Written by Chris Walton, JD

Written by Chris Walton, JDThrough my work valuing different physical therapy practices, I’ve seen time and again that continuous care drives stable earnings. Patients don’t just come in once. They book weeks of sessions and often return for maintenance check-ins. That “need-based” demand is the backbone of a PT clinic’s cash flow.

But to set a fair price for your PT practice, cash flow is only part of the story. We also need to assess how reliable and sustainable this cash flow is and then value your practice on that basis. To do this, we look at a handful of factors, including:

The answers to these questions reveal how a PT practice’s cash flow holds up month after month. Next, we apply the appropriate valuation methods to turn those insights into a defensible price.

The rest of this article explains how these valuation methods work and when each of them makes the most sense.

Key Takeaways

|

To value a physical therapy practice, we typically use one or a combination of the following valuation methods:

Each method looks at your practice through a different lens.

Some methods, like GPC or GT, use market data to show what buyers are actually paying for similar businesses.

Others, like the DCF Method, dig into your internal performance and project future earnings based on patient flow, treatment patterns, and seasonal trends.

And the asset-based approach zeroes in on the physical assets you own, especially when those matter more to your practice’s value than earnings or future potential.

Now, let’s take a closer look at these valuation methods: how they work, when they apply, and what they reveal about your clinic’s true value.

To value your PT practice, the Guideline Public Company Method looks at publicly traded companies with similar business and financial profiles. It works best when there are enough comparable public peers and data points.

Once we find public companies that are a good match, we look at their valuation multiples to see how the market prices them. These multiples show us how much buyers were willing to pay for each dollar of sales or profit. We then apply them to your practice’s own financial metrics to determine its value.

For example, if similar public companies trade at 2x revenue, and your practice brings in $1.2 million in annual revenue, its value would be $2.4 million.

The two most common multiples we use for physical therapy practices are:

Tip! You can find these multiples in financial databases, company reports, and online platforms like Bloomberg Terminal that track financial data for public companies.

Investors are often willing to pay a multiple of sales or profit because they’re valuing the factors that drive those numbers. For example, steady patient volume, strong referral sources and a solid reputation all create stable cash flows and lower risk. The stronger those drivers, the higher the multiple.

While these traits aren’t always visible in the data, we use judgment and experience to interpret what likely drove these multiples and the price buyers were willing to pay. Then, we assess whether your practice shares those exact same traits. If it does, applying a similar multiple may make sense. If not, we adjust the multiple up or down to reflect any meaningful differences.

And because private clinics are harder to buy and sell than public stocks, we usually apply a discount to reflect that lower liquidity and less transparent pricing.

Planning a merger or acquisition? Check out our list of the top M&A advisory boutique firms in the U.S. to find expert guidance tailored to your needs.

Unlike the GPC Method, which looks at stock-market prices, the Guideline Transaction Method shows what buyers actually paid to acquire similar PT clinics. It’s grounded in real deals, so you see the price people put on practices like yours.

For example, if a comparable clinic sold for 3x EBITDA and your clinic earns $2 million in EBITDA, that points to a $6 million value (3 x $2 million).

But every deal has its own story. Maybe the buyer paid extra to enter a new region, or the seller accepted less because they needed a quick close. That’s why we adjust for those one-off items so the multiple reflects your clinic’s value apart from special circumstances.

