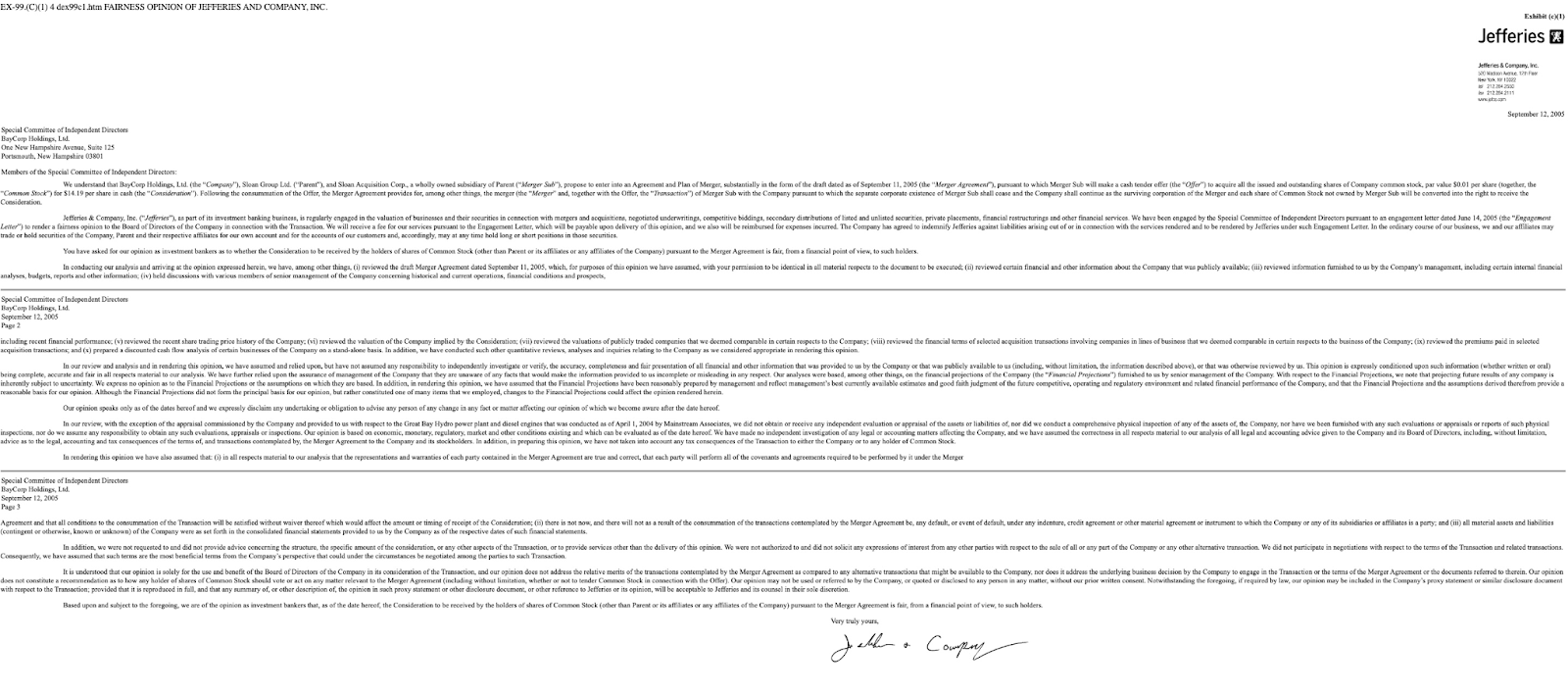

Here are the details of another fairness opinion provided by an investment firm.

Jefferies trusted the information they were given and did not do their own separate checks.

After their analysis, Jefferies decided that the $14.19 per share offer was fair for BayCorp Holdings’ shareholders.

There are three main methods experts use to conduct fairness opinion valuations:

Let’s look at each of them in detail.

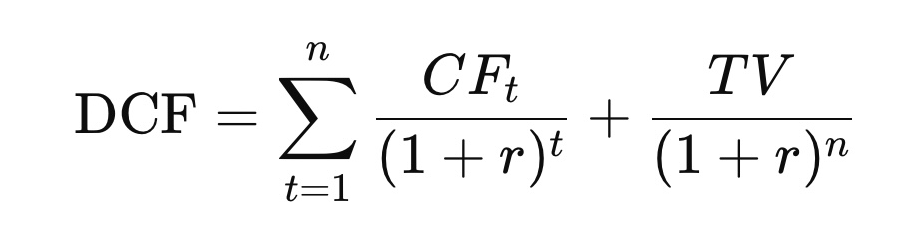

One of the most popular M&A valuation techniques is the discounted cash flow (DCF) analysis.

