Hi, I’m Chris Walton, author of this guide and CEO of Eton Venture Services.

I’ve spent much of my career working as a corporate transactional lawyer at Gunderson Dettmer, becoming an expert in tax law & venture financing. Since starting Eton, I’ve completed thousands of business valuations for companies of all sizes.

Read my full bio here.

I’ve worked on valuations for a range of chiropractic practices, and many of them are quite profitable. But when you’re valuing one, what matters most is whether those revenue streams will continue.

In my experience, the key is to understand the financial results and the factors that support their sustainability. These include:

These are the details that distinguish strong businesses, and they’re just as important as the company’s bottom line. Once I have those details, the next step is translating them into a solid figure using the right valuation methods.

The rest of this article explains how these valuation methods work and when each of them makes the most sense.

Key Takeaways

|

To value a chiropractic practice, we typically use one or a combination of the following valuation methods:

Each method uses a different approach to figure out what your clinic is worth. Some rely on sales data from similar practices. Others use expected future earnings to estimate value. And some value your physical assets when those matter more than its income or growth potential.

The right method depends on how the clinic earns and sustains its income, and whether it has room to grow or risks that could affect its value.

Here’s how each method works and when to use it:

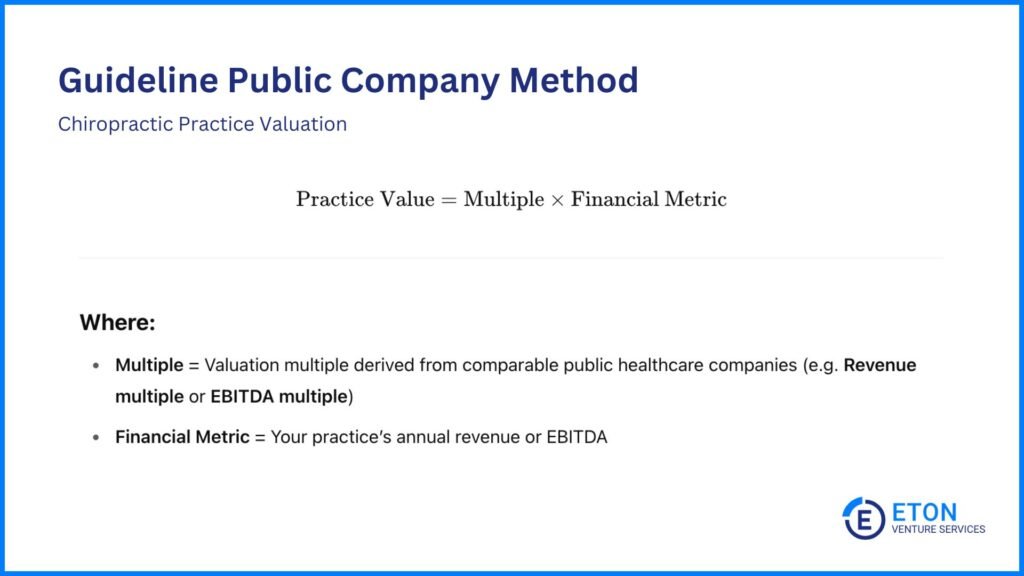

The GPC Method compares your chiropractic practice to similar companies that are traded on public stock markets. It’s useful when reliable market data is available from similar public healthcare providers.

To apply it, we first look for public companies that are similar to yours in size, revenue model, and industry classification.

Once we’ve found those matches, we look at their valuation multiples to see how the market values them. These ratios show how much investors are willing to pay for each dollar of revenue or earnings. For example, if a public company earns $5 million in EBITDA and its valuation is $25 million, it’s trading at a 5x EBITDA multiple.

The two most common multiples we use for chiropractic practices are:

Once we identify the relevant multiple, we apply it to your practice’s financials to estimate value. So, if your clinic earns $400,000 in EBITDA and comparable companies trade at 5x, your company’s value would be $2 million.