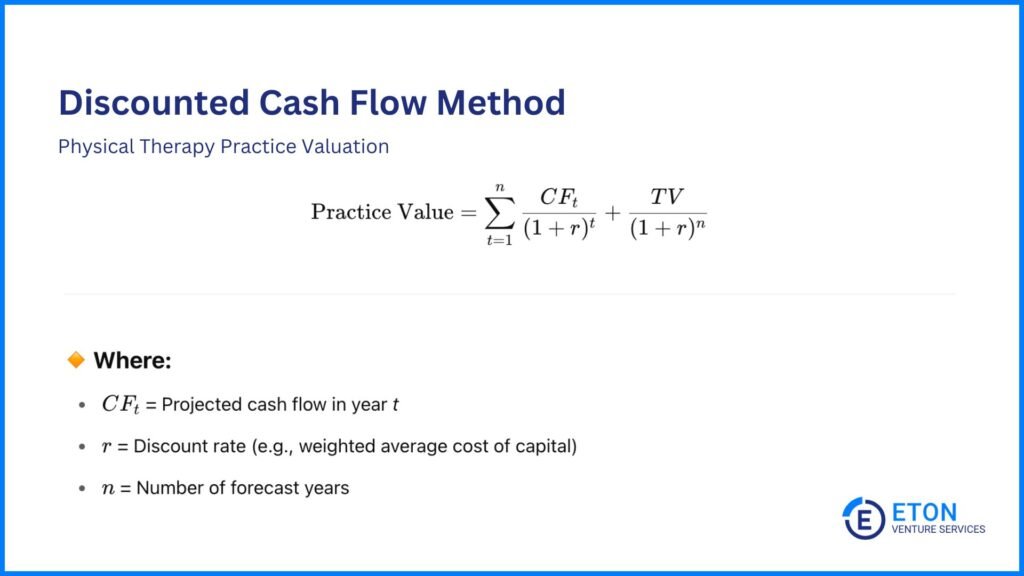

The DCF Method forecasts the cash your physical therapy practice will generate over time, then converts those future dollars into today’s value.

It’s best for clinics with stable, recurring revenue and predictable earnings, where you can reasonably estimate how many visits, and at what rates, you’ll see each year.

Here’s how it works:

Need third-party valuation help? Explore our guide to the top third-party valuation firms and find the right partner for your business.

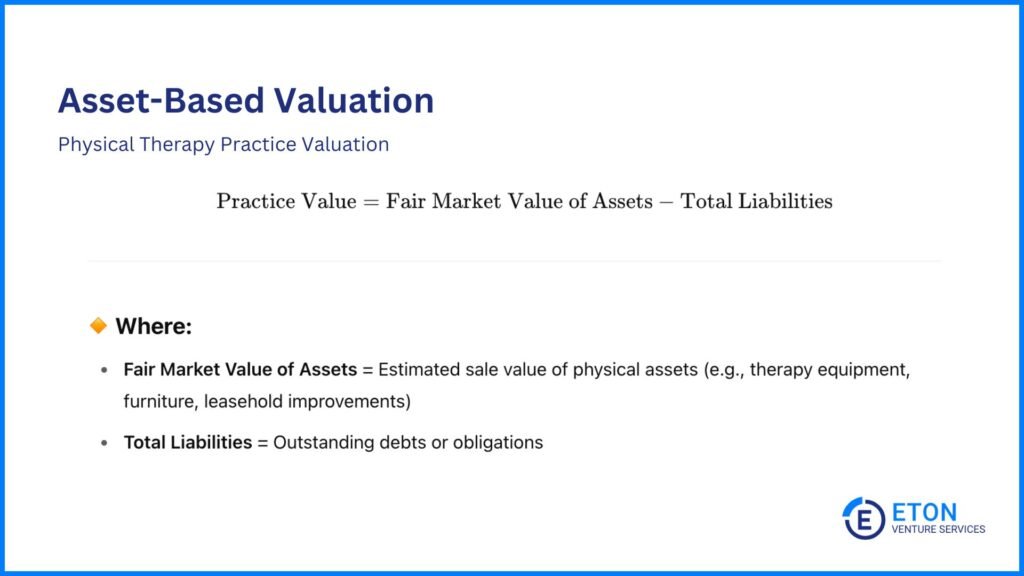

The asset-based approach values a PT practice based on the physical assets it owns. Everything from therapy tables and ultrasound machines to exercise equipment and even the office leasehold. It’s suitable when a smaller practice’s worth lies more in tangible investments than in its earnings or future growth potential.

To apply it, you total the fair market value of all assets and subtract any liabilities. For example, if your equipment, furniture and leasehold improvements are worth $2 million and you owe $600,000, then: $2,000,000 – $600,000 = $1,400,000. That $1.4 million is your practice’s value.

However, this method doesn’t capture intangible assets like referral networks, payer relationships, and brand reputation, all of which can drive long-term value beyond the bricks and machines.

For businesses where these factors play a significant role, it’s often best to combine this approach with income-based (DCF) or market-based methods (GPC/GT). There are two ways to do this:

PT practices often have steady cash flow thanks to ongoing care. But buyers and investors don’t just look at cash flow to set a price. They dig into the factors that support its stability.

Valuation experts play a huge role here. We analyze these drivers, highlight their impact, and make the case for how they shape your practice’s overall value.

Here are the main factors we consider:

When local orthopedic surgeons send you post-op patients week after week, and gyms refer members recovering from injuries, you can count on a reliable pipeline of care. That consistency helps ensure a single slow month won’t derail your cash flow.

And when your referral sources are diversified (MDs, chiropractors, sports teams and self-referrals), your clinic is less vulnerable if a single source dries up.

Buyers are willing to pay a premium for that stability, as it reduces risk and delivers more reliable earnings post-acquisition.