This method estimates the value of a company based on projected future cash flows.

Analysts forecast the company’s free cash flow for a set number of years, then calculate a terminal value to estimate the cash flow beyond the forecast period.

These future cash flows are then discounted to their present value using the company’s weighted average cost of capital.

This method takes into consideration the time value of money, recognizing that money received in the future is worth less than money received today.

When experts use it: Used for businesses with predictable, stable cash flows and a record of historical financial data.

The basic formula for DCF is:

Where:

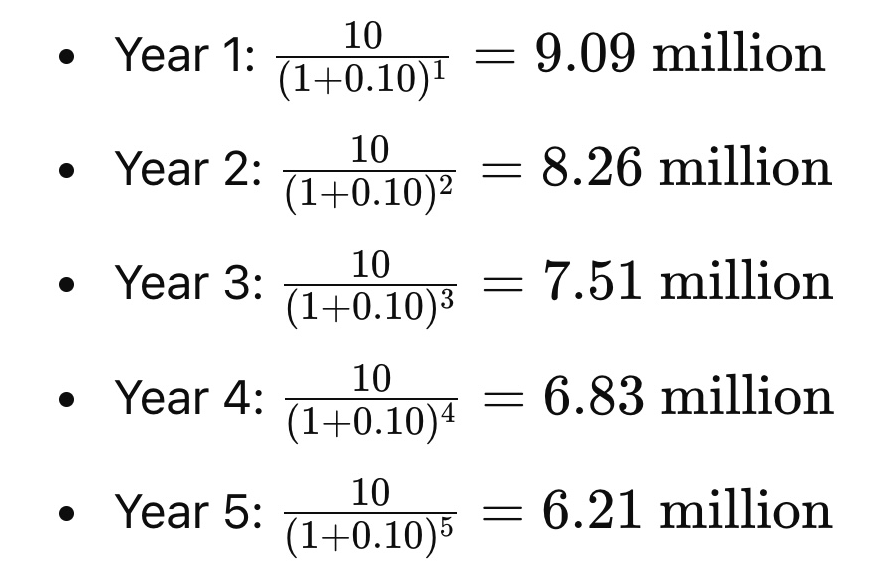

Example:

Suppose a company is expected to generate $10 million in cash flow annually for five years. The discount rate is 10%. The DCF calculation for these cash flows would be:

Adding these gives a DCF of approximately $37.90 million, plus the terminal value. This helps assess if the offered price aligns with the company’s true value.

The comparable company analysis determines a company’s value based on the multiples of similar public companies.

Analysts select comparable companies based on factors like:

Common multiples used are

The average multiples of the comparable companies are then applied to the target company to estimate its value.

When experts use it: CCA is a critical part of the assessment done during fairness opinion as it provides a market-based perspective.

Formula:

Value of Target=Average Multiple of Comparable Companies×Target’s Financial Metric

Example:

If comparable companies in the target’s industry trade at an average EV/EBITDA multiple of 8x and the target company’s EBITDA is $50 million, the estimated value would be:

Estimated Value=8×50=400 million

This method helps assess whether the acquisition price aligns with the market value of similar companies.

The precedent transactions analysis evaluates previous M&A deals in the same industry to determine a company’s potential value.

Analysts review recent acquisitions of comparable companies and apply the same revenue or EBITDA multiples to estimate the value of the target company. When experts use it

PTA is used in M&A to gauge the fair value of a company by referencing recent, similar transactions, especially in the same industry.

This method depends heavily on available data on precedent deals, which can sometimes be limited.

Formula:

Value of Target=Transaction Multiple of Comparable Deals×Target’s Financial Metric

For example, if recent deals were made at 3-4x revenues, then a target company with $50 million in revenues might be valued at $150-200 million.

Read more: M&A Valuation Methods: A Comprehensive Guide to Exploring 6 Different Approaches

Obtaining a fairness opinion is a critical step in ensuring that a proposed M&A transaction is fair to shareholders. Here’s a step-by-step breakdown of what CEOs and board members need to do to hire a fairness opinion firm and get the report:

At Eton, we’re a boutique team of Stanford Law lawyers and Ex-Big 4 Consultants.

We have done thousands of M&A advisory, valuations, and fairness opinions for the last 20 years.

We complete a fairness opinion report in under 10 days and at a reasonable cost.

We not only provide accurate fairness opinion assessments, but will also defend them in court if needed.

Eton’s M&A Valuation Services include:

Clients have praised our thoroughness, timely delivery, and audit-defensible valuations:

Ready to get started? Book a call to discuss your fairness opinion needs today!