A higher multiple often signals stronger fundamentals like steady patient volume, a solid reputation, and systems that keep the clinic running smoothly. It also reflects things like how dependent the clinic is on one provider, how revenue is split between cash and insurance, and whether there’s room to grow without major changes.

However, those traits don’t always show up in public filings. So, we use professional judgment to interpret what likely drove the multiples in the public comps, and then assess whether your clinic has similar strengths or risks. If it does, applying the same multiple might make sense. If not, we adjust it up or down to better reflect your situation.

For example, if your clinic has strong patient retention, multiple providers, and growing revenue, we might adjust the multiple from 5x to 5.5x or even 6x. That would raise your value, putting it in line with what the practice is really worth.

On the other hand, if the clinic relies heavily on one chiropractor or has flat growth, we might lower the multiple to 4x or 4.5x to reflect those risks.

Finally, we apply a discount to account for private market realities. Public companies benefit from transparency and liquidity. Their financials are public, and their shares are easy to trade. Private clinics don’t offer that kind of access, which can make them less appealing to some buyers. So, we adjust the final value to account for lower visibility and flexibility.

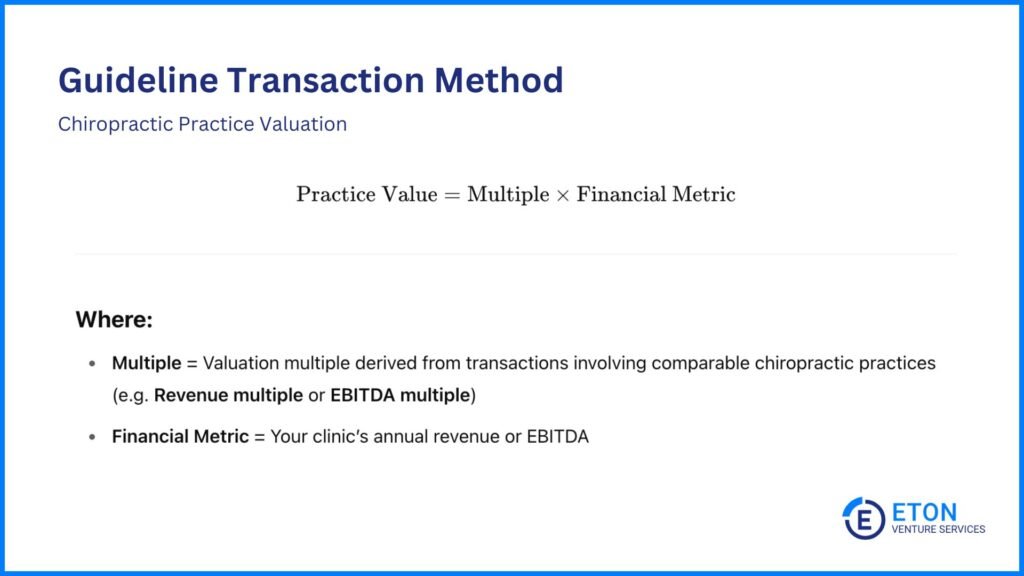

While the GPC Method compares your clinic to public companies traded on the stock market, the GT Method looks at what chiropractic practices actually sell for

To apply this method, we look at recent sales of practices similar in size and speciality. From these deals, we extract valuation multiples (like revenue or EBITDA multiples) and identify a range or average.

Then, we adjust the multiple up for stronger fundamentals, or down if there are added risks.. We then apply it to your clinic’s financial metrics.

For example, if a comparable clinic sold for 3x EBITDA and your clinic earns $500,000 in EBITDA, that gives a starting value of $1.5 million (3 x $500,000).

But if, based on our analysis, your clinic shows stronger patient retention, a more balanced payer mix, and systems that reduce reliance on any one person, we may adjust the multiple up.