It’s one thing to set a price and another to actually collect it. Locked-in contracts with Medicare or private insurers mean you know exactly what an evaluation or follow-up visit will net you.

For example, a guaranteed $120 for evaluations and $80 for follow-ups lets you forecast revenue down to the visit.

Clinics with negotiated fee schedules also face fewer surprise rate cuts or claim denials, which makes their cash flows more dependable and leads to a stronger valuation.

Faster recoveries free up appointment slots for new patients without adding staff. For example, completing a typical treatment plan in eight visits instead of ten lets you treat 20% more patients with the same resources.

At the same time, strong outcome metrics, like a 90% success rate in restoring range of motion, enhance your reputation and drive referrals.

This mix of efficiency and proven results tells buyers you deliver high value at low incremental cost, which justifies a higher price in their eyes.

Your clinic’s payers (Medicare, private insurers, and workers’ comp) stand between you and your cash flow.

If you consistently track each payer’s policy updates, proactively negotiate contract renewals, and act quickly on denials with appeals or corrected documentation, you can compress pre-authorization times to days rather than weeks and keep denial rates low.

When authorizations arrive fast, treatments start on time and payments follow promptly, and with fewer denials your team spends less time chasing paperwork or writing off claims.

Combined, these strengths lead to smoother operations and steadier cash flow, exactly what buyers look for when assessing risk.

A clinic that draws 50% of its revenue from Medicare, 30% from private insurance and 20% from self-pay weather policy changes far better than one with 90% Medicare.

So a diverse payer mix can cushion the blow if rates are cut or audits intensify. That balance is a key signal of lower risk and higher value to potential buyers.

A string of five-star Google ratings and video testimonials from happy patients creates social proof that money can’t buy.

When prospects see evidence of excellent care before they even call, they’re more likely to book. That built-in marketing lift reduces your customer-acquisition cost and strengthens the case for a higher valuation.

Buyers also look at whether that goodwill lives with the practice or rides on one or two people. If your reputation hinges on a star therapist, patients may follow them elsewhere. That adds risk.

But when your brand is built across multiple clinicians, it signals stability and makes your practice’s value more transferable.

Your clinic must follow rules at every step, everything from how you document an evaluation to the paperwork you keep after discharge. This regulatory complexity affects medical practice valuation across all specialties. When you build audit-ready checks into your daily routines, you avoid surprise write-offs and fines.

Passing state inspections and Medicare reviews with spotless records shows buyers you run a low-risk operation. That confidence in compliance translates directly into a higher valuation.

Patient visits tend to rise and fall with sports seasons, surgery schedules and holiday breaks. Some months you’ll see a flood of post-op rehab cases; other times, the schedule can look thin.

Clinics that fill those slow stretches with group wellness classes or quick tele-PT check-ins keep the calendar and the cash flow steady.

That steady rhythm shows buyers you’ve smoothed out the peaks and valleys, so they won’t inherit sudden revenue gaps after closing. This leads to a higher valuation.

At Eton Venture Services, we provide accurate, independent valuations that support your decision-making, whether you’re planning for growth, preparing for a transaction, or structuring a transition.

Our team of experts is dedicated to offering the highest level of service in assessing the value of your physical therapy practice. We ensure that all key factors, such as patient volume, billing rates, treatment efficiency, payer mix, reputation, and more, are thoroughly considered.

Trust our experts to deliver insightful, tailored valuations that support your next move.

Possibly, but only if those services generate consistent revenue and fit into your care model. Ancillary services that improve patient retention or attract new referrals can support higher valuation, but occasional, one-off, or low-margin services typically don’t move the needle.

Yes, a solo practitioner’s clinic can still be valued highly if it has steady revenue, strong referral sources, and efficient operations. The key is how easily that income can continue without you.

If a buyer can step in or hire a qualified replacement without losing patients or disrupting cash flow (i.e. when your practice runs on repeatable treatment protocols, has referral agreements in place, and patients come for the clinic’s reputation rather than just your name) the valuation can remain strong.

But if the business depends heavily on your personal relationships or presence, that may reduce its value.

Telehealth can boost your valuation if it creates new revenue streams, reduces cancellations, or fills schedule gaps during off-peak periods.

Buyers see value in flexibility, especially if your systems, documentation, and billing are already set up for virtual care.

However, if telehealth is underused or poorly integrated, it may not add much value on its own.

You treat the PT division as its own business.

The result is a clear, defensible value for that part of the business.

To learn more about how to sell a part of a business, such as a PT practice that’s part of a larger group in this case, we recommend reading this article.

Schedule a free consultation meeting to discuss your valuation needs.