On the other hand, if there’s high key person risk or limited growth potential, we adjust the multiple down to better reflect your clinic’s specific risks.

We also factor in the context behind each deal:

The goal is to land on a number that reflects the real value of your clinic, not just what someone paid under unique conditions.

Need third-party valuation help? Explore our guide to the top healthcare valuation firms and find the right partner for your business.

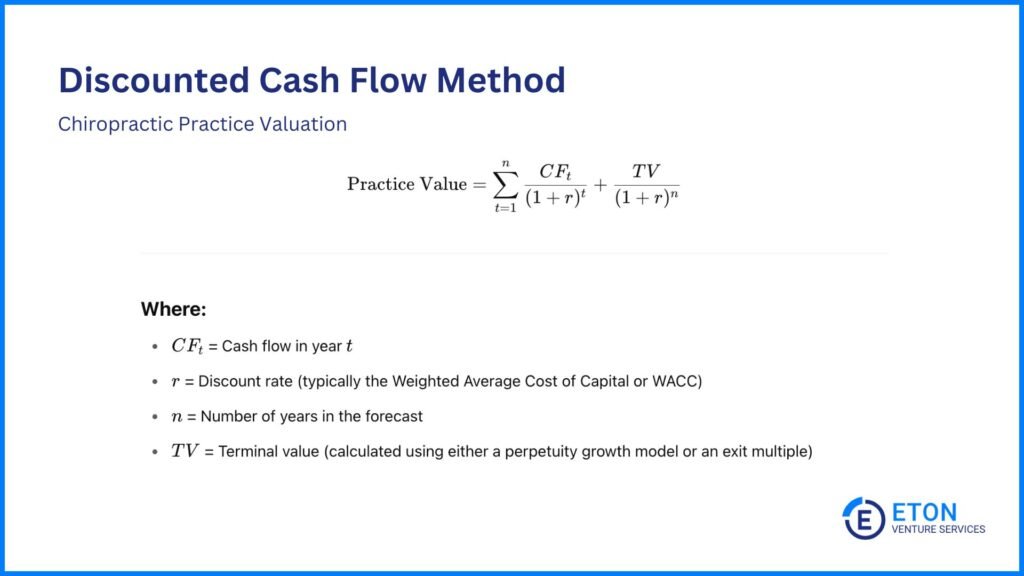

Unlike GPC or GT, which compare your clinic to others, the DCF method values your clinic based on its own projected earnings. It estimates what your practice is worth by projecting the cash it will earn in the future and adjusting that for risk and time.

And because it relies on cash flow projections, it’s best for well-established chiropractic practices with steady patient flow, consistent billing, and predictable cash flows.

Here’s how it works, step by step, with a simple example to walk you through:

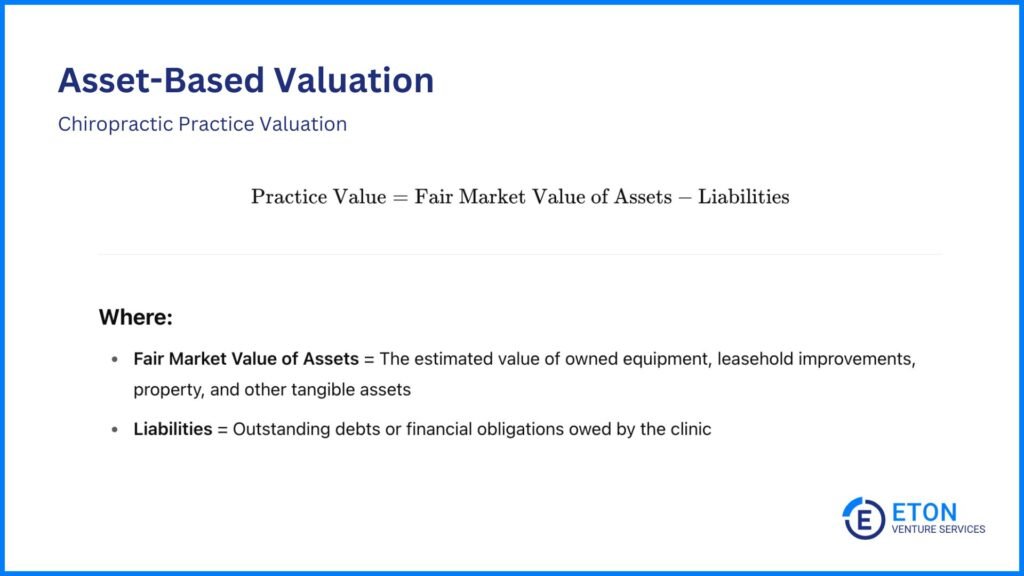

The Asset-Based Valuation method looks at what your clinic owns and subtracts what it owes.

It’s best for small or early-stage practices where profitability hasn’t caught up yet to rely on income-based methods like DCF. It also works for practices with valuable fixed assets like owned property or high-end equipment, like digital X-ray systems and decompression therapy tables.

To apply it, we estimate the fair market value of the clinic’s assets (like equipment, leasehold improvements, or owned real estate), then subtract any liabilities.

Let’s say your clinic owns $800,000 worth of equipment and improvements, and you have $200,000 in outstanding liabilities. Your value would be: $800,000 – $200,000 = $600,000.

However, this method has its limits. It doesn’t account for things like patient loyalty, a strong online presence, or efficient systems. These intangible strengths may not show up on the balance sheet, but they still influence value.

So, when possible, we combine this method with others, like DCF or GT. There are two ways to do this:

Need help getting a rough estimate of your chiropractic practice’s value? Use our free medical practice valuation calculator.

Profitability matters and is definitely something we look at when valuing chiropractic clinics. But it’s only one part of the story. Just as important are the factors that make that profitability sustainable.

For buyers and investors, things like patient retention, payer mix, reputation, and technology explain how reliable those profits are and shape how they view risk and long-term potential.

Valuation experts play a huge role here. We analyze these drivers, highlight their impact, and make the case for how they shape your practice’s overall value.

Here’s what we look at and how it impacts the valuation of your clinic:

Steady patient volume shows that the clinic has a reliable revenue stream. But what matters even more is retention. Are people coming back for ongoing care, or is the clinic always chasing new visits?

A practice that sees most patients return for care every few weeks is much more appealing than one that’s constantly starting from zero. High retention lowers marketing costs and signals trust. It also gives buyers confidence that revenue will continue post-sale.

Cash-paying patients usually mean quicker payments and fewer billing issues. They also give the clinic more control over pricing since fees aren’t limited by insurance reimbursement rates.

Still, insurance isn’t necessarily a drawback. Many clinics earn steady income from insurers, especially when they’ve built efficient billing systems and have solid contracts in place.

What matters is the balance. If a clinic gets 80% of its revenue from one insurer and that insurer changes its policies, it could create a serious drop in income. This payer concentration risk affects many rehabilitation practices – physical therapy practice valuation faces similar challenges with insurance dependency. A more even mix between cash and insurance or across multiple payers spreads the risk and protects long-term value.

If one chiropractor handles most treatments, knows all the patients, and manages the operations, the business can feel too tied to them. That’s risky for buyers.

But if the clinic runs smoothly with support staff, shared responsibilities, and systems in place, it’s easier to transition ownership without losing patients or momentum. This setup supports post-sale stability and increases value.

Can the clinic grow without major structural changes or costly expansion? Buyers look for signs that revenue can increase using the clinic’s existing demand or setup.

For example, if a clinic has more demand than it can currently handle, adding another chiropractor could increase revenue. While this adds some overhead, the extra income often outweighs the cost, especially when the space, systems, and patient flow are already in place.

Such built-in growth opportunities are a sign of long-term upside, which supports a stronger valuation.

What people say about your clinic carries real weight. Positive reviews, word-of-mouth referrals, and a good standing in the community all show that patients trust your care.

If the reputation is tied to the clinic as a whole, not just one chiropractor, it’s a big plus. It means patients are more likely to stick around after a sale, and new patients are more likely to come through the door. Buyers see this stability and goodwill as a major value driver.

Efficient systems reduce workload, save time, and create a better experience for patients and staff. Clinics that use modern tools for scheduling, billing, and recordkeeping tend to run more smoothly and avoid costly mistakes.

Strong systems also make it easier to handle growth without creating bottlenecks or relying too heavily on one person. This operational reliability supports a higher valuation because it signals consistency and scalability.

Regulatory issues can derail a deal fast. That’s why we look closely at how well a clinic handles compliance and licensing.

Are the right business and professional licenses in place? Are insurance policies current? Are treatment records, billing systems, and documentation organized and complete?

A well-run clinic will have all of this ready to go. But if things are missing or disorganized, it can raise red flags during due diligence. For example, if patient records are incomplete or billing practices seem inconsistent, it may lead to delays, legal concerns, or price reductions.

Clean compliance and up-to-date licensing tell us the clinic is well-managed and prepared for a smooth transition. It reduces the risk of regulatory issues down the line and gives more weight to reported financials. This adds to overall value and makes the practice easier to sell.

At Eton Venture Services, we provide accurate, independent valuations that support your decision-making, whether you’re planning for growth, preparing for a transaction, or structuring a transition.

Our team of experts is dedicated to offering the highest level of service in assessing the value of your chiropractic practice. We ensure that all key factors, such as patient volume, key person risk, payer mix, reputation, and more, are thoroughly considered.

Trust our experts to deliver insightful, tailored valuations that support your next move.

Yes, it can. But we usually value the clinic and the property separately.

If you’re selling both, the total value will be higher. Owning the building also adds stability, which can make your clinic more appealing to buyers.

But if you’re only selling the business, the real estate isn’t part of the valuation. It might still help with negotiations if you’re offering a good lease.

Equipment adds value when it’s in good condition and actively used to treat patients or improve efficiency. We include it in the valuation if it supports revenue or reduces workload. But if it’s outdated or rarely used, it may not make a difference.

Profit is important, but it’s not the only thing that matters.

We look at the full picture. If your clinic has loyal patients, steady volume, and signs of growth, it may still hold strong value. Maybe you’ve been reinvesting or recently expanded. Those moves can lower short-term profit but support long-term strength.

In cases like this, we may rely less on methods that use earnings, like DCF, and put more weight on things like asset value or comparable practice sales.

Low profit today doesn’t always mean low value. What matters is the story behind the numbers.

We start by understanding why growth is flat or falling. Is it due to market changes, increased competition, or something temporary like staffing issues?

If the slowdown seems fixable, buyers may still see value, especially if the clinic has loyal patients, strong systems, or solid earnings. But if there are deeper issues, we may adjust the valuation down to reflect that risk.

We also look at whether the clinic is still profitable and how it compares to similar practices. A flat-growth clinic with stable income can still hold value. It just may not get the same multiple as a fast-growing one.

Yes, but we account for them by looking at performance over a full year or even several years. If your clinic has busy and slow seasons, that’s normal in many areas. What matters is how consistent the overall yearly revenue and patient volume are.

We also look at whether those seasonal patterns are typical for your region or signal something else, like inconsistent marketing or scheduling issues. The goal is to understand the bigger picture, not just one strong or weak quarter.

Schedule a free consultation meeting to discuss your valuation needs.

Chris Walton, JD, is President and CEO and co-founded Eton Venture Services in 2010 to provide mission-critical valuations to private companies. He leads a team that collaborates closely with each client’s leadership, board of directors, internal / external counsel, and independent auditors to develop detailed financial models and create accurate, audit-ready valuations.